Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

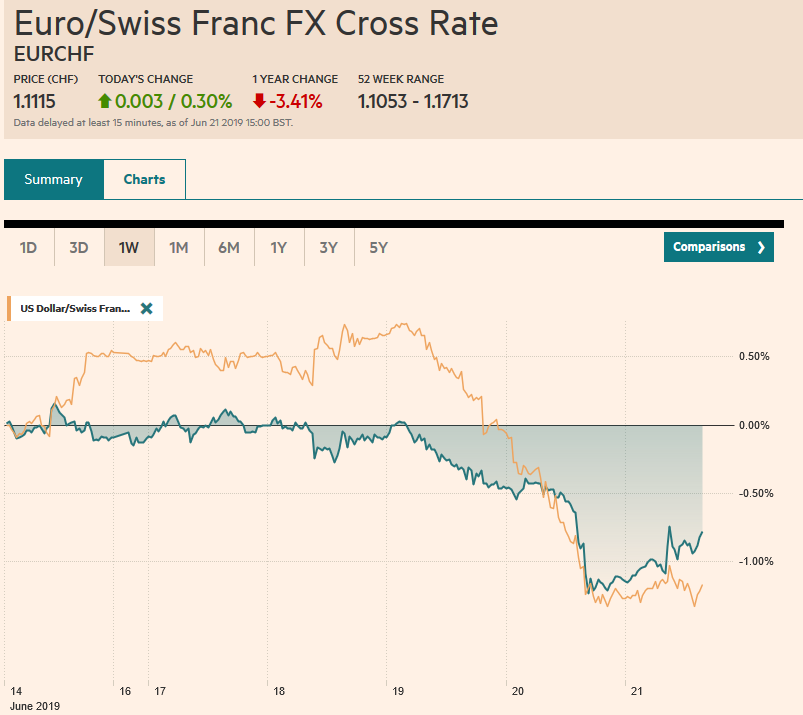

Swiss FrancThe Euro has risen by 0.30% at 1.1115 |

EUR/CHF and USD/CHF, June 21(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets are trading quietly ahead of the weekend. Equity markets are mostly narrowly mixed. Chinese shares extended their run, and the major benchmarks were up 4%+ on the week. Japan, Australia, South Korea, and India saw gains pared. European equities were edging higher, and the Dow Jones Stoxx 600 is holding on to around a 2% gain for the week. After closing at record highs yesterday, the S&P 500 is trading a little heavier in the electronic activity. News that the US was ready to strike Iranian radar and missile batteries but called it off at the last moment rattled investors. Japanese, Europe, and US 10-year benchmark yields firmed slightly, while Australia and New Zealand 10-year yields eased to new record lows. The dollar itself is also mixed, though the Dollar Index is trading a little below its 200-day moving average (~96.65) in the European morning. The Turkish lira and South African rand are leading most of the emerging market currencies lower. Gold briefly extended its gains above $1400 for the first time since 2013 before pulling back in Europe. It is poised for its largest weekly gain (~3.5%) in three years. |

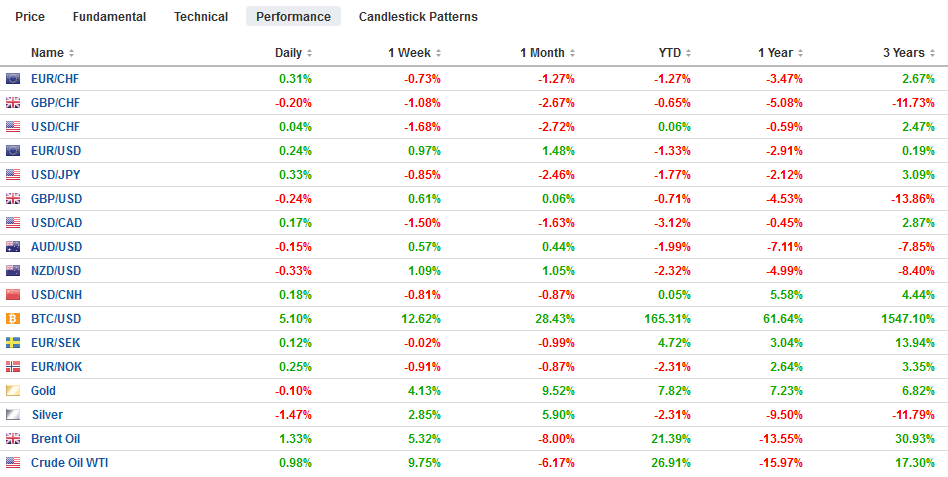

FX Performance, June 21 - Click to enlarge |

Asia Pacific

Japan reported softer price pressures and a June flash manufacturing PMI that remained below the 50 boom/bust level. Headline CPI slipped to 0.7% in May from 0.9% in April as economists expected. The core rate, which excludes fresh food, eased to 0.8% from 0.9%. When fresh food and energy are excluded–more like the US and Europe core measures–prices were up 0.5% from a year ago rather than 0.6% as was the case in April. The flash manufacturing PMI fell to 49.5 from 49.8 and reported the first drop in new orders since June 2016. Output remained firm, and the order backlog is being absorbed, setting the stage for a potentially difficult Q3. A bright spot may be services. The tertiary index for April jumped 0.9% after a 0.5% decline in March. This is the largest increase since last October. There are no policy implications from today’s reports. The bar to BOJ action appears a bit higher than in the US and Europe.

