Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

- The consensus narrative sees a coordinated attempt by officials to prepare investors for less accommodative monetary policy.

- Data from the eurozone and UK may suggest the respective economies are not accelerating.

- Before getting to the jobs report, the US economic data, like auto sales, may be soft, while the prices paid in the manufacturing ISM may ease.

Here are the data points that the consensus narrative connects. The BIS encourages countries not to dawdle and remove accommodation when appropriate. The Bank of Canada indicated that after several quarters of strong economic expansion and robust labor market growth, it is time to re-think its monetary stance.

The sell-off in European bonds dragged US bonds lower, but premium the US offered narrowed. The US 10-year premium over Germany, for example, narrowed 16 bp last week to nearly 180 bp; the smallest premium since last November. It peaked near 235 bp late last year. The US two-year premium slipped only a single basis point last week, but in the three-week slide, the premium has narrowed by 11 bp. The two-year premium peaked near 222 bp in early March, and since then has found a base near 192 in each month (April, May, and now June).

For two month’s the euro has alternated between weekly gains and losses. In the saw-tooth pattern the weekly advances have been larger than the weekly losses; hence the uptrend. If the pattern is to remain intact, it will be a down week for the euro, which is consistent with a further clarification by the ECB and soft economic data in the EMU (and the UK). We expect the market to turn cautious ahead of $1.15.

Sterling has advanced for eight consecutive sessions. It is the longest streak in two years. It has approached an important technical area that kept the May rally in check ($1.3055). A push above this level early in the week ahead could be similar to the end of a boxer’s punch, as opposed to a sustained breakout, especially if the fundamental data suggest Carney’s caution will continue to prevail.

There are events next week that may be under-appreciated. The first is that Japan and the EU are getting very close to a trade agreement. In fact, the July 6 summit is likely to produce a political agreement to remove all customs duties in the bilateral trade. The deal, according to estimates, could triple EU agriculture exports to Japan, and increase overall EU exports by a third.

Next week concludes with the G20 meeting in Hamburg Germany on July 7-8. The theme is a fair and free trade. It will be one of the more difficult summits to paper over the distinct tensions as is the usual fare. There are broad tensions with the United States. The withdrawal from the TPP and the Paris Accords, the sanctions that threaten the Nord Stream 2 pipeline, the reported requests for unilateral concessions from some Asian trading partners, supporting Le Pen in France, and the threat to put a tariff on steel imports are all flash points.

The inability to distinguish a squabble among friends and allies with strategic disputes with adversaries risks raising trade tensions and isolating America at a time when international cooperation is sought on a wide range of issues, including fighting terrorism and reining in North Korea. This could have a longer-term impact on the dollar, and underpin the underlying desire for an alternative, for which we would continue to argue that there is no compelling candidate.

