Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

No fewer than thirteen central banks meet in the week ahead. The UK and the US report the latest inflation figures, and the US and eurozone report industrial production. The eurozone sees the flash PMI for December, and the Japan’s latest Tankan business survey will be released.

Most of the central banks that meet will not be changing policy. Of the major central banks, the Bank of England, which hiked rates last month is hardly in a position to raise rates again. Headline inflation is slowing. Assuming next week’s November reading shows a 0.2% headline rate as expected, the three-month annualized pace would stand at around 2.4%, rather than 3.0% year-over-year pace.

SwitzerlandThe Swiss National Bank, whose currency is estimated by the OECD to be nearly 20% above fair value (PPP) is n where near prepared to move away from its extraordinary monetary policy. However, the worst of the economic impacts past. The economy accelerated for the third straight quarter, reaching 0.6% in Q3. Deflation has been arrested. Swiss CPI, using the EU-harmonized methodology stood at 0.8% year-over-year in November, up from -0.2% in November 2016. The Swiss franc has depreciated about 9.5% against the euro this year, and over the past couple of months, it has traded in narrow ranges near its lowest level since the cap was lifted in January 2015. After the Swiss franc, the Norwegian krone is the second most over-valued currency, according to the OECD (~17.25%). Price pressures fell sharply from Q3 2016 well into Q3 this year, but have stabilized more recently, and this is likely to born out with November update due out before the Norges Bank meets. Like Switzerland, the economy expanded by 0.6% in Q3, and although last week’s October industrial production disappointed (-1.4% month-over-month, and the September report was revised from -0.5% to -1.7%), manufacturing is firm. It expanded by a healthy 0.7% on the heels of the revised 2.8% gain in September. |

Economic Events: Switzerland, Week December 11 - Click to enlarge |

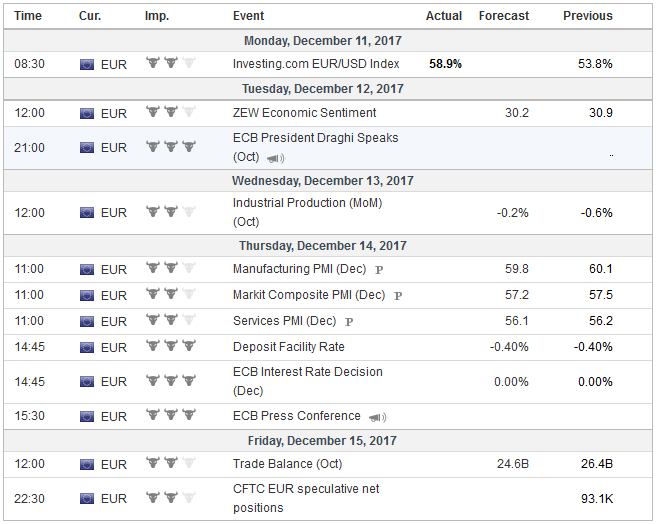

EurozoneThe ECB meeting is not important for what it officials will do. They fired their bazooka of sorts last month, and there is no need for new action now. The asset purchases will continue at a 30 bln euro pace starting next month through September 2018. There are voices that want a clear signal that September will conclude the purchases. The decision need not be made now, and we don’t expect it until next summer. There is no compelling reason to pre-commit. After being rebuffed on this front, the creditors may seek another line of attack. The ECB’s monetary stance is much broader than asset purchases. These other tools, like negative deposit rates, a zero interest rate on refi operations that are fully allocated, have been discussed much, except sequentially, that asset purchases are to stop first. There may be some push to consider an exit strategy for these too. The ECB’s corporate bond buying program may also come under scrutiny. Some creditors were not keen about it from the start. The ECB now holds bonds of more than one thousand companies. It appears that the Eurosystem may own a couple dozen bonds rated below investment grade (notional amount 21.2 bln euros), which account for about 16% of the corporate bond portfolio. Last summer, the ECB bought some of the 800 mln euros of bonds issued by the European branches of the South African-based retailer, Steinhoff, who is now mired in an accounting scandal. The company lost its investment-grade status, last week. The ECB may have to realize a loss on the bond, or if it is converted to equity (which may be the case), a loss on the stock, which the ECB’s own rules prohibit it from owning. Look for the ECB to be pressed by reporters on this issue. The ECB does not publish the amount of individual issues purchased, just the names of the credits. This is an area that greater transparency from the ECB may be helpful, and would seem like a small price to pay for buying the wrong bond. Some observers seem to be exaggerating the impact on the ECB and worry (for naught) about the central bank’s solvency. Consider the unbiased assumption that the ECB bought the roughly $130 bln of corporate bonds it holds were divided equally among the issues. That would be less than $130 mln average exposure, This is an important amount, but the loss needs to put in the context its balance sheet, and the seigniorage and profits it has accrued. It does not make for good press, the solvency of the ECB and the Eurosystem is not an issue. The ECB staff will update the macroeconomic forecasts. There are three things to watch. First, the staff will introduce the 2020 forecasts for the first time and hence will offer new information. Second, the CPI 2020 forecast will be particularly important. Will it forecast that the inflation target of near but lower than 2% be achieved? The 2019 forecast in September was 1.5%. Third, the data since the September forecasts suggest the staff may be tempted to revise higher their growth forecasts. This year’s was estimated at 2.2%, and it now looks closer to 2.5%. Next year’s growth was expected to be 1.8% and 1.7% in 2019. |