The dollar tested the JPY107 level, which was our technical objective of the double top pattern. A $1.2 bln option struck there that expires today may have helped it steady. The greenback bounced, but optionality may still impact activity today. In Europe, the dollar is above the JPY107.25 strike that holds a $605 mln expiring option and is near JPY107.50 and a $1.4 bln option that will be cut. If those are not sufficient to contain the dollar, there are $2.7 bln in options between JPY107.70-and JPY107.75 that should do the trick. The Australian dollar edged higher to a new high for the week (~$0.6940) to flirt with the 20-day moving average before a light bout of profit-taking pushed it a bit lower. Initial support now is seen near $0.6900. The dollar entered the gap created against the Chinese yuan after tariff ceasefire abruptly ended in early May. The gap was not closed (extends to about CNY6.8265) and the dollar recovered to finish the local session near CNY6.8770. The dollar fell about 0.7% against the yuan this week, the biggest decline in five months.

Europe

There are three main talking points from Europe today: The Tory leadership contest in the UK, the flash PMI, and developments in negotiating the next European Commission. The first is the easiest to address. Over the next several weeks, the 160k or so members of the Conservative Party will now choose between Johnson and Hunt to succeed May. After the candidate is selected, the real challenge, May’s challenge returns. The EC refuses to renegotiate the Withdrawal Bill. There seems to be no agreement in the UK what to do next. Chancellor of the Exchequer Hammond said the only way to break the deadlock may be new elections or a referendum. PredictIt.Org has a 2/3 chance that the UK does not leave at the end of October.

The flash eurozone PMI was not nearly as poor as Draghi’s pessimism would have suggested. The composite PMI for the eurozone as a whole rose to 52.1 in June from 51.8 in May. It is the highest since last November. Manufacturing edged higher (47.8 from 47.7), which reflects the global trade headwinds, while the service PMI rose to 53.4 from 52.9, the best in seven months. Germany saw both manufacturing and service sector PMI increase, but in a statistical quirk, the composite was unchanged at 52.6. France did better. Both reports were stronger than expected, and the composite rose to 52.9 from 51.3. The takeaway from the flash PMI is that there has been steady even if slow improvement through Q2. The real sector did better than the surveys suggested in Q1 and might do a bit worse than the surveys suggest in Q2. Much depends on Q3 data.

European leaders failed to resolve their differences over the configuration of the next European Commission. What was agreed upon was none of the candidates leading the three main political groupings (“Spitzenkandidaten”) were acceptable, and it is back to square one. Debating and horse trading is likely over the next few weeks.

The euro is consolidating yesterday’s surge and is straddling the $1.1300 level, where 2.4 bln euro of options will be cut today. Since yesterday’s high, a little above $1.1315, was recorded, the euro has not been below $1.1270. That said, the US market has not seemed to be as dollar-negative as the Asian and European sessions in recent days. There is a roughly 530 mln euro expiring option at $1.1325 that appears to be safe. After reaching $1.2725, sterling stalled just shy of the nearly GBP500 mln option struck at $1.2730 that will roll off today. Now even the GBP235 mln option at $1.2700 looks safe as sterling is pushed toward $1.2660 following some deterioration of the government finances. Initial support now may be seen near $1.2640.

America

US and Chinese negotiators have not spoken for six weeks. Three days for the G20 meeting they will meet in Osaka and prepare for the two presidents’ meeting. Many observers seem to think that because there has been an agreement, according to the media, on around 90% of the issues, a resolution is likely. That framing may be misleading. All asks are not equal. There is low hanging fruit that may be easily picked. These are what typically get agreed upon first. The more contentious issues are what is left. Your heart is around the size of your fist, but its size does not determine its importance. The other problem with the framing is that it continues to regard China as a big Japan. Several of the US negotiators, including Lighthizer, cut their teeth negotiating with Japan in the 1980s, which at the time was accused many of the same violations as China is today, including stealing American technology and beggar-thy-neighbor currency policy. Also, the voluntary export restrictions and orderly market agreements that the US deployed to address Japan’s challenge, were permissible under GATT, but are not under the WTO.

China is not just bigger than Japan, it is qualitatively different. Outside the US, many countries’ powers are primarily in one area. The Soviet Union’s military might was its only real claim to superpower status. Germany and Japan are economic powers. They hardly matter in global military terms. China possesses several elements of power, though unlike the US, it has one foreign military base (Djibouti) and has not attacked any foreign country in a generation. China need not be a rival. It could be a partner. They could divide the world into spheres of influence the way that the Yalta Conference divided Europe. But the die has been cast, and it will not show up in the things that economists count.

Many observers argue stocks and bonds are telling two different stories. Given the capital flows and sophisticated participants, it seems reasonable that the difference would have been arbitraged away. It seems more likely that the markets tell that same story. The rally in stocks might not be an expression of economic optimism, but the belief that interest rates (as an alternative investment) will stay lower for longer, which is the same thing, arguably the debt market seems to be saying. The US reports existing home sales, where are expected to increase around 2% after falling three of the first four months of the year. Lower interest rates may attract new buyers. The flash June PMIs are also due, and expectations are for little change. Disappointment could weigh on the dollar. Canada reports April retail sales. After the outsized rise of 1.1% in March, any gain would be impressive. Canada joins Norway to be among the few major central banks that are not considering easing policy. The Canadian dollar has risen in the past four sessions but may struggle ahead of the weekend amid the general consolidative mood. There is a $2.3 bln option at CAD1.3220 that will be cut today. The dollar spiked below MXN18.90 yesterday but closed back above MXN19.00. It is pushing a little higher today. Initial resistance is pegged near MXN19.10.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,EUR/CHF and USD/CHF,Europe,newsletter,Trade