Stock MarketsEM FX ended Friday on a firm note, capping off a generally softer week overall. TRY and PHP were the best performers last week, while CLP and ZAR were the worst. US core PCE, ISM manufacturing, FOMC meeting, and jobs data all pose risks to EM this week. We remain a bit defensive on risk assets in general now. |

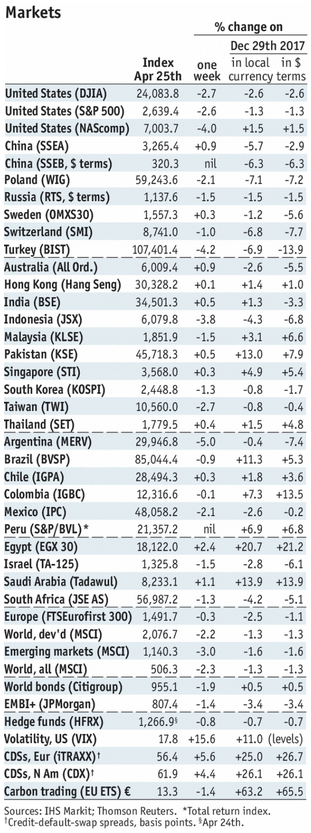

Stock Markets Emerging Markets, April 25 - Click to enlarge |

KoreaKorea reports March IP Monday, which is expected at -1.6% y/y vs. -6.4% in February. It then reports April trade Tuesday, with exports expected to rise 3.9% y/y vs. 6.1%in February. April CPI will be reported Wednesday, which is expected to rise 1.5% y/y vs. 1.3% in March. If so, inflation would remain below the 2% target and should allow the Bank of Korea to tighten modestly this year. Next policy meeting is May 24, no change is expected. March current account data will be reported Friday. ChinaChina reports official April manufacturing PMI Monday, which is expected at 51.3 vs. 51.5 in March. Caixin will report its measure Wednesday, which is expected at 50.9 vs. 51.0 in March. For now, the mainland economic outlook remains solid but further softening would be concerning. TurkeyTurkey reports March trade Monday, which is expected at -$5.8 bln. The central bank will also release its quarterly inflation report that day. April CPI will be reported Thursday, which is expected to rise 10.45% y/y vs. 10.23% in March. If so, inflation would move further above the 3-7% target range. The central bank just surprised with a larger than expected 75 bp hike in the Late Liquidity rate. With the lira remaining under pressure, more tightening will likely be needed at the next policy meeting June 7. South AfricaSouth Africa reports March trade, budget, money, and private sector credit data Monday. While the economic data have been improving, we think the SARB would like to continue cutting rates. Much will depend on the rand. If it remains firm, we think another 25 bp cut to 6.25% is possible at the next policy meeting May 24. MexicoMexico reports Q1 GDP Monday, which is expected to grow 1.7% y/y vs. 1.5% in Q4. Inflation has been falling even as the economy remains sluggish. However, we doubt that Banco de Mexico can contemplate any easing until after the July elections. Next policy meeting is May 17, no change is expected. BrazilBrazil reports March consolidated budget data Monday. The economic recovery has helped boost the budget data, but lack of pension reform means that this cyclical improvement will not be permanent. April trade will be reported Wednesday and March IP will be reported Thursday. The market is looking for one last 25 bp cut to 6.25% at the next COPOM meeting May 16. ThailandThailand reports April CPI Tuesday, which is expected to rise 0.9% y/y vs. 0.8% in March. If so, inflation would remain below the 1-4% target range and should allow the Bank of Thailand to remain on hold this year. Next policy meeting is May 16, no change is expected. PeruPeru reports April CPI Tuesday, which is expected to rise 0.7% y/y vs. 0.4% in March. If so, inflation would remain below the 1-3% target range and should allow the central bank to continue cutting rates this year. Next policy meeting is May 10, and a 25 bp cut to 2.5% is likely. IndonesiaIndonesia reports April CPI Wednesday, which is expected to rise 3.5% y/y vs. 3.4% in March. If so, inflation would remain in the bottom half of the 3-5% target range and should allow Bank Indonesia to remain on hold for the time being. However, the weak rupiah is a growing concern. Next policy meeting is May 17, and a hawkish surprise is possible. PolandPoland reports April CPI Wednesday, which is expected to rise 1.5% y/y vs. 1.3% in March. If so, inflation would be right at the bottom of the 1.5-3.5% target range and should allow the central bank to keep rates steady this year. Next policy meeting is May 16, and no change is expected. Czech RepublicCzech National Bank meets Thursday and is expected to keep rates steady at 0.75%. CPI rose 1.7% y/y in March and is in the bottom half of the 1-3% target range. The central bank has been hiking rates every other meeting since it started the cycle in August. While that points to another hike at this meeting, there is a possibility that lower than expected inflation delays that move until the June 27 meeting. ChileChile central bank meets Thursday and is expected to keep rates steady at 2.5%. Earlier that day, Chile reports March retail sales. CPI rose 1.8% y/y in March, below the 2-4% target range. While the central bank has signaled an end to the tightening cycle, low inflation will allow it to resume cutting if the economy were to slow sharply. PhilippinesThe Philippines reports April CPI Friday, which is expected to rise 4.5% y/y vs. 4.3% in March. If so, inflation would move further above the 2-4% target range and should force the central bank to start the tightening cycle soon. Next policy meeting is May 10, no change is expected but we see growing risks of a hawkish surprise. ColombiaColombia reports April CPI Saturday, which is expected to rise 2.96% y/y vs. 3.14% in March. If so, inflation would fall below the 3% target (but within the 2-4% target range). This should allow the central bank to continue cutting rates this year. The bank just cut rates 25 bp to 4.25% last week and has been cutting every other meeting. Next policy meeting is May 31, and steady rates are likely. |

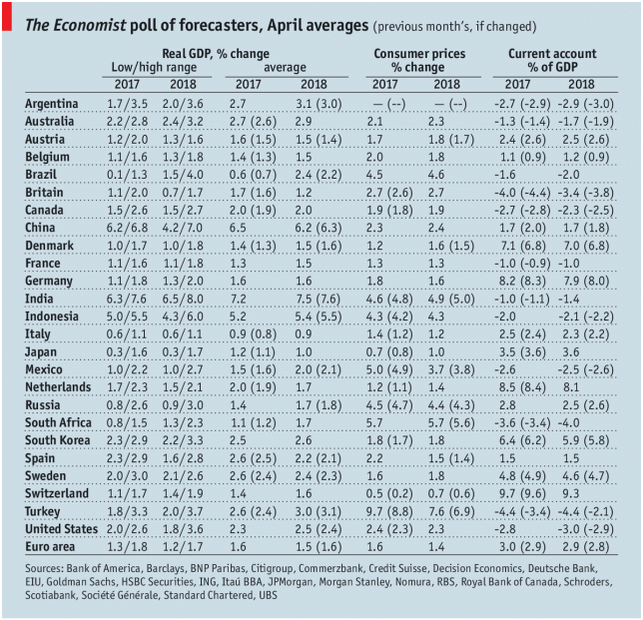

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, April 2018 Source: economist.com - Click to enlarge |

Tags: Emerging Markets,newslettersent,win-thin