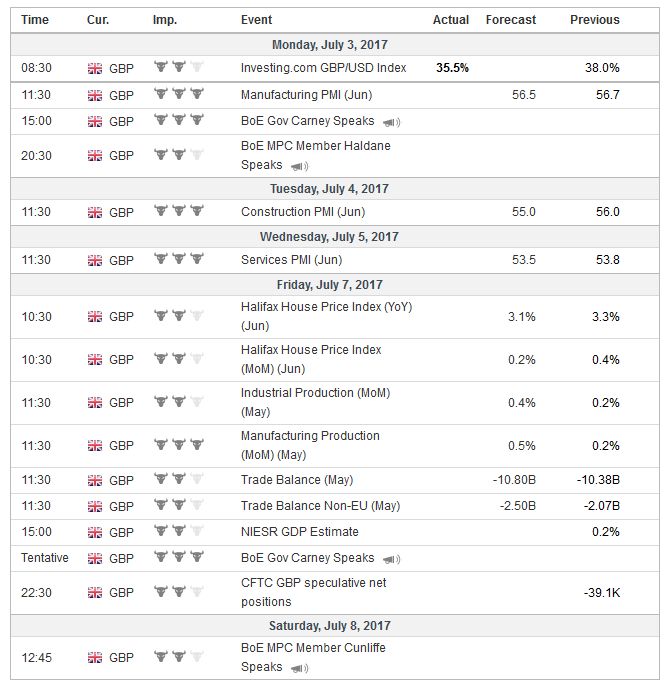

United KingdomIn a close (5-3) vote, the Bank of England left rates on hold in June, and Governor Carney who had forcefully argued against raising rates seemed more open. It has removed some accommodation provided after last year’s referendum through raising the capital buffer. The UK June PMIs are expected to have softened. It would be the second consecutive decline. The composite average in Q2 is unlikely to show improvement from Q1, suggesting growth is still around a 0.2%-0.3% pace. While median forecasts call for an increase in industrial production and manufacturing output, it appears to come at the cost of a deterioration in the trade balance. Nor did Carney flip-flop from the Mansion House Speech. He outlined his considerations if monetary accommodation should be removed. It seems clear from Carney’s comments that those considerations would not be addressed in weeks but months.

|

Economic Events: United Kingdom, Week July 03 - Click to enlarge |

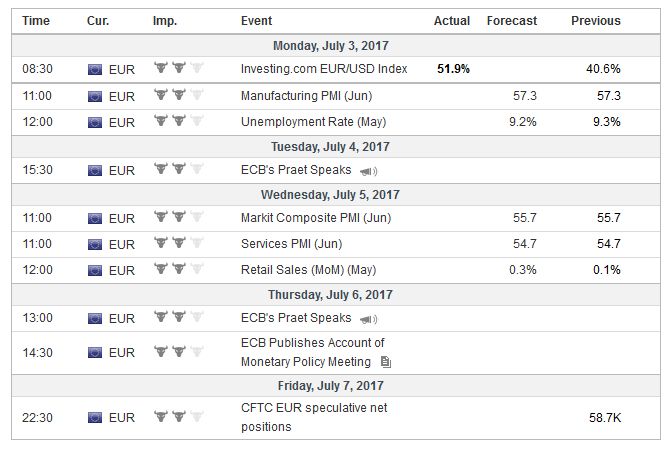

EurozoneThe ECB has been gradually evolving its risk assessment and forward guidance. The downside risks to growth have dissipated, it says, and the threat of deflation has been turned back. Many understood Draghi to have also indicated readiness to begin removing accommodation. There is a coordinated effort underway to take away the proverbial punch bowl. The euro’s price action had traced out some kind of topping pattern against the Swedish krone. Whether it is a triple top or a head and shoulders pattern, the neckline ( ~SEK9.70) broke dramatically, and the initial target near SEK9.60 was approached before the weekend. It also corresponds to a 50% retracement of this year’s euro rally. The next target is in the SEK9.50-SEK9.55 area. The story that is spun suggests that officials everywhere are telling investors that the gig is up, that peak QE is behind us and a new monetary cycle is at hand. We are skeptical and suspect that the narrative is getting ahead of itself. The Vice President of the ECB quickly tried to explain that Draghi was not announcing a change in policy. Draghi had, we thought, been clear that the preconditions of removing accommodation, namely a durable and sustainable increase of inflation, had still not been achieved. Even before last week’s comments, we anticipated that in September, the ECB would likely announce an extension of its asset purchases into the first half of 2018 albeit at a reduced pace. Draghi also seemed clear that he was opposed to lifting the deposit rate before the asset purchases were complete. If the market ran on what it thought it heard, the economic data due out in the coming days might provide a reality check. The final eurozone PMIs will likely confirm the moderation seen in the flash reading. Germany and Spain will likely report a decline in May industrial output. Unemployment in the region is expected to have steadied at 9.3% in May. It is down from 10.2% in May 2016, but it is still not at politically acceptable levels. Retail sales are expected to have decelerated to a 2.3% year-over-year pace from 2.5% in April. It would be the slowest pace in three months. |

