Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

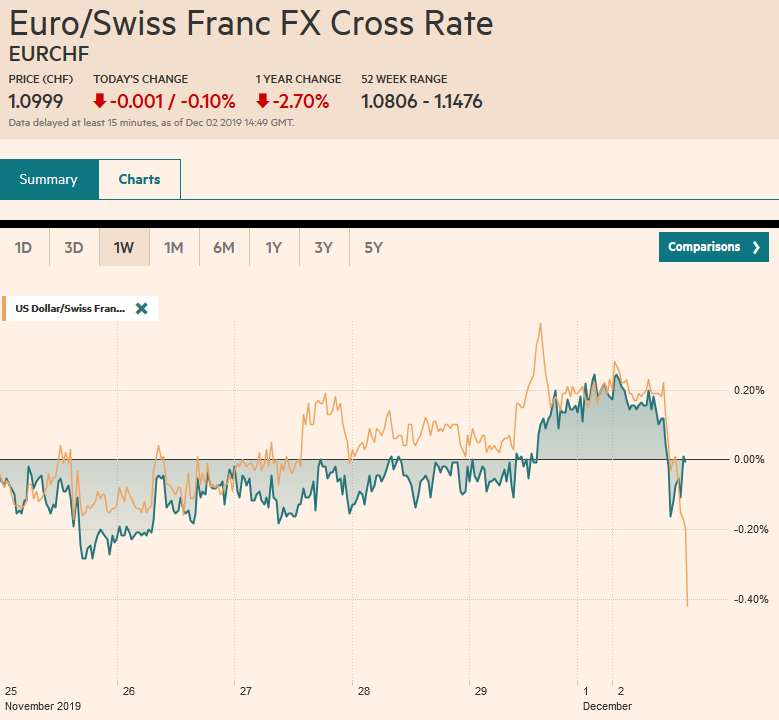

Swiss FrancThe Euro has fallen by 0.10% to 1.0999 |

EUR/CHF and USD/CHF, December 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

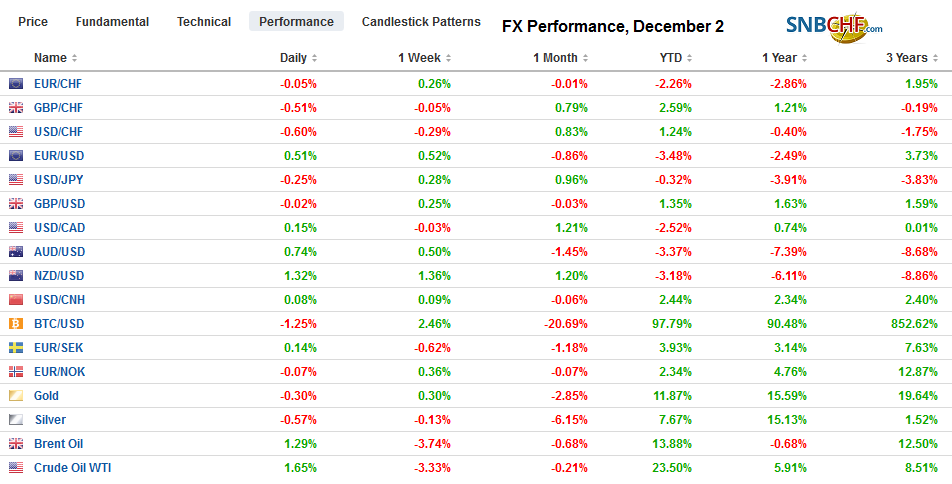

FX RatesOverview: Mostly better than expected manufacturing PMI readings for December, including in China, is providing the latest incentive for equity market bulls. Led by the Nikkei, which was aided by a weaker yen major equity markets in Asia Pacific rallied and recouped most of the nearly 1% loss before the weekend. Europe’s Dow Jones Stoxx 600 is also shrugging off the pre-weekend loss and to challenge the multiyear high recorded last week. US shares are trading firmer, and the S&P 500 could gap slightly higher at the open. Bond markets are selling off hard, with benchmark yields mostly 5-7 bp higher in Europe and the US, and 3-6 bp in Asia Pacific. Irish bonds are holding up better than most, following the S&P upgrade before the weekend to AA-.The dollar is mixed. The Antipodean and Scandi currencies are posting modest gains, while yen, euro, and sterling are posting small losses in narrow ranges. Gold has given up its month-end gains to again test support near $1450. Oil is recovering from its biggest drop in two months ahead of this week’s OPEC meeting. The current output agreement extends through March 2020. Most expect the quotas to be extended. |

