Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Worries about a trade war appear to have eased, at least for the moment, but that does not make investors worry-free. The concerns have shifted toward rising US interest rates, perhaps more than anything else, but general anxiety seems elevated.

The unpredictableness of Trump Administration is not helpful, and even though oil prices recovered, they did react quickly, losing a dollar a barrel in response to his tweet. There have been inexplicable comments about currency manipulation, individual companies, and the back-and-forth on TPP. It is very much on asset managers’ minds even if it is difficult to model.

North Korea’s announcement, ahead of the North-South summit that it would close a missile site and refrain from further tests sounds like good news and favorable for risk assets at the start of the new week. It is easy to accept at face value as a wholly favorable development for denuclearization. That would be naive.

First, this is not the first time North Korea has made such offers. A few years ago, it agreed on a test moratorium in exchange for US aid but then proceeded to test a long-range rocket. Second, if North Korea has acquired the capability to strike the US as it claims, then there is no urgency for further testing. It has a seat at the table. Third, the recent US strike in Syria (without UN authorization), increases the value of North Korea’s nuclear weapons. Crudely and simply put, countries with nuclear weapons are not attacked, and it must be assumed that North Korea recognizes that.

Equities have traded firmly in recent weeks. Europe’s Dow Jones Stoxx 600 has risen by about 4.2% in the four-week advance it carries into the new week. The MSCI Asia Pacific Index is up three of the past four weeks and has gained 1%. The S&P 500 has also risen in all but one of the past four weeks and has gained a net 3.1%. Earnings season continues, and big oil and pharma, European banks and Alphabet are featured. A strong earnings season is anticipated, so the bar to an upside surprise is high and disappoints are punished.

In the debt market, there are three notable developments. First, US rates have continued to trend higher. We estimate that more than half of the 25 bp rise in the US 10-yield this month reflects rising inflation expectations. The two-year yield has risen 19 bp. We note that dealers have had to absorb more of recent Treasury sales and need to adjust prices to liquidate their inventory. Second, the two-ten year US yield curve stabilized in the second half of last week, and many investors will be scrutinizing this week’s developments. Third, three-month dollar LIBOR sharp rise in recent months appears to be stabilizing.

The dollar appears to be finding better traction against both high-yielding currencies, like the Australian and New Zealand dollars, and lower yielding currencies like the Japanese yen and Swiss franc. The widening interest rate differentials translate into increased costs of shorting the dollar if it is not falling. The euro has been in a clear range for months, and the dollar rose to a two-month high against the yen.

Sweden’s Riksbank, the European Central Bank, and the Bank of Japan hold policy meetings in the week ahead. None are expected to change policy. However, there are nuances that could make a difference. The Riksbank may not change its projected policy path, but it may lift its inflation forecast. Note that the trade-weighted krona has fallen by nearly 6% over the past three months and is at its lowest level since 2009.

JapanThe Bank of Japan is committed to its current course, characterized by Qualitative and Quantitative Easing and Yield Curve Control. The significance of this meeting is that it will offer forecasts for FY20 for the first time. Currently, it projects (core) inflation to be 1.8% in FY19. The challenge is that in October 2019, the sales tax will be raised to 10% from 8%. The past two hikes have weakened the economy. An inflation forecast near 2% for FY20, excluding the effects of the tax increase, though seemingly optimistic, may support the yen, as it would be consistent with a move toward exiting the extraordinary monetary policy. |

Economic Events: Japan, Week April 23 - Click to enlarge |

EurozoneAt the start of the year, many market participants had been expecting a substantive evolution of the ECB’s statement and forward guidance to prepare investors for the end of the asset purchases. However, the economic data has disappointed, and inflation pressure eased. Consider that CPI averaged 1.5% in 2017, but 1.4% in Q4 17 and 1.3% in Q1 18. To be sure, we continue to expect the ECB to finish its asset purchases this year, but there is no great hurry to signal anything after September when the current purchase plan ends. We expect the ECB to eventually signal that it will taper further in Q4 18. However, such an indication may not come for a few more months. Turning to the economic calendar, one of the highlights will be the first formal look at Q1 18 GDP. From the eurozone, both France and Spain will report. French growth appears to have slowed sharply in Q1 to 0.4% from 0.7% in Q4 17. Spain looks largely steady at the 0.7% pace seen in Q4 17. The eurozone will also see the flash April PMI readings. The median expectation from the Bloomberg survey point to continued weakness. We are somewhat more optimistic and see the risk on the upside on ideas that the poor weather may have exaggerated the pace of the slowdown in Q1. |