Economic Events: Eurozone, Week July 03 - Click to enlarge |

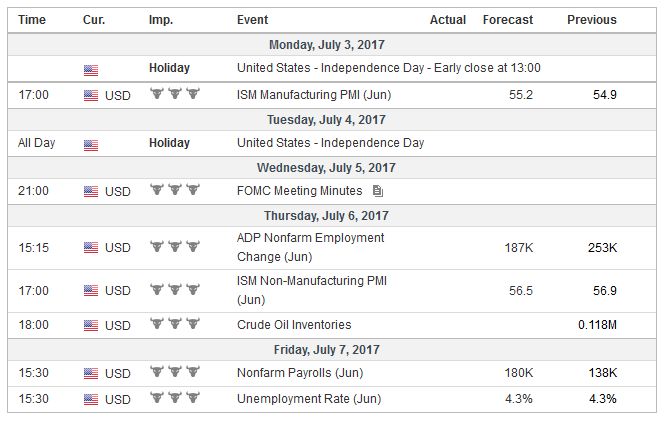

United StatesIronically, the only major central bank that the market is skeptical about seems to be the Federal Reserve. The troika of leaders (Yellen, Fischer, and Dudley) as well as a couple of regional Fed Presidents not only want to press ahead with the course, and added to their arguments a discussion about financial conditions and rich equity valuations. Depending on one’s assumptions, the Fed funds futures strip implies around a 15% chance of a hike in September and around a 45% chance of a hike. However, before getting to the jobs report, there will be other data that will likely play on investor concerns about the trajectory of the economy and prices. Even if the manufacturing ISM picks up as suggested by the various Fed manufacturing surveys and the Chicago PMI reported before the weekend, prices are likely to have softened. Price paid may have fallen for the third month. We suspect that officials in Europe will be more likely to protest a premature backing up of interest rates than US officials. This taper tantrum began in Europe. They will likely want to prevent it from getting out of hand. The data highlight of the holiday-shortened US week is the employment data, and a bounce back after a soft May report is expected. Non-farm payrolls are expected to have expanded by around 175k-180k in June, with a 0.3% increase in average hourly earnings. The unemployment rate has fallen from 4.8% in January to 4.3% in May, where it likely remained. The underemployment rate (U-6) fell from 9.4% in January to 8.4% in May. It too is not expected to have changed in June. Central bankers, especially the Americans, are convinced that some Phillip’s Curve is at work, whereby higher labor costs (spurred by demand relative to supply) are passed along to customers through higher prices. As long as slack in the labor market is being absorbed, many Fed officials will be confident that, at some point, wages will rise, and there will be an increase in the general price level (inflation). Softer goods prices would be acceptable, perhaps, if it was associated with an increase in demand. However, the continued gradually slowing in auto sales warns of a headwind on retail sales. If the median expectation that the US bought cars and light vehicles at a 16.5 mln unit pace in June, then it will mark the slowest quarter since Q1 14. However, the key to the dollar’s performance in the time frame that matters to most investors lies with cyclical considerations and the US economic and monetary policy. The debate within the Republican Party, which has a majority in both chambers, has paralyzed the legislative process, creating the famed gridlock, in a similar but different way that as the inter-party rivalry has sometimes fostered. The lack of convincing legislative progress on healthcare, for which the opposition to the Affordable Care Act was most united, raises questions about the broader economic agenda, and recently prompted the IMF t o revise down its growth outlook for the US. |

