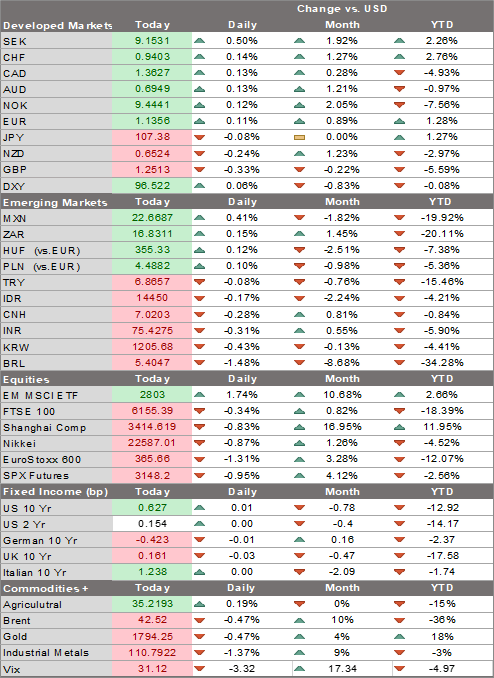

- Market sentiment has been dented by more than just rising virus numbers; yet the dollar continues to trade within recent well-worn ranges

- California’s decision to reverse partial reopening will likely have a huge economic impact; June CPI may hold a bit more interest in usual; June budget statement is worth a quick mention

- Weak eurozone IP was reported; machinations around the EU’s €750 bln rescue fund continue to progress in the right direction

- UK data today was very disappointing; UK Office for Budget Responsibility (OBR) published its fiscal sustainability report; Poland is expected to keep rates steady at 0.10%

- Singapore advance Q2 GDP was disappointing; China’s trade figures rebounded faster than expected in June; US officials have ruled out attacking the HKD peg

Market sentiment has been dented by more than just rising virus numbers.

Today’s economic data has been largely disappointing and comes after a series of negative developments yesterday. The Dow Jones Industrial Average burned through 600 points in a couple of hours yesterday afternoon on a series of bad headlines: The US posted a record -$864 bln budget deficit in June, American Airlines warned pilots about possible furloughs, California closed indoor dining and bars as its virus numbers spiked, and geopolitical tension rose as the US rejected China’s South China Sea claims, calling them “completely unlawful.” China then imposed sanctions on Lockheed Martin in response to US arms sales to Taiwan.

Yet the dollar continues to trade within recent well-worn ranges. DXY has for the most part traded between 96 and 98 since early June. Similarly, the euro has traded between $1.12 and $1.14 and sterling between $1.22 and $1.27 since early June. USD/JPY has traded within a 106-108 range since mid-June. Right now, the dollar is still pretty much in the middle of all these trading ranges. With problems mounting for the US economy, we think the risks of a breakout from these ranges for the dollar is tilted towards the downside.

AMERICAS

California’s decision to reverse partial reopening will likely have a huge economic impact. Governor Newsom ordered statewide closure of all bars, indoor dining, wineries, and theaters. The state will also close indoor gyms, malls, houses of worship, and hair salons in 30 of the hardest hit counties. As we’ve noted before, California accounts for nearly 15% of GDP, followed by Texas at nearly 9%. Florida accounts for 5% of GDP so these three states together account for almost 30% of total US GDP. With many reopenings on hold or reversed now, this will be a headwind for Q3. Period. If these states can quickly bend the curve back down, perhaps the recovery can proceed but as of now, we are getting more pessimistic about the US economic outlook in H2.

June CPI may hold a bit more interest in usual given the recent downward trajectory in US Treasury yields. Consensus sees headline inflation of 0.6% y/y vs. 0.1% in May, and core inflation of 1.1% y/y vs. 1.2% in May. After last Friday’s downside miss in PPI (headline -0.8% y/y vs. -0.2% expected), we see similar risks for CPI. The Fed’s Brainard and Bullard speak. This past week, many Fed officials have warned of increasing downside risks due to the rising virus numbers. Yesterday, Kaplan noted that the recovery is losing momentum and that the Q3 rebound is likely to be a bit more muted than expected.

June budget statement out yesterday is worth a quick mention. The deficit came in close to consensus at -$864 bln deficit vs. -$398.8 bln in May. This one month nearly eclipses the deficit for all of FY2019 and brings the 12-month total to another record high of nearly -$3 trln. Receipts fell -28% y/y, while outlays surged 223% y/y. There is no reason to believe that this trend reverses anytime soon, especially with another round of stimulus being negotiated that is likely to total $1 trln. Note that our latest sovereign ratings model for Q3 shows increasing downgrade risks for the US, driven largely by fiscal slippage.

EUROPE/MIDDLE EAST/AFRICA

Ahead of the ECB decision Thursday, weak eurozone IP was reported. The headline reading came in at 12.4% m/m vs. 15.0% expected and a revised -18.2% (was -17.1% in April). Given the IP readings already reported by Germany, France, and Italy, we thought the risks were tilted to the upside. Elsewhere, Germany’s ZEW survey for July came in on the weak side. The expectations component printed 59.3 and the current situations component was -80.9, both well below forecasts.