FX Performance, December 2 - Click to enlarge |

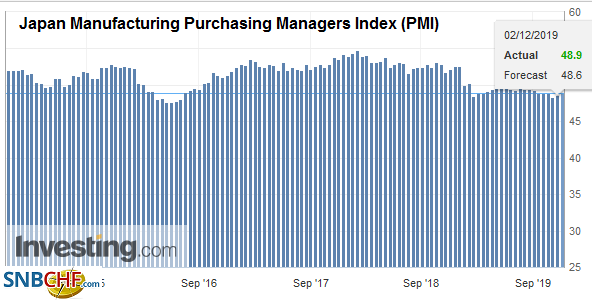

Asia PacificChina announced it would sanction some rights groups and halt US warships from making port in Hong Kong in response to the Hong Kong bills the US Congress widely backed, and President Trump signed into law last week. It does not appear to have derailed the trade talks, whose outcome remains uncertain given Beijing’s demand to roll back tariffs, not just the mid-December round the US has threatened. Many are still hopeful that phase one of an agreement can be reached. China surprised with a stronger than expected November PMI, and traders saw it with a jaundiced eye. The official manufacturing PMI rose 50.2 from 49.3. It was the first time above the 50 boom/bust level since April. The Caixin PMI, which puts more weight on smaller businesses (51.8 vs. 51.7), defying expectations for a cut. The official non-manufacturing PMI rose to 54.4 from 52.8. This led to a rise in the composite to 53.7 from 52.0, the highest since March. Japan’s data was generally better than expected. The November manufacturing PMI rose to 48.9 from the flash report or 48.6 and the October reading of 48.4. Capital spending in Q3 rose 7.1% (Bloomberg median was for a 5% gain after a 1.9% increase in Q2). However, corporate profits fell (-5.3%, which was twice what economists expected). There was a local press report that suggested that the Abe government may consider doubling the initial supplemental budget from JPY5 trillion to JPY10 trillion. |

Japan Manufacturing Purchasing Managers Index (PMI), November 2019(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

South Korea’s November trade figures suggest that if the region’s slowdown in trade has ended, the recovery may be painfully slow. South Korea’s exports and imports were weaker than expected though posts sequential improvement. Exports fell 14.3% year-over-year after a 14.8% decline in October. Imports were off 13.0%, following a 14.6% deterioration. The trade surplus has fallen by nearly 45% this year to an average of $3.39 bln a month from $5.95 bln in the first 11 months of 2018. Separately, South Korea reported CPI rose 0.2% from year-ago in November, It was flat in October after a 0.4% decline in September. The core rate was 0.6%. The deflationary threat has ebbed, but price pressures are expected to be muted for several more months. Separately, its November manufacturing PMI rose to 49.4 from 48.4. Indonesia and Malaysia also reported manufacturing PMIs that showed sequential improvement but still below 50. The Philippines saw its PMI slip from 52.1 to 51.4. Thailand stands out with a decline to 49.3 from 50.0.

The dollar edged higher to a new seven-month high against the Japanese yen to just below JPY109.75. The greenback has been confined to about a quarter of a yen range. There are options struck between JPY109.50 and JPY109.52 for $1.4 bln. The Australian dollar is snapped a three-day slide that took it to $0.6755 before the weekend. It is testing the $0.6790 area in the European morning. Shorts may be being trimmed ahead of the central bank meeting results that will be announced first thing tomorrow in Australia. The Chinese yuan weakened slightly today to trade at the lower end of its two-week range. The dollar has been confined to about a CNY7.02-CNY7.0450 range since mid-November.

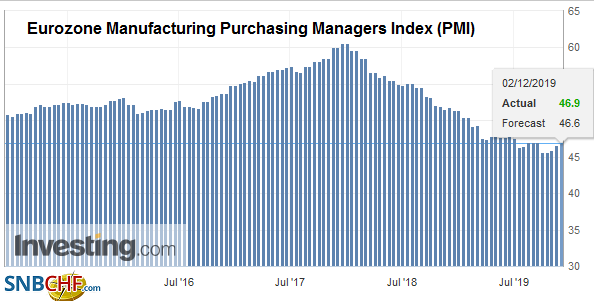

EuropeThe manufacturing PMI for the eurozone improved from the flash reading of 46.6 to 46.9 and 45.9 in October. This was a function of German and French reports being revised up. Germany’s stands at 44.1 from the 43.8 flash reading. The manufacturing PMI may have bottomed in September at 41.7. The French reading ticked up to 51.7 from the 51.6 initial estimate and 50.7 in October. It bottomed in July at 49.7. Italy slipped to 47.6 from 47.7. Its low was in March at 47.4. Spain bounced from its cyclical low of 46.8 in October to 47.5 in November. Overall, the decline in new orders slowed, and business confidence rose to a five-month high. |

Eurozone Manufacturing Purchasing Managers Index (PMI), November 2019(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

