Stock MarketsEM FX closed last week on a firm note as weak US jobs data supported the notion that the Fed will find it hard to tighten in H2. No major US data will be reported this week and the FOMC embargo for the June 14will be in effect. As such, there is little on the near-term horizon that might help the dollar, so it’s likely to remain on the defensive this week. As always, political risk in EM remains significant. Brazil and South Africa continue to simmer, and we see more bad news ahead from both. As of this writing, the outcome of the Mexican state elections is not yet known. |

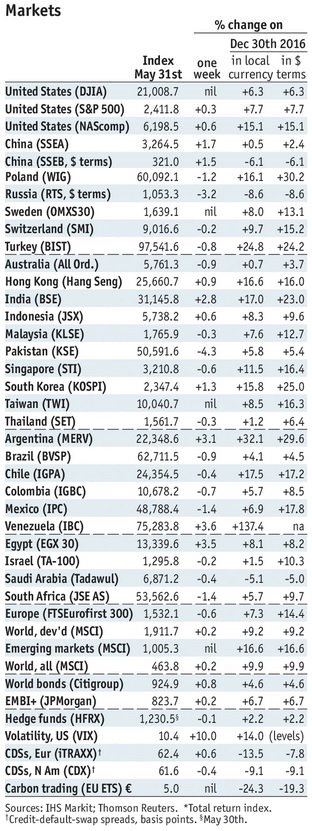

Stock Markets Emerging Markets, May 31 Source: economist.com - Click to enlarge |

ChinaCaixin reports May China services and composite PMIs Monday. Recent data suggests the economy is slowing, albeit modestly. China reports May trade data Thursday, with exports expected to rise 7.0% and imports by 9.0% y/y. This will be followed by May CPI and PPI Friday. The former is expected to rise 1.5% y/y, while the latter is expected to rise 5.7% y/y. TurkeyTurkey reports May CPI Monday, which is expected to rise 11.7% y/y vs. 11.9% in April. If so, it would be the first deceleration since November. Still, inflation would remain well above the 3-7% target range and so we think further tightening will be needed. Next central bank policy meeting is June 15, and another hike in the Late Liquidity Window rate is possible. Turkey then reports April IP Thursday, which is expected to rise 4.1% y/y vs. 2.8% in March. ChileChile reports April monthly GDP proxy Monday, which is expected to rise 0.8% y/y vs. 0.2% in March. Chile reports May trade Wednesday. It then reports May CPI Thursday, which is expected to rise 2.5% y/y vs. 2.7% in April. This would move it closer to the bottom of the 2-4% target range. The bank has signaled that the easing cycle is over for now. Next central bank policy meeting is June 15, and no change is expected. ColombiaColombia reports May CPI Monday, which is expected to rise 4.49% y/y vs. 4.66% in April. If so, it would be the lowest rate since August 2015 and a bit closer to the 2-4% target range. Yet the weak economy has prompted the start of the easing cycle last month. Central bank minutes from that meeting will be reported Friday. Next policy meeting is June 30, and another 25 bp cut seems likely. TaiwanTaiwan reports May CPI Tuesday, which is expected to rise 0.6% y/y vs. 0.1% in April. The central bank does not have an explicit inflation target. However, the lack of any price pressures will allow it to remain on hold for now. It next meets June 22, no change expected then. Taiwan reports May trade Wednesday, with exports expected to rise 7.1% and imports by 8.5% y/y. PhilippinesPhilippines reports May CPI Tuesday, which is expected to rise 3.3% y/y vs. 3.4% in April. This is in the upper half of the 2-4% target band, which gives the central bank leeway to keep rates on hold for now. Next policy meeting is June 22, no change is expected then. Czech RepublicCzech Republic reports April retail sales Tuesday, which are expected to rise 1.2% y/y vs. 10.1% in March. It then reports April industrial (-1.0% y/y expected) and construction output Wednesday. May CPI will be reported Friday, which is expected to rise 2.2% y/y vs. 2.0% in April. The central bank does not appear to be in any hurry to hike. Next policy meeting is June 29, no change is expected then. HungaryHungary reports April retail sales Tuesday which are expected to rise 4.1% y/y vs. 5.4% in March. It then reports April IP Wednesday, which is expected to rise 5.4% y/y WDA vs. 10.0% in March. Central bank minutes will also be released Wednesday. April trade and May CPI will be reported Thursday, with inflation expected at 2.1% y/y vs. 2.2% in April. If so, it would move closer to the bottom of the 2-4% target range. Next policy meeting is June 20, no change is expected then but there is a small risk of a dovish tweak to unconventional policy. South AfricaSouth Africa reports Q1 GDP Tuesday, which is expected to rise 1.0% y/y vs. 0.7% in Q4. It then reports April manufacturing production Thursday, which is expected at -1.6% y/y vs. +0.3% in March. We believe that with inflation easing, the weak economy will lead the SARB to start an easing cycle in H2. Next policy meeting is July 20, but that’s too soon and so we expect steady rates then. BrazilCOPOM releases its minutes Tuesday. At that meeting, it cut 100 bp but signaled a slower pace going forward due to political concerns. Brazil reports May IPCA inflation Friday, which is expected to rise 3.74% y/y vs. 4.08% in April. Next policy meeting is July 26, and we think a 75 bp cut is likely then. IndiaReserve Bank of India meets Wednesday and is expected to keep rates steady. Q1 GDP came in much weaker than expected, while recent inflation measures have fallen sharply. CPI rose 3% y/y in April, in the bottom half of the 2-6% target range. All in all, the data give the RBI scope to keep rates steady until a clearer picture of the economy emerges. PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. CPI rose 1.9% y/y in May, which is near the bottom of the 1.5-3.5% target range. The bank is sticking with its forward guidance for the first hike in 2018. However, the economy remains robust and so that guidance should eventually be moved forward to H2 2017. However, this meeting seems too soon. RussiaRussia reports May CPI Wednesday, which is expected to rise 4.0% y/y vs. 4.1% in April. If so, this would be right at the central bank’s year-end target. Next policy meeting is June 16, and a 25 bp cut is likely then. April trade will be reported Friday. MexicoMexico reports May CPI Thursday, which is expected to rise 6.16% y/y vs. 5.82% in April. If so, this would be the highest since April 2009 and further above the 2-4% target range. Next Banxico meeting is June 22, and another 25 bp seems likely, especially if the Fed hikes June 14. April IP will be reported Friday, which is expected at -2.1% y/y vs. +3.4% in March. PeruPeruvian central bank meets Thursday and is expected to keep rates steady at 4.0%. A minority of analysts look for a 25 bp cut. CPI rose 3.0% y/y in May, the lowest since August 2016 and right at the top of the 1-3% target range. The sluggish economy led the central bank to start the easing cycle last month with a 25 bp cut, and the easing cycle should continue this year. |

