George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

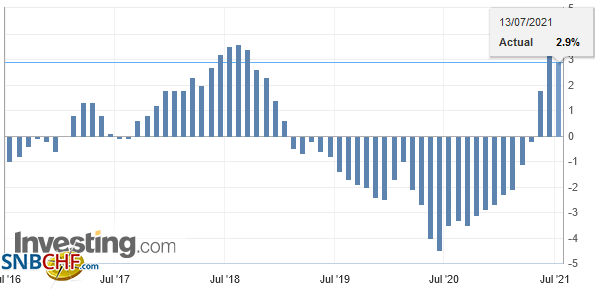

Swiss FrancSpeculators were net short CHF in January 2015, shortly before the end of the peg, with 26.4K contracts. Then again in December 2015, when they expected a Fed rate hike, with 25.5K contracts.The biggest short CHF, however, happened in June 2007, when speculators were net short 80K contracts. Shortly after, the U.S. subprime crisis started. The carry trade against CHF collapsed. The reverse carry trade in form of the Long CHF started and lasted - without some interruptions - until the peg introduction in September 2011. In mid 2011, the long CHF trade became a proper carry trade - and not a reverse carry trade anymore - because investors thought that the SNB would hike rates earlier than the Fed. CHF Speculative PositionsLast data as of August 01: The net speculative CHF position has risen from -1.5K short to 1.4K contracts long (against USD).

|

Speculative PositionsChoose Currency source: Oanda |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Marc Chandler My articles My offerMy siteAbout meMy videosMy books Follow on:LinkedINTwitterSeeking AlphaAmazon In the CFTC reporting week ending August 1, speculators in the futures market continued to build long exposure in the dollar-bloc currencies. In the three sessions after the reporting period closed, the dollar-bloc currencies have traded heavily.The bulls added 12.5k contracts to lift the gross long Canadian dollar position to 82.9k contracts. It is the largest such position in nearly five years. The bears covered 1.5k contracts to leave a gross short position of 42.2k contracts. This resulted in a 50% increase in the net long position to 40.6k contracts from 26.6k.The bulls topped up their gross long Australian dollar position by adding 4.5k contracts, lifting it to 85.3k contracts. The gross short position edged ever so slightly higher. The net long position increased to 60.7k contracts and was the seventh consecutive weekly increase. Speculators were mostly inactive in the New Zealand dollar, but the net long position edged up to 34.9k contracts. The other significant (more than 10k contract) gross position adjustment was in sterling. Speculators added 10k contracts to the gross short position, lifting it to 88.3k contracts. In the prior reporting week, the gross shorts rose by 11k contracts. The bulls were not discouraged and added 6.7k contracts to the gross long position. It stood at 58.9k contracts. Although the speculative position adjustment in the euro and yen were modest at best, there has been a change. The bulls cut gross long euro positions for the second consecutive week. The bears covered almost 1k previously sold yen contracts, but the gross short position was reduced for the second consecutive week. However, the overall negative dollar bias remained evident. Of the eight currency futures we track, the gross longs were increased in six. On the other hand, the bull who have dominated the 10-year Treasury note futures retreated. They liquidated 23.1k contracts, leaving a gross long position of 850.6k contracts. The bears were emboldened and added 46.7k contracts to the gross short position, raising it 639.7k contracts. The net long position fell by a quarter to 210.9k contracts. The bulls were reinvigorated. They added 58.9k contracts to the gross long position, increasing it to 717.8k contracts. The bears covered 4.6k contracts, leaving a gross short position of 231.7k contracts. As a result, the net long position increased by 63.4k contracts to 486.1k contracts. |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Full story here Are you the author?

Tags: Commitment of Traders,EUR/CHF,newslettersent,Speculative Positions,USD/CHF