Economic Events: Eurozone, Week April 23 - Click to enlarge |

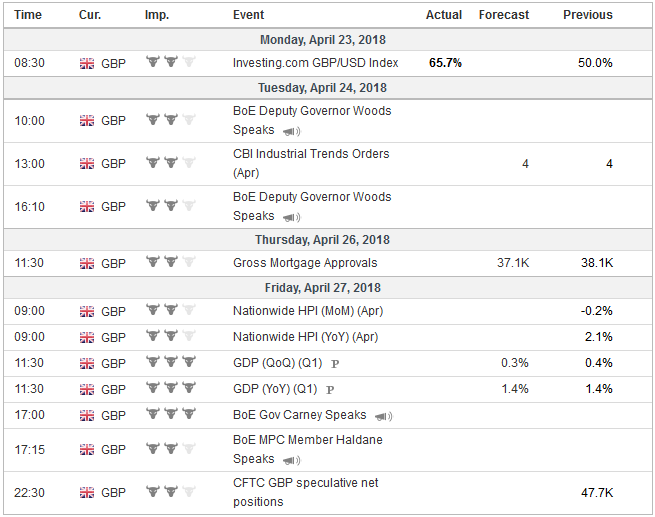

United KingdomThe UK also lost some economic momentum. After expanding by 0.4% in Q4 17, the UK economy slowed, and the risk may be on the downside of the median 0.3% forecast for Q1 18 GDP. The government’s strategy to leave the EU at the end of next March is arguably facing its largest challenge. The House of Lords amendment to the Withdrawal Bill called for remaining in the customs union. Although the action can be blocked by House of Commons, the upper house action appears to have emboldened the pro-EU forces. It is not clear yet how this plays out, or the impact on and from next month’s local elections, but it is important and may shape the investment climate going forward. In addition to greater continuity, remaining in the customs union would resolve the seemingly intractable problem of the Irish border. |

Economic Events: United Kingdom, Week April 23 - Click to enlarge |

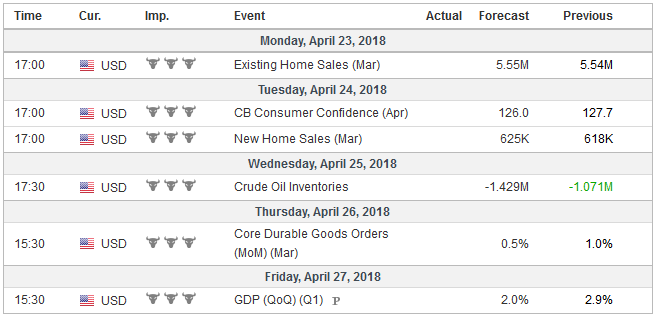

United StatesThe US reports its first look at Q1 GDP. It too appears to have slowed considerably. The latest estimate for Q4 17 GDP put it at a 2.9% annualized pace. The market is expecting 1.8%-2.0%. The Atlanta Fed’s GDPNow has it at the upper end of the market range, while the New York Fed’s GDP tracker sees it unchanged at 2.9%. As goes the US consumer, so goes the economy. Consumption rose at an annualized pace of 4% in Q4 18 and looks to have slowed to less than 1.5%, which would make it the slowest since Q2 13. We look for better growth in Q2 and continue to expect the Federal Reserve to look past the softness. The impact of the fiscal stimulus is expected to lift growth and prices. Bloomberg’s model still inexplicably sees a nearly 30% chance of a Fed hike next month. The CME’s model and our own work show practically no chance. |

Economic Events: United States, Week April 23 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week April 23 - Click to enlarge |

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,$JPY,$TLT,newslettersent,SPY