Economic Events: United States, Week July 03 - Click to enlarge |

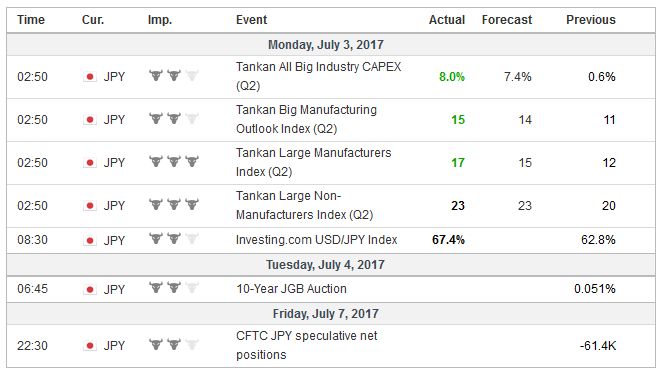

JapanThe Bank of Japan has not discussed its exit strategy. Some have argued that by shifting policy toward targeting the 10-year yield, which requires the purchase of fewer JGBs, that the BOJ has already begun tapering. We do not think this is a fair assessment, and it is one that the BOJ itself rejects. The sell-off in European bonds spurred a global move and the JGB was not immune. We expect a robust defense by the BOJ. While we suspect the eurozone economy is more likely to moderate than accelerate, the Japanese economy is accelerating. The Tankan Survey kicks off the quarter and improvement is expected across the board, including a healthy jump in capex plans, which are expected to be the strongest in a year and a half. Japan’s Composite PMI stood at its highest level in at least three years in May. It may be little changed in June. The resounding defeat of the LDP in the Tokyo election prompt another supplemental budget. With numerous accusations of improprieties and favoritism, Prime Minister Abe may find his political agenda challenged, even as there appear no alternative to Abenomics. With the BOJ lagging behind the other central banks, short yen cross positions have been in momentum and carry buckets. The dollar’s weekly close above JPY112.00 was a constructive price development. A downtrend line from the year’s high intersects at the end of next week near JPY112.50. A break of this would further lift the tone. On the downside, the JPY111.20-70 offers an initial base. |

Economic Events: Japan, Week July 03 - Click to enlarge |

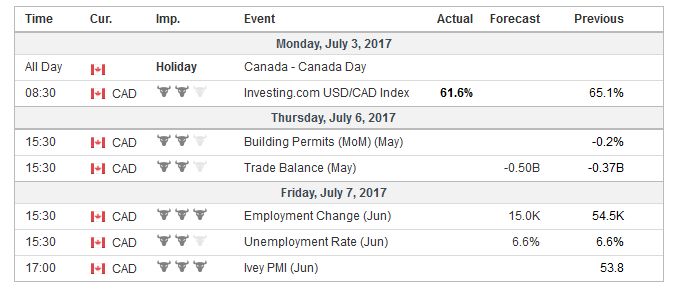

CanadaThe Bank of Canada has unambiguously warned the market that it is considering raising rates. The market believes it. The OIS appears to have discounted an 80%-85% chance that a 25 bp hike will be delivered on July 12. Canada reports both jobs and trade in the week ahead. Theoretically, they have the ability to disrupted official plans, but most likely they won’t. Job growth has been sizzling. Canada has generated 316.8k jobs over the past 12 months, and a solid two-thirds have been full-time positions. Wages have firmed recently. For the past three-quarters, the economy has grown around 3.5% and appears off to a solid start in Q2. Canada’s trade balance has improved, helped by a recovery in non-energy exports. The impact of the softwood lumber duties will be of interest. How much was volume impacted or how much simply meant US consumers paid a higher price? |

Economic Events: Canada, Week July 03 - Click to enlarge |

AustraliaTwo major central banks meet in the week ahead. Both the Reserve Bank of Australia and Sweden’s Riksbank are likely to also tilt their neutral stance toward a little less accommodation. Through statement rather than deeds, the respective monetary authorities can downplay the likelihood that economic conditions will warrant further easing. This may have more market impact in Australia, where there are some lingering ideas that rates may still be cut, and the Australian dollar is trading at the upper end of a year-old trading range. In fact, as the first half ended, the Australian dollar is flirting with a trend line drawn off the April and November 2016 spike highs and the highs from March this year. It is found near $0.7725.

|

Economic Events: Australia, Week July 03 - Click to enlarge |

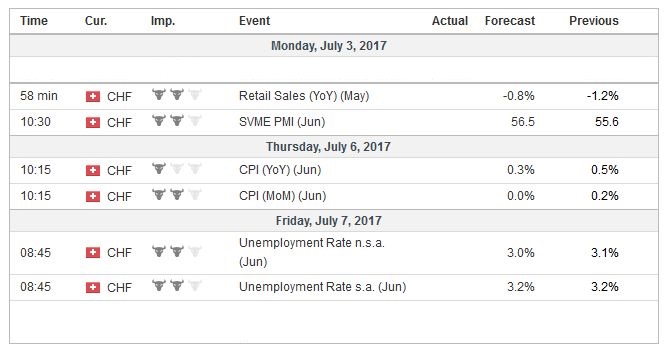

Switzerland |

Economic Events: Switzerland, Week July 03 - Click to enlarge |

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,newslettersent,SEK