Stock MarketsEM FX was mostly softer last week, though it ended the week firmer, buoyed by outsized MXN gains Friday. The Fed is sending very strong signals for a March hike, which should keep EM FX on its back foot. However, with the March 15 FOMC embargo coming into effect, there will be no Fed speakers after Kashkari on Monday. Jobs data on Friday will be the highlight, but given the Fed’s signals, we do not think a soft report will derail a hike next week. EM CPI and real sector data this week should support our view that Asian and EMEA central banks will have to tilt more hawkish this week. Latam data should show further disinflation that supports a more dovish tilt in that region. |

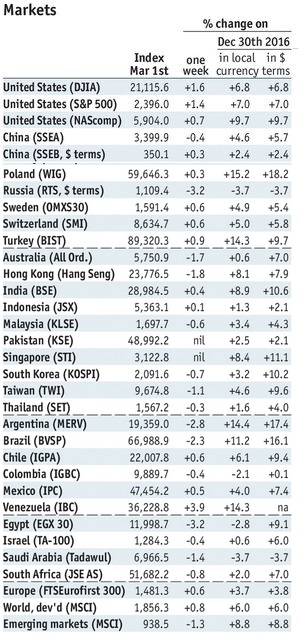

Stock Markets Emerging Markets, March 01 Source: economist.com - Click to enlarge |

ChileChile reports January GDP proxy Monday, which is expected to rise 1.1% y/y vs. 1.2% in December. Chile reports February trade Tuesday. It then reports February CPI Wednesday, which is expected to remain steady at 2.8% y/y. Whilst still within the 2-4% target range, the stalled disinflation warrants some caution on the part of the central bank. Next central bank meeting is March 16, and no change is likely then. TaiwanTaiwan reports February CPI and trade Tuesday. CPI is expected to rise 0.75% y/y vs. 2.25% in January, while exports are expected to rise 16.3% y/y and imports by 24.9%. Note that January and February data will be distorted by the timing of the Lunar New Year in 2016 (February) and 2017 (January). The central bank does not have an explicit inflation target, but rising price pressures should keep it on hold at its next quarterly policy meeting this month. PhilippinesPhilippines reports February CPI Tuesday, which is expected to rise 3.2% y/y vs. 2.7% in January. Is so, this would be the highest rate since November 2014, but still be within the 2-4% target range. Next policy meeting is March 23, and rates are likely to be kept steady at 3.0%. The central bank will be on alert and may turn more hawkish if price pressures accelerate further. HungaryHungary reports January IP Tuesday, which is expected to rise 2.8% y/y WDA vs. 1.9% in December. It reports February CPI Wednesday, which is expected to rise 2.8% y/y vs. 2.3% in January. If so, this would be the highest since February 2013 but still within the 2-4% target range. January trade will be reported Friday. South AfricaSouth Africa reports Q4 GDP Tuesday, which is expected to grow 0.6% y/y vs. 0.7% in Q3. The economy remains weak, but SARB cannot cut rates with inflation above the 3-6% target range. Furthermore, austerity measures taken to keep investment grade rating are a headwind on the economy. Next SARB meeting is March 30, no change seen then. However, an easing cycle could start in H2 if disinflation allows. BrazilBrazil reports Q4 GDP Tuesday, which is expected at -2.4% y/y vs. -2.9% in Q3. It then reports January IP Wednesday, which is expected to rise 1.5% y/y vs. -0.1% in December. If so, it would be the first positive reading since February 2014. IPCA inflation will be reported Friday, and is expected to rise 4.86% y/y vs. 5.35% in January. Markets are split between a 75 bp and 100 bp cut at the next COPOM meeting April 12, but we lean toward 75 bp. ChinaChina reports February trade Wednesday. In USD terms, exports are expected to rise 14% y/y and imports by 20%. It then reports February CPI and PPI Thursday. The former is expected to rise 1.8% y/y and the latter by 7.5%. Here too, January and February y/y comparisons will be distorted by the timing of the Lunar New Year holiday. Overall, the economy remains in solid shape. TurkeyTurkey reports January IP Wednesday, which is expected to rise 1.7% y/y vs. 1.3% in December. The economy is sluggish, but the central bank cannot ease in light of rising inflation. February CPI rose 10.13% y/y vs. 9.74% expected and 9.22% in January. Despite the firmer lira, CPI moved further above the 3-7% target range. Recent lira weakness and the 15.36% y/y surge in PPI suggest price pressures are intensifying. Next policy meeting is March 16. If the lira continues to weaken, further tightening is likely by tweaking the rates corridors again. PolandNational Bank of Poland meets Wednesday and is expected to keep rates steady at 1.5%. The bank may tilt slightly more hawkish in light of rising price pressures. Some NBP officials are finally acknowledging that 2018 may be too late to start the tightening cycle, and that 2017 is becoming more likely. CPI rose 1.8% y/y in February, within the 1.5-3.5% target range but the highest since December 2012. Czech RepublicCzech Republic reports January trade and February CPI Thursday. The former is expected at CZK22 bln while the latter is expected to rise 2.4% y/y. If so, inflation would be the highest since December 2012, though still within the 1-3% target range. Next policy meeting is March 30, and no change in policy or forward guidance is likely. We think the CNB is on track to exit the koruna floor around mid-year. MexicoMexico reports February CPI Thursday, which is expected to rise 4.81% y/y vs. 4.72% in January. Banxico warned of above-target inflation for 2017 in its quarterly inflation report. It also cut its 2017 growth forecast to 1.3-2.3% from 1.5-2.5% previously and its 2018 growth forecast to 1.7-2.7% from 2.2-3.2% previously. As such, we do not think it will tighten further if the peso remains firm. Next policy meeting isMarch 30, and no move is likely even if the Fed hikes March 15. PeruPeru central bank meets Thursday and is expected to keep rates steady at 4.25%. Price pressures remain elevated, with CPI accelerating to 3.3% y/y in February from 3.1% in January. This remains above the 1-3% target range. Indeed, with the exception of a month or two here and there, inflation has remains above this range since mid-2013. We believe further disinflation is needed to support the case for the first 25 bp rate cut. |

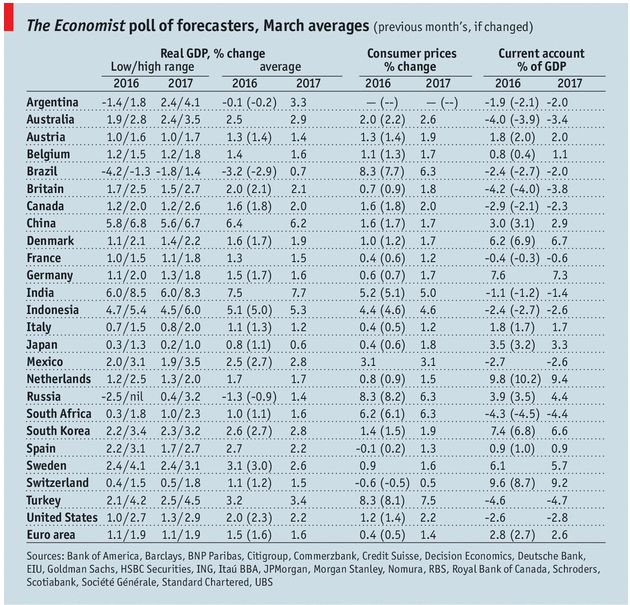

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, March 2017 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin