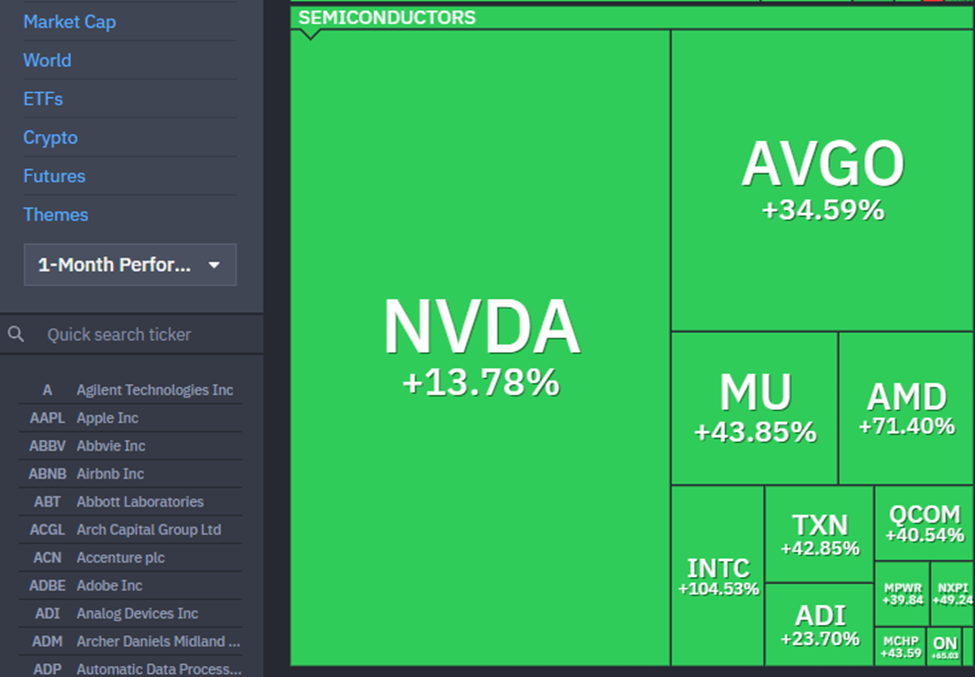

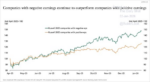

The semiconductor leaderboard has quietly flipped over the past month, and the NVDA to CPU rotation is worth pausing on. NVDA, the name that defined the AI trade for two-plus years, is up just 13.4% over the trailing month. The CPU cohort has run circles around it. AMD has ripped 70.4% higher, MU has added 44.7%, and even INTC has outpaced Nvidia by a wide margin. Over the past week, the divergence widened further. NVDA fell 4.3% while AMD posted another 3% gain and MU surged 7.3%. NVDA is now the laggard within its own sector, an unfamiliar position for a stock that has effectively been the market for the last 24 months.

Some of this NVDA to CPU rotation is due to positioning. NVDA entered 2026 as the most-owned, most-crowded, and most-hedged name on the Street. And crowded trades exhaust themselves long before fundamentals roll over. When relative performance flips, the marginal dollar chases laggards rather than leaders, and CPU names with depressed valuations become the obvious release valve.

The more durable thesis is the one we laid out on April 21st. The shift from LLM training to agentic AI applications creates incremental demand for CPUs. In theory, this shifts who captures the next dollar of AI capex. Hyperscalers building out agentic infrastructure cannot do it on Nvidia silicon alone. That math benefits the CPU complex on the margin, even if Nvidia retains its 75% gross margin moat at the high end of the GPU stack. The NVDA to CPU rotation reflects the market beginning to discount that mix shift in real time.

Here is the catch. AMD reports earnings tomorrow, and NVDA reports later this month. Neither has confirmed the thesis with numbers yet. If AMD guides cautiously on data-center momentum, or NVDA delivers another beat-and-raise quarter with strong Blackwell commentary, a large portion of this rotation could reverse in a matter of days. The NVDA to CPU rotation is a longer-term thesis worth respecting, but not a trade worth chasing into earnings.

What To Watch Today

Earnings

Economy

Market Trading Update

me high of 7,220 on Friday following Apple’s blowout earnings (+3%). From the March low of ~6,300, the index has rallied roughly 15% in five weeks, which blew through BofA’s 7,168–7,206 target we flagged as resistance just two weeks ago. Both the Nasdaq and S&P 500 posted consecutive record closes; breadth was solid in the equal-weight index; the Russell 2000 outperformed; and Q1 earnings are beating across the board.

The technical picture is unanimously bullish but increasingly stretched. According to Investing.com, 12 of 12 moving average signals are at a “Strong Buy.” The 14-day RSI sits at 71.18, touching the 70 overbought threshold, and momentum is extended and rising, but closing in on a "sell signal.". The 50-DMA has surged to ~6,821, while the 200-DMA stands at ~6,728, now 5.2% below the index. VIX is also at its lowest since January. The nuance, however, is that overbought does not mean overvalued. RSI can remain above 70 for weeks during a strong trend, and 12 of 12 buy signals means momentum is confirmed, not exhausted. But the higher it climbs, the sharper the eventual mean-reversion pullback.

The most striking feature is that the S&P 500 is hitting records while oil sits above $105, gasoline has surged 42–44% to $4.30 per gallon, and consumer sentiment hit its lowest on record. The Iran conflict remains unresolved, with Trump saying Friday that “no one knows the status of talks aside from himself.” PCE came in line, and Q1 GDP was resilient, but AI investment is carrying the load while private consumption slows. The market is pricing in a resolution: strong earnings growth, expanding multiples, and a ceasefire narrative gaining ground. But the consumer is flashing red, and the war premium hasn’t unwound. The longer oil stays above $100, the more the economic damage compounds beneath the surface. As we noted on Friday:

"The market is not pricing oil at $90 in 2027; it is pricing it at roughly $70. That is either a generational good hedging opportunity for any business that buys energy, or a generational mistake that gets corrected violently. Below is the updated three-scenario framework. The structure from March holds; the probability weights and price targets have shifted to reflect the new reality."

Time is the most important factor in the market. We are in the rare position of holding a technically perfect tape, new highs, broad breadth, all MAs flashing buy, VIX at 17, while the fundamental backdrop includes a war, $105 oil, record-low consumer sentiment, and a Fed on hold. The technicals say stay long. The fundamentals say this market is priced for perfection with zero margin for error. Both can be true. Trail stops, take partial profits, and use any pullback to the 50-DMA (~7,158) or the 7,000 level to add. The March lows at 6,300 feel like ancient history; they’re not. That was five weeks ago. Stay humble. Trade accordingly.

The Week Ahead

The labor market takes center stage this week. JOLTS openings tomorrow (expected 7M vs. 6.882M prior), ADP employment on Wednesday, and Friday's nonfarm payrolls report frame the action. Wall Street is bracing for a sharp slowdown, with consensus calling for just 73K jobs added in April. That estimate sits well below March's 178K print. The unemployment rate is expected to hold at 4.3%. If the data cooperate with expectations, it would mark the weakest two-month stretch of job creation in some time and reinforce the cooling narrative the Fed has been watching closely.

Tomorrow also brings the ISM Services PMI, expected to ease to 53.7 from 54.0. Given that services represent roughly 80% of GDP, any stumble would be a louder warning than the headline payroll number. Thursday's Q1 unit labor costs are expected to moderate to 3.0% from 4.4%, an important input into the Fed's inflation math. Friday's preliminary Michigan Consumer Sentiment reading is expected to tick up to 50 from 49.8, though the absolute level remains historically depressed.

Finally, the Fed speaker calendar is relentless. Bowman, Barr, Musalem, Goolsbee, Hammack, Williams, Cook, Daly, and Waller all hit the wires this week. Some speeches may offer hints on the policy path, and any dovish tilt against a soft NFP could light a fuse under both stocks and bonds.

A Robot Economy: Who Gets Rich, Who Gets Left Behind

The real question I want to explore in today’s post is what happens to the people who don’t own the robots? Let’s dig in.

I spent the past week reading through a detailed account of what’s happening inside Figure’s robotics facility in San Jose, and I want to be direct: the humanoid robots economy is no longer a thought experiment. Figure’s latest robot ran for 67 consecutive hours of fully autonomous work, kitchen tasks, package handling, and logistics, without a single error. That’s not a demo reel, that’s a product. When you factor in a projected lease cost of roughly $10 a day, it’s a product priced to replace the single largest input cost on every corporate income statement in America: human labor.

The optimists call what’s coming the “age of abundance.” Cheaper goods, freed-up time, robots building robots until supply constraints essentially disappear. That would be incredible, and you should not dismiss that vision. Furthermore, I think it’s directionally correct over a long enough horizon. But after 35 years of watching economic cycles play out, I’ve learned that the gap between a macro promise and the lived experience of actual households is where the real story lives.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post NVDA To CPU Rotation: Durable Thesis Or Crowded Trade? appeared first on RIA.

Full story here Are you the author?You Might Also Like

A Fed Balancing Act: Oil, Iran, Slower Growth

A Fed Balancing Act: Oil, Iran, Slower Growth

2026-03-19

Few Fed meetings in recent memory have presented the FOMC with a more uncomfortable set of competing signals than yesterday’s. The Iranian conflict and its impact on oil and oil-dependent product prices have created the potential for an inflationary impulse, yet higher oil prices would likely slow economic activity, leading to higher unemployment. As if …

The Value Rotation Illusion

The Value Rotation Illusion

2026-02-11

“Value is back in vogue”, the media claim. Investors are rushing out of the high-flying mega-cap tech stocks and into the boring staples, utilities, and healthcare stocks. Given the huge outperformance of value stocks versus growth stocks, it appears investors are going all in on the value rotation. What some of these investors don’t know …

Warsh To Head The Fed

Warsh To Head The Fed

2026-02-02

The wait is over, and President Trump has nominated Kevin Warsh to head the Federal Reserve. To better appreciate Warsh’s views on monetary policy and what they may entail for markets, we summarize a recent Wall Street Journal editorial he wrote, The Federal Reserve’s Broken Leadership. Our market-related thoughts are below the bullet points. From …

Mainstream Expectations: Hope Vs. Potential Risk

Mainstream Expectations: Hope Vs. Potential Risk

2026-01-30

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure. As such, many institutional investors interpret this as a year of opportunity for markets and corporate earnings.That was a …

The Reflation Narrative Stumbles Out Of The Gate

The Reflation Narrative Stumbles Out Of The Gate

2026-01-26

With a 4.4% increase in economic growth in the third quarter and expectations that it could be higher in the fourth quarter, the so-called reflation narrative appears primed to dash out of the gates in 2026 at its current strong pace. The problem with assuming the reflation narrative will hold in 2026 is that it …

QE Is Back: Which Assets Benefits From The Liquidity Boost

QE Is Back: Which Assets Benefits From The Liquidity Boost

2025-12-17

QE is back! On December 10th, the Federal Reserve announced its plan to purchase $40 billion in Treasury securities each month for at least four months. Through these QE purchases, bank reserves will increase, and recent liquidity concerns should lessen. Furthermore, increased liquidity often leads to more speculative market conditions and higher asset prices as …

2025-12-10

Michael Green, Chief Strategist and Portfolio Manager at Simplify Asset Management, wrote a provocative Substack essay, Part 1: My Life Is A Lie, that is sparking a debate among economists and raising awareness of the affordability crisis. It’s not just the wonky economists debating the merits of his article; The Washington Post, CNN (News Central), …

Natural Gas Prices: Weather, Data Centers And LNG

Natural Gas Prices: Weather, Data Centers And LNG

2025-12-04

As we share below, courtesy of FinViz, natural gas prices have risen by over 50% since late October. Moreover, natural gas prices, approaching $5, are at three-year highs. The primary cause of the recent price surge is increased heating demand driven by colder-than-expected winter weather, which is resulting in greater-than-average inventory draws. Per the EIA, …

Tags: Featured,newsletter