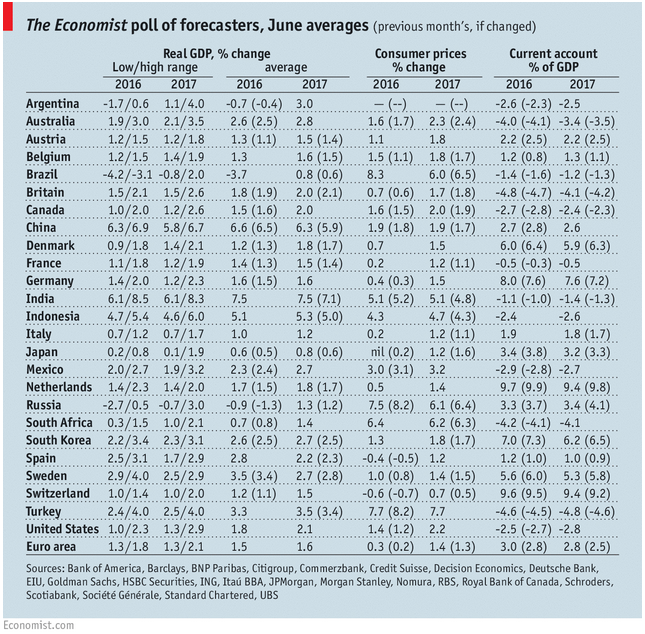

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, June 2017 Source: economist.com - Click to enlarge |

Tags: Emerging Markets,newslettersent