Machinations around the EU’s €750 bln rescue fund continue to progress in the right direction. Overnight, reports suggest that Italy is willing to accept more stringent criteria required by the Frugal Four countries for receiving grants and loans. The group will hold its summit this Friday and Saturday. Again, we would be very surprised if this package did not make it through, even if somewhat watered down compared to the original headlines. But we also think this outcome is largely priced in, so we wouldn’t bet on a large upside market reaction.

| UK data today was very disappointing. GDP grew 1.8% m/m vs. 5.5% expected, construction output rose 8.2% m/m vs. 15.0% expected, and services rose 0.9% m/m vs. 4.8% expected. Elsewhere, IP rose 6.0% m/m vs. 6.5% expected and manufacturing production rose 8.4% vs. 7.8% expected. Asset prices in the UK are moving largely in line with broad markets trends, with sterling a touch weaker against the dollar, gilt yields down a couple of basis points across the curve, and the FTSE 100 is outperforming slightly.

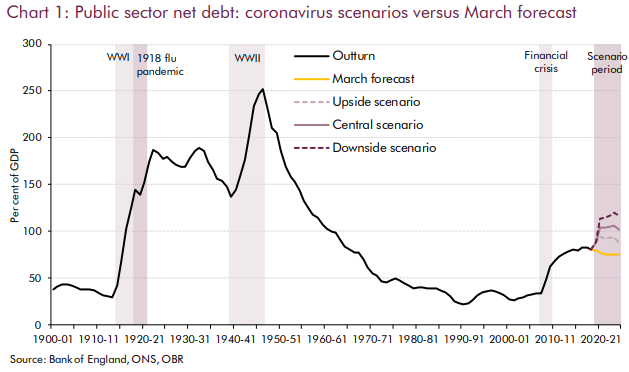

The UK Office for Budget Responsibility (OBR) published its fiscal sustainability report today updating its projections. In the worst-case scenario, the economy will contract 14.3% on the year. The budget deficit is projected to widen anywhere between 13 to 21% of GDP and unemployment will rise to around 10% next year. (Full report here). Note that our latest sovereign ratings model for Q3 shows increasing downgrade risks for the UK, driven largely by fiscal slippage. National Bank of Poland is expected to keep rates steady at 0.10%. After surprising markets with a 40 bp cut in May, the bank kept rates steady in June and sounded a bit more upbeat. For now, we think the bank will remain in wait and see mode. Poland also reports May trade and current account data Tuesday. Minutes will be released Thursday and its quarterly inflation report will be released Friday. |

Public Sector Net Debt, 1900-2020 - Click to enlarge |

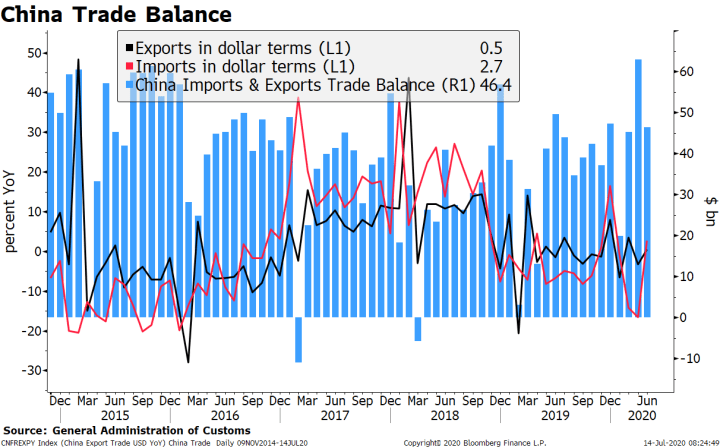

ASIASingapore advance Q2 GDP was disappointing. The economy contracted -12.6% y/y (-41.2% SAAR) vs. -10.5% y/y (-35.9% SAAR) expected. The results were a bit disappointing since government has delivered five stimulus packages totaling nearly 20% of GDP. At this clip, growth might come at the lower range or even undershoot the government’s forecast of -4% to -7% for the year. This is the first Q2 reading and while Singapore is a small economy, it serves as a regional bellwether. Despite the recovery in the mainland China economy, the region has yet to feel much of a recovery. June trade will be reported Friday, with NODX expected to rise 4.9% y/y vs. -4.5% in May. China’s trade figures rebounded faster than expected in June. Exports rose 0.5% y/y (-2.0% expected) and imports increased 2.7% y/y (-9.0% expected). The trade surplus shrank to $46 bln from a $62 bln record last month. Imports were supported by commodities while exports benefited from higher demand for medical equipment and clothes. Q1 GDP and June retail sales and IP will be reported Thursday. GDP is expected to rise 2.2% y/y vs. -6.8% in Q1, sales are expected to rise 0.5% y/y vs. -2.8% in May, and IP is expected to rise 4.8% y/y vs. 4.4% in May. Data last week suggest that loan and aggregate financing growth remain robust in response to previous easing measures. |

China Trade Balance, 2015-2020 - Click to enlarge |

| Reports suggest US officials have ruled out attacking the HKD peg as a way of punishing China. The fact that it wouldn’t impact China officials was reason enough to rule it out, but we are incredulous that it was even being discussed. |

. |

Full story here Are you the author?

Tags: Articles,Daily News,Featured,newsletter