Stock MarketsEM FX was mixed last week but in general held up well in the aftermath of Super Thursday. The global backdrop seems relatively benign right now despite the FOMC meeting this week. We still think investors have to be picky.

TRY, ZAR, and BRL at current levels seem too rich given the underlying risks in all three. On the flip side, we think China is looking stable right now and should help Emerging Asia’s outlook near-term.

|

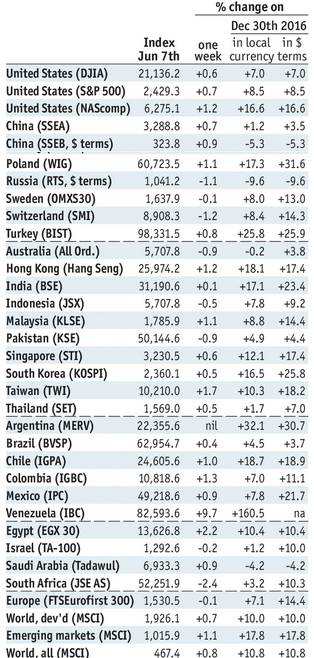

Stock Markets Emerging Markets, June 07 Source: economist.com - Click to enlarge |

ChinaChina will report May money and new loan data sometime this week. No date has been specified, but these series are expected to show some modest slowing from April. May IP and retail sales will be reported Wednesday. The former is expected to rise 6.4% y/y while the latter is expected to rise 10.7% y/y.

SingaporeSingapore reports April retail sales Monday, which are expected to rise 2.5% y/y vs. 2.1% in March. It then reports May trade Friday, with NODX expected at -5.6% y/y vs. -0.7% in April. Recent real sector data have been firm, while CPI rose 0.4% y/y in April. While the MAS does not have an explicit inflation target, low price pressures should allow it to maintain steady policy into 2018. However, it may tweak its language at the October policy meeting to reflect modest improvement in the economic outlook.

TurkeyTurkey reports Q1 GDP Monday, which is expected to grow 3.4% y/y vs. 3.5% in Q4. The central bank then meets Thursday and is expected to keep all rates steady. CPI inflation eased to 11.7% y/y in May, the first deceleration since November. With the lira remaining firm, this gives the central bank leeway to keep policy steady for now.

IsraelIsraeli central bank releases its minutes Monday. Israel then reports May trade Tuesday and Q1 current account Wednesday. May CPI will be reported Thursday, with inflation expected to remain steady at 0.7% y/y. This is still below the 1-3% target range, which should allow the central bank to remain on hold for now. Next policy meeting is July 10, no change is expected then.

IndiaIndia reports May CPI and April IP Monday. The former is expected to rise 2.4% y/y vs. 3.0% in April, while the latter is expected to rise 2.8% y/y vs. 2.7% in March. India reports May WPI Wednesday, which is expected to rise 3.1% y/y vs. 3.85% in April. Sluggish growth and falling inflation have some analysts looking for a rate cut from the RBI. We are skeptical, but acknowledge that it will likely remain on hold for now. Next policy meeting is August 2, no change expected then.

BrazilBrazil reports April retail sales Tuesday, which are expected at -2.5% y/y vs. -4.0% in March. The economy has bottomed, but the recovery has been lackluster. Next COPOM meeting is July 26, and a 75 bp cut is widely expected. With the easing cycle likely to slow, GDP growth may lag market expectations for 0.7% this year and 2.3% next year.

South AfricaSouth Africa reports April retail sales Wednesday, which are expected to rise 0.6% y/y vs. 0.8% in March. After the surprisingly weak Q1 GDP data, markets will be looking to Q2 for signs of a rebound. We didn’t get it yet with manufacturing production (-4.1% y/y). We think weak data will lead SARB to cut rates in H2, though the July 20 meeting may be too soon. September 21 seems more likely to start cutting.

IndonesiaBank Indonesia meets Thursday and is expected to keep rates steady at 4.75%. CPI rose 4.3% y/y in May, the highest since March 2016 and in the top half of the 3-5% target range. This should keep the central bank leaning hawkish, though a rate hike seems unlikely until late this year.

ColombiaColombia reports April IP and retail sales Thursday. The former is expected at -3.4% y/y while the latter is expected at -2.0% y/y. The economy remains weak, and supports the case for further rate cuts as inflation converges with the 2-4% target range. Next policy meeting is June 30, and another 25 bp cut to 6.0% seems likely.

ChileChile central bank meets Thursday and is expected to keep rates steady at 2.5%. May CPI rose 2.6% y/y, the lowest since November 2013 and within the 2-4% target range since August. The bank has signaled the end of the easing cycle after 100 bp of easing this year, but the data remain weak. If the recovery does not materialize, we would not rule out further easing.

RussiaCentral Bank of Russia meets Friday and is expected to cut rates 25 bp to 9.0%. However, the market is split. Of the 23 analysts polled by Bloomberg, 2 see steady rates, 12 see a 25 bp cut, and 9 see a 50 bp cut. Governor Nabiuliina admitted that the bank was likely to discuss 25 or 50 bp cuts. We now lean toward 25 bp after CPI inflation remained steady at 4.1% y/y.

|

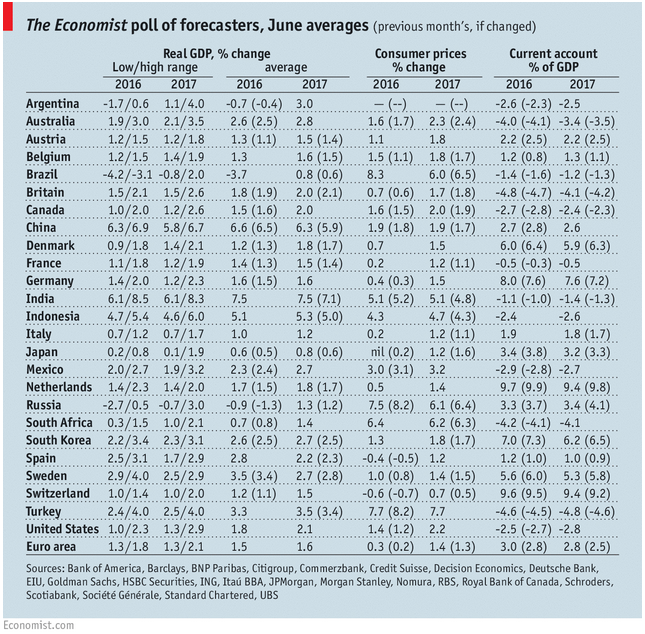

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, June 2017 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Win Thin is a senior currency strategist with over fifteen years of investment experience. He has a broad international background with a special interest in developing markets. Prior to joining BBH in June 2007, he founded Mandalay Advisors, an independent research firm that provided sovereign emerging market analysis to institutional investors. He received an MA from Georgetown University in 1985 and a B.A. from Brandeis University 1983. Feel free to contact the Zurich office of BBH

Tags: Emerging Markets,newslettersent