Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There are three broad forces of movement in the week ahead: the equity market performance, political developments, and economic data.

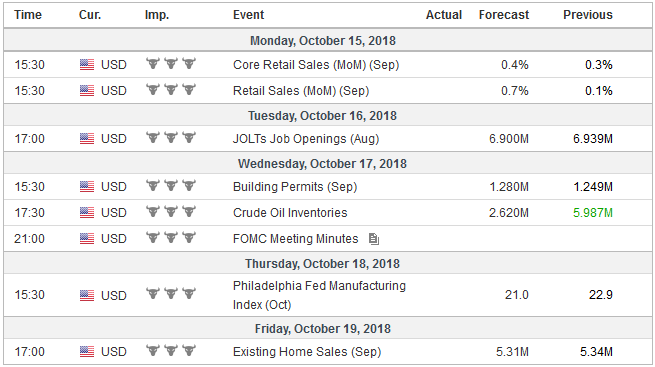

United StatesIt was a tumultuous week for equities, and there was not clear or obvious trigger. With US bond yields and equities trending higher this year, there does not seem to a reason why it ended last week. Similarly, the recovery before the weekend, which lifted the S&P 500 back above its 200-day moving average, did not appear to have a trigger. Instead of beginning a sustained correction in the stock market, last week may have been the climactic finish to a three-week slide that took the MSCI World Index (of developed countries) down 7.25%, and its Emerging Markets Index 9.5%. The Dow Jones Stoxx 600 fell about 6.7%, while the S&P 500 fell 5.5%. Remember most of the benchmark indices were below their 200-day moving averages before last week’s drop. Given that broad economic forces have not changed, and that the S&P 500 closed firm ahead of the weekend, boost the chances that this was a short-lived hiccup in the markets. If this assessment is too optimistic, the next mile marker in the S&P 500 is 2645, which would present a 10% pullback from the highs. Below there are the lows from February’s downdraft around 2530. The equity market decline appeared to fuel the dollar sales last week, and the better performance ahead of the weekend coincided with gains in the greenback. Within the current context, stronger stocks are good for the dollar as it does not prevent the Fed from continuing to gradually hike interest rates. The market does not expect the stock market or political pressure to push the Fed off its course. The current average effective Fed funds rate is 2.18%. The implied yield of the December 2019 Fed funds futures has eased five basis points since the end of September from 2.81% to 2.76%. Growth this year is about one percentage point faster than it had anticipated in September 2016, and unemployment is more than 0.5 percentage points lower than it had expected. A December hike would put the fed funds target a quarter point higher than the median Fed officials signaled. The US Treasury report about the international economy and the foreign exchange market is expected to be released in the week ahead. Even though by the quantitative metrics provided by Congressional legislation, most observers recognize that China does not meet the threshold of “manipulation.” the unorthodox Administration could have done it anyway as part of a tactic in the larger effort to get China to change behaviors in trade and economics, and the US finds objectionable. It is true that the yuan has weakened this year, but some have most currencies against the dollar. It hardly seems to require a unique explanation. Simply put, the interest rate premium China offers has narrowed, the economy is slowing, and its equities are in a bear market (the Shanghai Composite is off nearly 30% since the January highs). |

Economic Events: United States, Week October 15 - Click to enlarge |

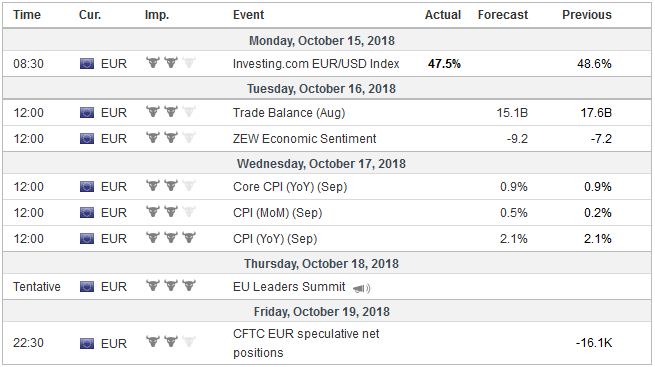

EurozoneSeveral political events pose headline risks in the week ahead. The outcome of Bavaria’s election is unlikely to have much market impact. The CSU is expected to lose its majority, which will require a coalition government going forward, and between it, and the coalition partner on the national level, the SPD may not have a combined majority. Indeed, the AfD may surpass the SPD, but the Greens could become the second largest party. The outcome is important for the implications for the national politics and the erosion of the two main parties. Italy is to submit its budget to the EC at the start of the week. It has already met a cool response, and an excessive deficit procedure may be initiated in response, which requires the government to provide a plan for corrective actions. This can be a back-and-forth processes for some time. However, it is not clear that the market has completed the adjustment to the new supply, indebtedness, and risk of a policy mistake/confrontation with the EU. A rise toward 4% in the 10-year yield cannot be ruled. The widening of the Italian premium over Germany tends to correspond to a weakening of the euro (0.80 inverse correlation past 120 days). The EU meets on October 17 and will get an update on the status of negotiations with the UK. Ideally, before the summit is over the next day, a decision will be made that there has been sufficient progress on the Irish border issue to call for a special summit next month to finalize an agreement. If this happens, perceptions of the risk of a hard exit, without a deal, will ease and sterling can outperform at least the euro if not the dollar as well. At the same time that the UK and EU may be closing in on an agreement, Prime Minister May’s challenges within her cabinet and Parliament intensify. It is possible a cabinet official or two resign in protest. The government also has tested the waters to see if sufficient Labour support can be peeled off against the wishes of its leadership, to offset the Tories that prefer no agreement. There seems to be only one compelling reason why there has not been a leadership challenge. No one thinks they can win the challenge or Brexit. |

