Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Investors have worked themselves into a lather. Equities crashed in Q4 last year amid on corporate earnings and concerns about growth. The Fed’s tightening decision in December was made unanimously. The above-trend growth, the preferred inflation measure was near target, unemployment was the lowest in a generation and real rates were historically low.

There are myths in the market, like the Plunge Protection Committee, or that the Fed targets the core rate of inflation. One such myth that some Fed officials have helped to perpetuate is that the central bank is a murderer. That it kills expansions. It may have been true, but it has reformed.

Indeed, it was the Federal Reserve under Paul Volcker, a market favorite, that was last murdered an expansion. The last three business cycle downturns were preceded by a financial crisis and were not caused by too tight of Fed policy. Think about it: The S&L crisis, the tech bubble, and the Great Financial Crisis, which one did the Fed tightening spur?

That is another myth the Fed has helped to perpetuate. It often refers to its dual mandate. Others do too. Full-employment and price stability. But the truth of the matter is the there is a third mandate and the fact that it is often left out is revealing (affirmation through negation). It is financial stability.

II

Market fundamentalism is as dangerous as all fundamentalisms. It is both an exaggeration and simplification. It exaggerates the market’s function as the greatest aggregator of information. It oversimplifies ignoring other relevant factors and often assumes what it has to prove, namely that the market is always right. While nearly constant incremental movements are the norm, it is prone to lurches, overshoot, and reversals.

What is the yield curve telling us? What is the bond market telling us? These are the question economists, investors and policymakers are asking. Many market fundamentals know the answer. The precipitous fall interest rates and inversion of the yield curve reflect investors’ anticipating a recession. Q.E.D.

Yet the situation is considerably more complicated. Right alongside the “fair value” model we have in our heads or on the spreadsheet needs to be another model, albeit, perhaps less formal. It would include the myriad of factors that are not about a macroeconomic assessment. When it comes to US yield, this means it is not just asset managers but also the US Treasury debt managers who determine the precise issuance. It would include the attractiveness of US yields, regardless of one’s view of the economy, given that nearly a fifth of all bonds has a negative yield, which is more than $10 trillion.

Narratives focus almost exclusively on investors, and much of the media coverage of the markets make it seem as if hedge funds and other risk takers are the market. What about hedgers and passive investors who are forced into action by other developments? The mortgage holder faces early pre-payment risk due to the decline in interest rates may be forced to hedge. It may be like an echo chamber, where the echo produces its own echo. Previously the conventional wisdom was that central banks bond-buying drove down yields and dampened volatility. Now on a net basis, central bank buying has ceased, and yields have plunged.

The unwinding of the Fed’s balance sheet, some suggested, would push up interest rates. Since the Fed’s balance sheet operations reached terminal velocity, the 10-year yields have dropped around 85 bp. No one would buy Italian bonds once the ECB stopped, we were told by top economists and op-ed writers, and yet the 10-year BTP yield has fallen nearly as much as US yield over the past six months, as the ECB tapered and then ceased buying altogether. In the six months before, while the ECB was buying, the yield had risen by more than twice that.

III

Market fundamentalism also leads to exaggerating the economic weakness. The data is read through market prices, and modernity appears to have exorcized any discussion of value as a philosophic demon and its fanciful language that coverup for personal desires, passions, and moralizing.

The gap between the 1.5 rate cuts the market is discounting this year for the Federal Reserve stands in stark contrast to not only Fed’s forecasts (dot plot) but also the FOMC statement, which is its primary communication tool. That gap needs to be closed. Federal Reserve speakers, including the perceived doves like Bullard and Kashkari, are already using their speaking opportunities to emphasize the underlying strength of the US economy and the neutral stance of the central bank.

Market fundamentalists often make their claims almost an article of faith. Let’s treat our ideas as hypotheses. Our hypothesis many participants are exaggerating the economic weakness and that next week’s US economic data will help underpin the Fed’s message that a rate cut is not warranted.

