Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

- Yellen will unlikely deviate from general tone of post-FOMC meeting remarks.

- FOMC minutes were clear, most members see the decline in inflation due to transitory developments.

- Bank of Canada is expected to hike rates and will likely leave the door open to another rate cut in Q4.

- UK wage growth has continued to slow.

In Germany, roughly half the backing of nominal interest rates can be explained by an increase in the 10-year breakeven. In the US, the nominal 10-year yield has risen 25 bp, but the 10-year breakeven rose by only five basis points. Italy’s performance is more like the US experience. Only about a quarter of the nominal yield increase can be accounted for by the rise of inflation expectations as reflected by the breakeven.

Reports suggest that many of the members at the G20 were prepared to support a joint declaration condemning North Korea, but the US did not put one forward such a motion. It may not change things on the ground, but displays a vacuum of leadership that makes investors uncomfortable.

If summits have winners and losers, Trump and Putin appear to have done fine. The snub to American intelligence service and environmental concerns, championed by Europe, the two leaders had their first bilateral meeting while the G8 were discussing climate protection. Trump reportedly was willing to accept Putin’s denial of hacking into the US to influence the 2016 campaign at face value, while another cease-fire was agreed in Syria.

It is said that statistics sufficiently tortured will confess to anything. There should be a corollary for G20 statements. The English language is sufficiently flexible, that any disagreement can be so obfuscated as to render it a meeting of the minds. The US won the recognition that there were legitimate trade defense measures and a November deadline to begin addressing the over-capacity in the steel. The US is threatening to put tariffs or tariffs and quotas on imported steel.

Although it seemed that the decision was going to be made at the end of June, the G20 meeting appears to have bought some time. Imposing the steel duties ahead of the deadline would be seen as particularly aggressive. Note that the US is formally investigating aluminum imports on national security grounds as well. However, the frustration of legislative inaction (the GOP Senate health care plan still does not have a majority, according to reports, as Congress returns to Washington).

GermanyOn June 26, the 10-year generic German yield closed at 24.5 basis points. It finished last week a little over 57 basis points. The similar Italian yield has risen 45 basis points to 2.05%. The short-end of the yield curve is constrained by the negative 40 basis point deposit rate. The steepening of the yield curve offsets the price erosion of banks’ bond holdings, and bank share price (in the Dow Jones Stoxx 600) have risen five percent during this period dramatic increase in long-term interest rates). |

Economic Events: Germany, Week July 10 - Click to enlarge |

EurozoneThe ECB continues to try to calibrate its communication with the evolving economy and its risk assessment. It appears that the confidence of officials has outstripped their willingness to express it for fear of spurring precisely what has happened: a premature tightening of financial conditions. Recall with without inflation on a durable and self-sustaining path, the ECB, with Draghi at the helm, is reluctant to remove accommodation. The ECB will most likely add another 360 bln euros of assets to its balance sheet this year and more next year, even if at a slower pace. The record of last month’s ECB meeting suggested that the central bank is prepared to alter its risk assessment for an increase in asset purchases. Investors have long assumed this to be the case, and Draghi has pushed back against ideas that deposit rate should be hiked before the asset purchases are complete. At stake for the ECB is tweaking its forward guidance and risk assessment. In the US, the issue is still material changes in the monetary stance. Specifically, the improved growth prospects in Q2 after a disappointing Q1 (again), the strength of the non-manufacturing ISM, and the ongoing firm labor market suggests the Fed remains on course to begin shrinking its balance sheet, and continue to gradually raise interest rates. |

Economic Events: Eurozone, Week July 10 - Click to enlarge |

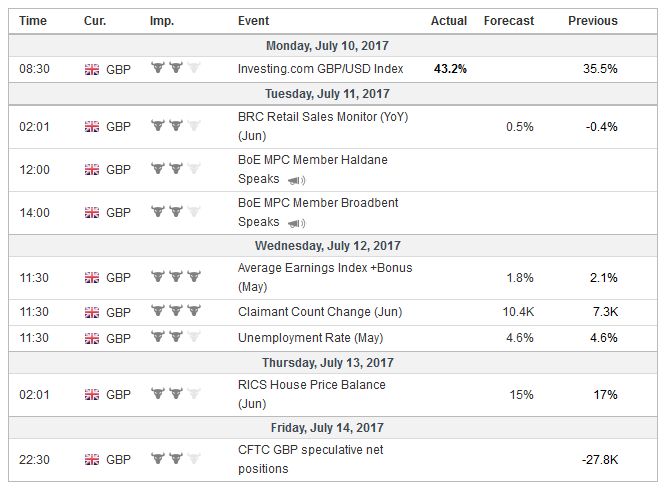

United Kingdom

|

Economic Events: United Kingdom, Week July 10 - Click to enlarge |

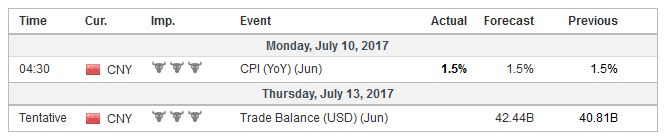

ChinaPresident Xi of China might have lost the most. The US-Russia dialogue was center stage. Xi did not want the focus to be on steel overcapacity, for which China is the critical player. The flare-up of a longstanding territorial dispute with India made for some uncomfortable meetings, according to reports. |

Economic Events: China, Week July 10 - Click to enlarge |

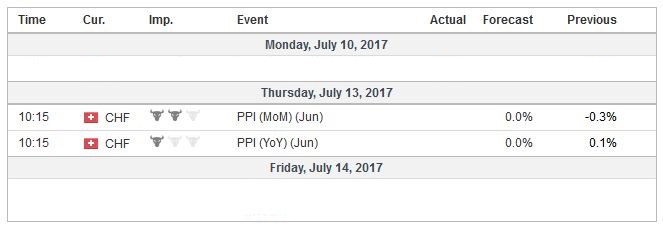

Switzerland |

Economic Events: Switzerland, Week July 10 - Click to enlarge |

Canada

The Bank of Canada is also not just about talk and altering its forward guidance. It will most likely become the second G7 central bank after the Federal Reserve to raise interest rates. Ever since Senior Deputy Governor Wilkins suggested on June 12 that the central bank is reconsidering the level of monetary accommodation in light of economic performance, there has been a sustained campaign. The result is that a 25 bp rate hike at this week’s meeting is practically fully discounted. Indeed, we suspect that there are better odds than the market is discounting of a follow-up hike in Q4, as the central bank unwinds the two rate cuts delivered in 2015 in response to the oil shock.

The economy has averaged 3.5% growth (annualized) over the past three-quarters, and Q2 17 appears to have begun off on solid footing. Job growth has been impressive. Canada has grown 29k jobs a month on average over the past 12 months. Canada is roughly a tenth the size of the US. It would be as if the US created around 290k jobs a month. Instead, on average over the past year, it has created about a third less. Canada’s job growth in Q2 was the most in seven years. In contrast, the US job growth on a three-month basis fell to a three-year low in May before rebounding in June.

The Canadian dollar has been the strongest major currency since the beginning of May, rising 6.25% against the US dollar. However, it has been a laggard so far this year. Its year-to-date 4.4% gain, is among the worst performers, being stronger only than the Norwegian krone (~3.3%)and the Japanese yen ( ~2.7%). In the futures market, speculators retain a net short Canadian dollar position, while they are net long the other dollar-bloc currencies. The Canadian dollar has appreciated in seven of the past ten weeks, and this has left technical stretched, but have not turned.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,G20,newslettersent