Economic Events: Eurozone, Week October 15 - Click to enlarge |

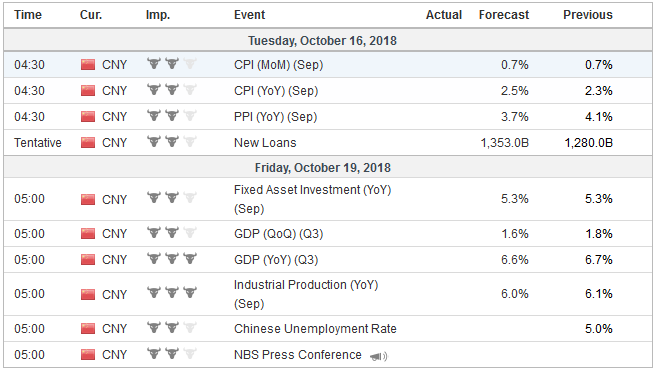

ChinaTo the extent that China has intervened, it appears to have done so to slow the descent. It has drawn the line at CNY7.0. We suspect that over the medium-term the yuan may go through there, in which case, the target would be around CNY7.15. The latest press reports suggest that the Treasury Department is unlikely to cite China as a manipulator and that President Trump will meet President Xi on the sidelines of the G20 meeting at the end of next month. The Chinese trade data suggests is difficult to read due to the likely attempt to beat the imposition of new tariffs, but through September, the direct impact seems marginal. This constructive news stream coupled with the strong close ahead of the weekend suggests reasons to take a step back from the edge of the abyss and take pressure off the yuan. The trade data reported before the weekend also showed a record surplus with the US, a reminder that the underlying source of antagonism remains. Turning to economic data, the US reports retail sales and industrial production. The data are expected to be consistent with above-trend growth. The housing market is interest-rate sensitive and some slowing is evident. There are also press reports of mortgage lending departments at banks being downsized. Housing starts and existing home sales will be reported. The August TIC data will also be released. Through July, the TIC shows a monthly average of $95.6 bln of portfolio inflows into the US. This is more than twice the average for the same period last year (~$41.4 bln) or for last year as a whole (~$35.5 bln). The repatriation of earnings from overseas by US corporations appears to be playing a significant role. |

Economic Events: China, Week October 15 - Click to enlarge |

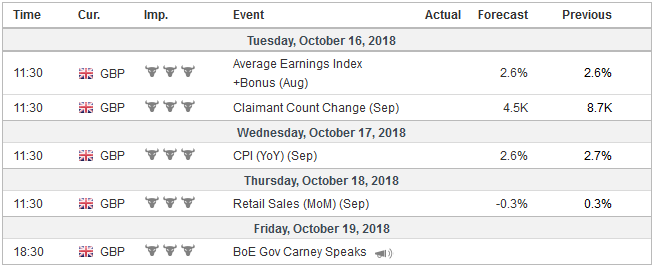

United KingdomThe UK reports employment, inflation, and retail sales. From a high level, the labor market is steady as is earnings growth. Price pressures are easing a little, and retail sales are expected to have softened, though the base effect, suggests that the year-over-year rate may increase. Investors recognize a chance that the BOE could hike rates before Brexit, but do not see it as the odds-on favorite scenario. The market has discounted more than a 50% chance of the next increase rate increase in Q2 19. It is nearly completely priced in by the end of Q3 19. |

Economic Events: United Kingdom, Week October 15 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week October 15 - Click to enlarge |

Japan

Japan will likely report its third consecutive monthly trade deficit in September, the longest spell in three years. Exports are slowing, while high oil prices are helping keep imports strong. Better news may be on the inflation front, where September CPI, excluding fresh food, which is the measure the BOJ targets may creep up to 1.0% matching the cyclical high seen in February. Japan’s weekly MOF portfolio flow data may be of interest after foreign investors bought the most Japanese stocks since at least the early 1990s in the week ending October 5. It was the second consecutive weekly purchases that snapped a nine-week divestment run.

The market is discounting more than a 90% chance of a Bank of Canada rate hike when it meets on October 24. The upcoming data includes retail sales (firmer), and CPI (softer) are unlikely to persuade the market to reconsider. The Canadian dollar was the weakest major currency last week, losing about 2/3 of one percent. All the other currencies, but the Swiss franc, rose against the US dollar. Although Canada’s stock market held up a little better than the S&P 500, Canada’s coupon curve outperformed the US, resulting in wider differentials. There are a couple of other developments in Canada to note. Later this month, Canada will impose tariffs on aluminum to deter product that from being deflected by the US tariffs. Canada’s heavy crude that is rich in bitumen is selling for nearly $50 a barrel less than WTI and is reportedly attracting Chinese interest.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,newsletter