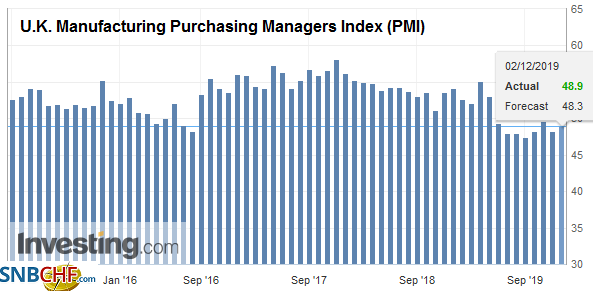

| Separately, the UK’s manufacturing PMI trimmed the decline reported in the flash estimate but remains below the 50 boom/bust. It stood at 49.6 in October and fell to 48.9, not 48.3 in November. It had bottomed in August at 47.4. |

U.K. Manufacturing Purchasing Managers Index (PMI), November 2019(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The German Social Democrats chose new leaders that have been more critical of the Grand Coalition with Merkel’s CDU. Still, it would be an exaggeration to see this a left-tilt. For example, the new leaders, Walter-Borjans and Eskek, propose a minimum wage in Germany of 12 euros, which is less than what is being proposed by UK Prime Minister Johnson. The SPD is ill-prepared (drawing less than 15% support in recent polls vs. 20.5% in 2017) for an election, so leaving the coalition now does not seem particularly likely. A vote this coming weekend will likely confirm this, but new leaders may seek to re-negotiate the 2018 coalition agreement. The CDU is in an awkward position, as well. It does not want to re-open the coalition agreement. While the SPD is being challenged by the Greens from the left, the CDU is being outflanked to the right. However, the transition to a post-Merkel era has been anything but smooth. It, too, would likely see its support fall in a snap election were to be held now.

The euro remains mired in a narrow range of a little more than 15 pips today. It has held above $1.1010 and has not been much above $1.1025. There nearly 1.3 bln euros of options between $1.0995 and $1.1000 that will be cut today. ECB President Lagarde’s first speech to the European Parliament attracts attention, of course, but may not provide new trading incentives. Sterling’s range is twice as large at around 30 pips, but it still not particularly inspiring, and it is within the pre-weekend range (~$1.2880-$1.2945).

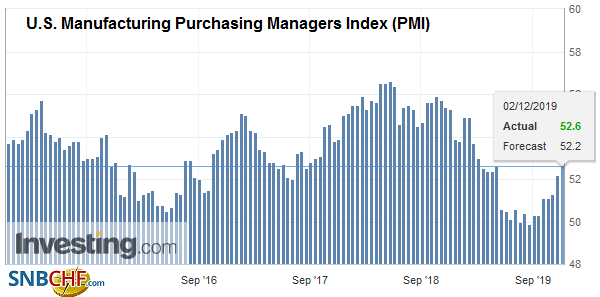

AmericaThe US reports November ISM/PMI. The flash manufacturing PMI showed the third consecutive gain to 52.2 from 51.3. It bottomed in August at 50.3. The ISM is expected to have gained as well. The week’s highlight is the jobs report on Friday. The end of the GM strike is expected to boost the headline by 40-50k (to about 190k). Note last week’s data that inspiring the Atlanta GDP tracker to jump to 1.7% in Q4 from 0.4%. However, the NY Fed’s model was less impressed and ticked up to 0.8% from 0.7%. |

U.S. Manufacturing Purchasing Managers Index (PMI), November 2019(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The Bank of Canada meets in the middle of the week and is widely expected to keep rates steady (1.75%). The November jobs report will be released at the end of the week. Employment is expected to have gained (~10k) after a small decline in October. The highlight for Mexico this week maybe today’s PMI. Both the manufacturing and non-manufacturing readings are expected to have remained below 50.

The intervention that Chile announced last week begins today. The dollar fell 2.2% against the peso before the weekend as positions were adjusted. The greenback still rose almost 1.5% last week to extend its streak to the seventh consecutive week. The Chilean central bank will sell $200 mln day this week and place $200 mln in the forward market is well. The central bank meets on Wednesday, and despite the currency’s weakness, many still expect it to cut the official cash rate by 25 bp to 1.50%. It has delivered three rate cuts since June for a total of 125 bp.

The US dollar is trading sideways against the Canadian dollar. It has been carving out a pennant formation. The falling resistance line is found near CAD1.3315 today, and the rising support line is seen near CAD1.3265. The Mexican peso is little changed. It has fallen for the past three weeks. Both local developments and its role as a proxy for other emerging market currencies, especially in Latam recently, have worked against it. It reached almost MXN19.66 last week and fell to MXN19.4250 ahead of the weekend.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Chile,EUR/CHF,Eurozone Manufacturing PMI,FX Daily,Germany,Japan Manufacturing PMI,newsletter,South Korea,U.K. Manufacturing PMI,U.S. Manufacturing PMI,USD/CHF