Economic Events: Eurozone, Week December 11 - Click to enlarge |

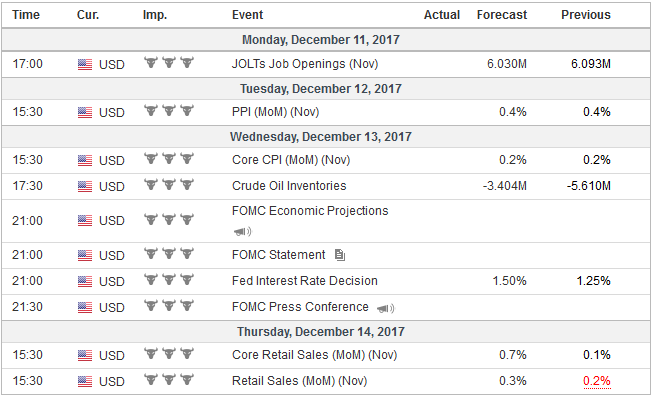

United StatesOf the major central banks, only the Federal Reserve is expected to change policy. The market has been reluctant to believe it, but the Fed will most likely deliver the third hike this year. This is precisely what it indicated it would do a year ago. This has not bolstered confidence in the Fed’s September dot plots that indicated that another three hikes in 2018 would likely be appropriate. The median forecast expected two hikes in 2019 and one in 2020. Investors are less sanguine. Looking at the Fed funds futures strip, a hike near the middle of next year. Only a little more than half of another hike is discounted by the end of 2018. As the composition of the Federal Reserve changes, the dot plot may take on greater significance. It will offer early insight into how the new members view the macroeconomic picture. The new forecasts will include the new member Quarles forecast. His dot will replace Fischer’s who stepped down after the September forecasts. Next year’s regional bank rotation of FOMC voting members will shift in a more hawkish fashion as the two main doves, the Minneapolis and Chicago Fed represents, move off. Investors will keep a watchful eye on fiscal policy developments. The reconciliation committee has its work cut out, and it is important to keep in mind that the final bill may look nothing like the House or Senate’s versions. We see two main risks. The first is that the delicate balance reached to pass the Senate may not be preserved in the final version. The second is unintended consequences. The final Senate version contained the Alternative Minimum Tax for corporations. This was not expected and may have spurred a sell-off of some particularly sensitive sectors until it was clear from the key Republican senators that would be dropped. Technology shares helped lift the broader indices in the second half of the week. Or consider the effort to address what is dubbed “base-erosion,” the transfer of taxable profits in the form of inter-company loans and interest payments. However, it would hit foreign banks particularly hard, and foreign banks play an under-appreciated role in financial disintermediation; in lending to households and businesses in the United States. This could pose a bigger threat to domestic financial conditions than the shrinking of the Fed’s balance sheet. |

Economic Events: United States, Week December 11 - Click to enlarge |

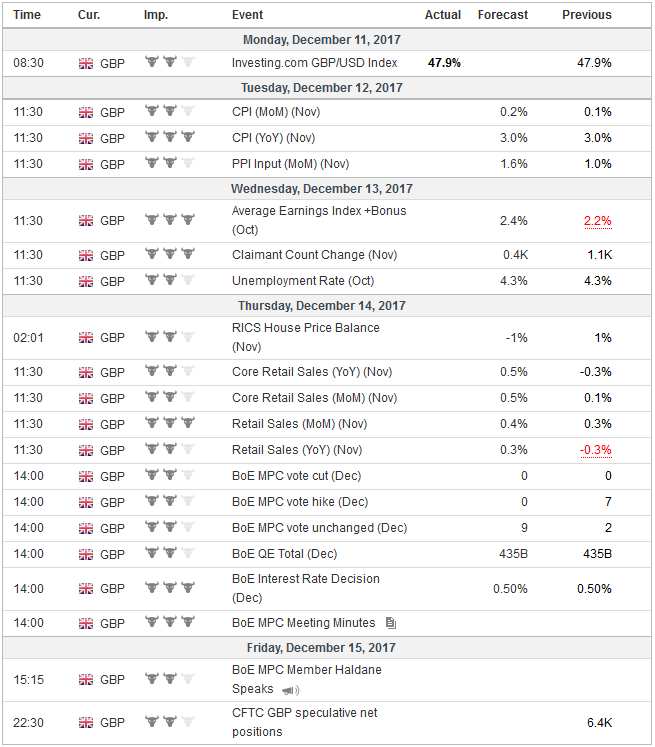

United KingdomThe EU Summit at the end of next week is most likely to grant that the UK has made sufficient progress to proceed to the next stage of negotiations-the future trade relationship. However, the general impression seems to be that it was a fudge and that key issues have not been resolved. The EU’s chief negotiator left no little doubt that the next stage is unlikely to be easier and may have less time. Barnier indicated that substantial discussions might not begin until February or March as the UK is not clear about its aims. He also indicated he is looking to conclude the talks by next October because of the lengthy approval process. The UK’s insistence that it intends to leave the single market and customs union narrow the range of post-Brexit trade relationships that are realistically viable. |

Economic Events: United Kingdom, Week December 11 - Click to enlarge |

In the emerging market space, the new Governor of Mexico’s central bank may establish his anti-inflation credentials by hiking rates by 25 bp at his first meeting, to 7.25%. This means that for the first time, Mexico’s overnight rate will be above Brazil’s Selic rate (following Brazil’s 50 bp cut last week to a record low 7.0%). On the other hand, Russia is expected to continue to unwind the 2014 tightening with a 25 bp rate cut to bring its key rate to 8.0%.

The other emerging market central banks that meet, Chile, Colombia, Peru, Indonesia, Philippines, and Turkey, none are expected to move. If there is a surprise, it could be tightening by the Turkey, where inflation expectations are trending higher and in November stood at their highest level (8.65%) since 2008. The December report will be made before the central bank meets. Turkey is also expected to report a sharp acceleration in Q3 GDP from 5.1% year-over-year in Q2.

Full story here Are you the author?Tags: Bank of England,ECB,Federal Reserve,newslettersent,Swiss National Bank