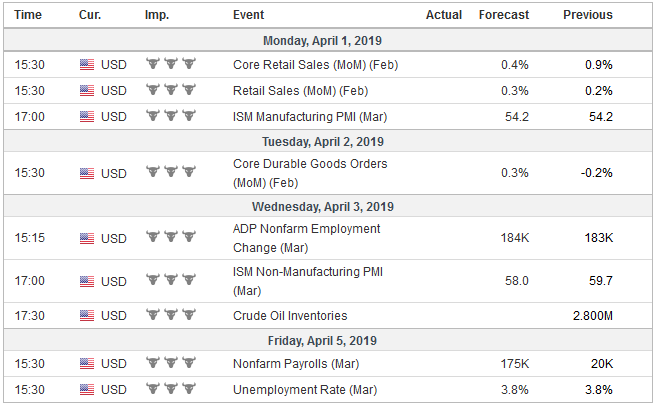

United StatesSpecifically, the January surge in US retail sales was not the capitulation of American shoppers. Consumption likely like grew further even if at a more moderate pace. Auto sales likely firmed after declining in January and February. Most important, the 20k rise in February non-farm payrolls was a fluke. It will not be repeated. It is more likely that the March jobs growth snaps back toward trend. The six and 12-month averages are 200k, +/- 10k. Hourly earnings growth should remain near cyclical highs, and the work week may have expanded, which given the size of the workforce, swamps the month-to-month net change in employment. The Atlanta Fed’s GDP tracker for Q1 began March below 0.5% and finished the month at 1.7%. The New York Fed’s model is at 1.3% after stating the month less than 0.9%. The median forecast of the Bloomberg survey is smack between the two at 1.5%. |

Economic Events: United States, Week April 01 - Click to enlarge |

IV

ChinaWe see preliminary signs that the Chinese economy may have also found a base. Even if it is not evident in the PMI reports, the household and corporate tax cuts that begin now and other stimulus measures, suggest it will be forthcoming shortly. We put emphasis on Xi’s political will and interest to avoid an economic weakness in this the 70th anniversary of the Revolution, which would give the US an advantage in negotiations. Speculation that China will get more serious about the trade negotiations now the Mueller investigation is complete appears far from the mark. The media has delivered a steady stream largely repetitive stories quoting senior US officials talking about the progress that is being made. We have been led to believe that the main problem is in enforcement because the US rejects the currently preferred use of independent panels. The Trump Administration sees what previously had propagated as the rule of law as a sinister erosion of US sovereignty. It wants to reserve the right to unilaterally respond commensurately with the hard if no timely resolution of a conflict is found. |

Economic Events: China, Week April 01 - Click to enlarge |

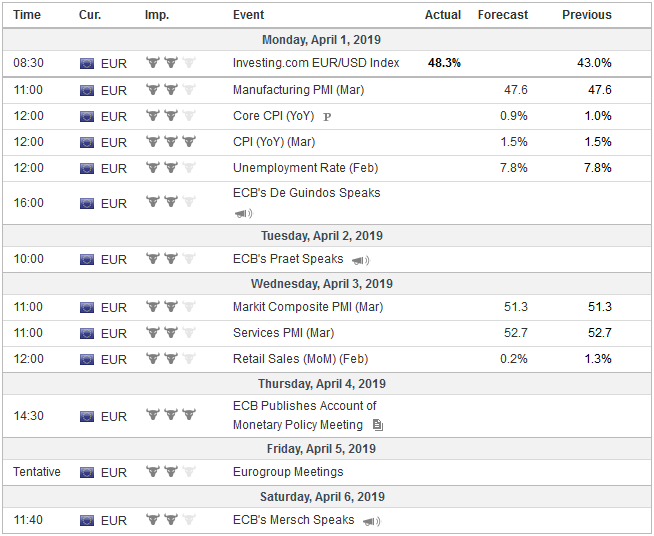

EurozoneEurope’s economy may also be finding a base. The current slowdown centered in the core and especially Germany. Yes, Italy contracted in H2 18, even in the best of times it did has not grown quickly. Since 2011, the Italian economy has experienced only three quarters in which growth exceeded 0.4%. The more immediate problem is Germany, and the corner appears to have been turned. |

Economic Events: Eurozone, Week April 01 - Click to enlarge |

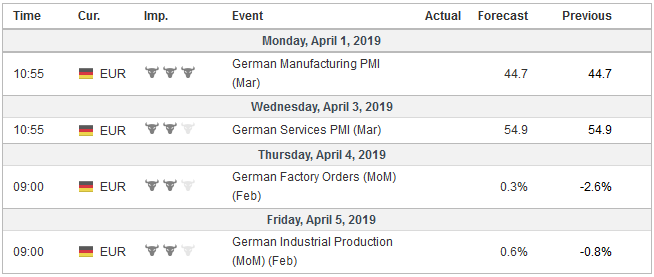

GermanyLast week, the German IFO survey surprised on the upside and seemed to contradict the dismal flash PMI.The February unemployment rate slipped to 4.9%, the lowest since unification. Economists had cautioned that the jump in January retail sales stole from future sales and the median forecast in the Bloomberg survey was for a 1.0% decline in February. Instead, they rose 0.9% (and the January gain was revised down from 3.3% to a still-heady 2.8%). The two-month gain matches the strongest in five years, which itself was the best since mid-2011. More evidence is that the European locomotive is getting back on track is likely in the coming days when Germany reports February factory orders and industrial production figures. Both should recover from the steep slide in January (2.6% and 0.8% respectively). Modest gains are expected suggesting the recovery is gradual. The recovery is not even, and spring may come to France later. |

Economic Events: Germany, Week April 01 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week April 01 - Click to enlarge |

Tags: China,Federal Reserve,Germany,Interest rates,newsletter,United States