Summary

Stock MarketsIn the EM equity space as measured by MSCI, Hong Kong (flat), South Africa (flat), and China (-0.2%) have outperformed this week, while Mexico (-5.9%), Brazil (-5.2%), and Turkey (-4.7%) have underperformed. To put this in better context, MSCI EM fell -1.7% this week while MSCI DM fell -0.5%. In the EM local currency bond space, Philippines (10-year yield -6 bp), India (-4 bp), and Czech Republic (-2 bp) have outperformed this week, while Turkey (10-year yield +109 bp), South Africa (+13 bp), and Poland (+12 bp) have underperformed. To put this in better context, the 10-year UST yield fell 2 bp to 2.96%. In the EM FX space, EGP (+0.4% vs. USD), PHP (+0.4% vs. USD), and PKR (flat vs. USD) have outperformed this week, while ARS (-5.8% vs. USD), TRY (-4.7% vs. USD), and MXN (-3.1% vs. USD) have underperformed. To put this in better context, MSCI EM FX fell -0.6% this week. |

Stock Markets Emerging Markets, May 07 - Click to enlarge |

IndonesiaBank Indonesia is taking measures to stabilize the local bond market. The bank said it will buy bonds in the secondary market if fresh selling pressures emerge. It added that it is open to reviewing its scheduled borrowing this year, noting that it has already completes nearly 50% of its gross borrowing target at the end of April. The bank failed to meet its sales target in the previous two auctions. PhillippinesThe Philippine central bank is tilting more hawkish. Governor Espenilla said that he was “very concerned” with April CPI data (4.5% y/y and further above the 2-4% target range. This follows comments from him earlier this week expressing concern that price pressures are spreading into the wider economy. Next policy meeting is May 10 and markets are pricing in a 25 bp hike to 3.25%, the first move in this tightening cycle. Czech RepublicCzech National Bank cut its inflation forecasts and suggested that the pace of tightening will slow. The bank sees inflation slowing to 1.5% in Q4 2018 vs. 2.2% forecast in February. Governor Rusnok noted that the new forecast implies that the next rate hike will happen near year-end, “say, in the fourth quarter.” He added that an earlier hike can’t be ruled out if the situation changes. One board member voted to raise rates while six voted against. TurkeyThe Turkish government is loosening fiscal policy to drum up popular support. More than 12 mln retirees (about 15% of the total population) will get a payment from the government a week before elections on June 24. The ruling AKP said it will be the first of two payments tied to national holidays. The two payments of TRY1000 liras each will cost Turkey an additional $5.9 bln. The AKP also announced planned measures to forgive debt erase interest payments and restructure fines, taxes, and social security payments. S&P downgraded Turkey to BB- with stable outlook. It noted that “There is a risk of a hard landing for Turkey’s overheating, credit-fueled economy.” S&P has been the most negative on Turkey and we agree with this move. Our own sovereign ratings model April shows Turkey’s implied rating rose a notch to B+/B1/B+ in April, reversing last quarter’s drop. However, Turkey still faces strong downgrade risks to its BB-/Ba2/BB+ ratings. ArgentinaArgentina officials are taking significant measures to support the peso. The central bank has raised rates three times this past week to 40% currently. Foreign reserves dropped $5 bln just last week alone, a pace of FX intervention that clearly couldn’t be sustained. The government also announced fiscal tightening meant to narrow the primary deficit to -2.7% of GDP this year vs. -3.2% previously. BrazilBrazil central bank made a subtle shift in its FX intervention strategy. It announced that it would offer more swaps than those expiring June 1, but did not say exactly how much more would be offered. In the past, it would simply issue a set amount of new swaps when FX markets got too unstable. |

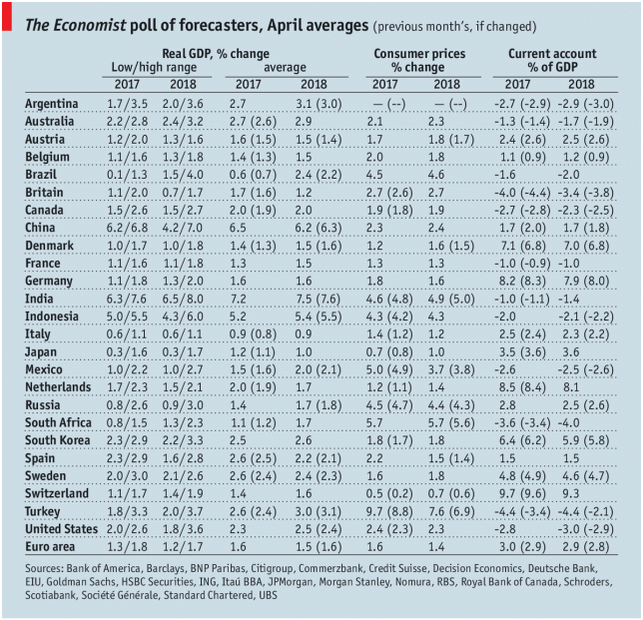

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, April 2018 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin