Perspectives Pictet

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterFacebookAmazon

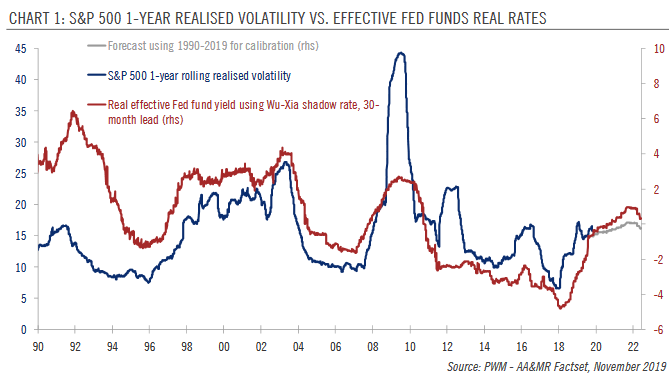

| Whereas inflation is expected to be dormant next year, our expectation of real GDP growth of just 1.3% in the US in 2020 could put upward pressure on equity volatility. Since monetary policy tends to lead volatility by two and a half years, the Fed’s turn toward quantitative tightening in 2017 is also continuing to exert upward pressure on volatility levels for now.

But there are also countervailing forces at work. Although there is not a perfect correlation, decreasing margins tend to translate into higher volatility. As we outline in our 2020 outlook for equities, we expect margins to remain elevated in 2020, as wage increases are offset by benign raw material prices. Volatility also increases when consensus dispersion on future earnings is high. Consensus dispersion on the S&P 500 has been muted since 2017. In our core scenario we do not see either margins or consensus earnings dispersion as factors in volatility in 2020. |

S&P 500 1-year Realised Volatility vs Effective Fed Funds Real Rates, 1990-2019 - Click to enlarge |

Slowing economic momentum and the lagged effect of quantitative tightening are putting upward pressure on equity volatility. By contrast, the low-yield environment and the development of risk premia strategies that extract yield from options are creating natural inflows into short-volatility strategies. Structurally positive gamma is also tending to cap volatility. Combining these different positive and negative factors and taking account of occasional spikes leads us to predict an average one-year realised volatility level of 16% for the S&P 500 in 2020.

Tags: newsletter,Pictet