Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

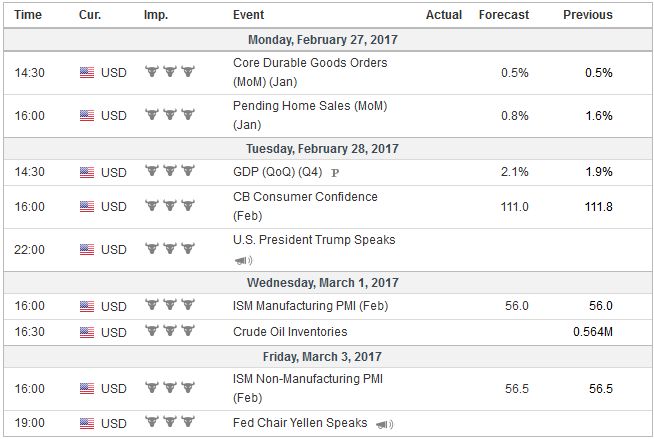

United StatesThere is a broad consensus around the macroeconomic picture. The headwinds slowing the US economy in H1 16 have eased, and above trend growth in H2 16 appears to be carrying into 2017. Q4 16 GDP is expected to be revised to 2.1% up from 1.8%. Many economists appear to accept that a good part, though not all, of the decline in the estimated trend growth in the US, is a function of demographic considerations. Price pressures are gradually increasing, though the Fed’s preferred and targeted measure of inflation, the core PCE deflator is likely to have remained at 1.7% in January, the base effect warns of topside risk in the coming months. Meanwhile, the labor market continues to improve. The four-week moving average of weekly jobless claims fell to a new cyclical low the same week the BLS conducted the survey for non-farm payrolls, which will be released on March 10. The Federal Reserve raised rates once in 2015 and once in 2016. This year will be different. The shift in opinion is not so much in the increase of the likelihood of a March increase or June increase, but in a move in May. As we have noted, the advantage May is that it would be part of the normalization process when every meeting must be live. Up until now, there was a general recognition that Fed action would take place at the quarterly meeting that had the economic forecast updates and was followed by a press conference. That was good and arguably necessary. However, this may no longer be the case. As the pace of removing accommodation increases, the Fed needs greater flexibility. Just as the minutes of the January FOMC meeting showed that the Fed would tweak the dot plot communication tool by including fan lines of confidence, as we have argued before, the Fed ought to consider a press conference after every meeting, like many others, including the BOE, ECB, and BOJ, and that would kill two birds with one stone, so to speak. Communication would be enhanced, and the Fed would double the number of actionable meetings. Alternatively, the Fed could scramble and put together an ad hoc press conference, but there are risks of leaks and fails to take advantage of the opportunity to evolve the Fed’s communication and transparency. |

Economic Events: United States, Week February 27 - Click to enlarge |

EurozoneEurozone growth is solid and stable, and above trend, which is estimated near 1.25%. This is likely to be confirmed with the final January PMIs due in the second half of the week ahead. Individual countries will update Q4 16 GDP estimates, and most likely will not have much market impact, but will be revealing nonetheless. The Spanish economy motored ahead by 3.0% year-over-year in Q4 16. France and Italy both appear to have grown 1.1%. Among other European countries reporting GDP, Sweden’s 1.9% puts it a little ahead of Germany’s 1.7%, while Switzerland’s 1.2% places it nearer France and Italy. The risks of deflation have evaporated in Europe thanks to the rise in oil prices. Indeed, the preliminary estimate for February CPI, which is to be reported on March 2, is expected to tick up to 1.9%-2.0%. The higher oil prices have knock-on effects on transports, heating, and energy prices. It was also unseasonably cold in southern Europe, which may have underpinned unprocessed food prices as well. In any event, core prices are expected to be flat at 0.9% for the third month and have seen a steady pace of 0.8%-0.9% since last May. It bottomed at 0.6% in January 2015. |

Economic Events: Eurozone, Week February 27 - Click to enlarge |

GermanyMany observers do not appreciate the importance of the faster increase in Germany inflation than elsewhere in the monetary union. Germany’s headline harmonized measure may push above 2.0% in February and will be reported ahead of the aggregate figures. There are a number of ways that countries can boost their competitiveness against Germany. Draghi pushes for structural reforms in both Germany and elsewhere, but it is proving a difficult to achieve. Another way is through the inflation differential. Several years ago, it was thought desirable that the periphery has lower inflation than Germany. However, Germany was experiencing disinflation and sometimes outright deflation. This forced deflationary condition on others. However, Germany now has higher inflation, even above target, and this is a net positive for the periphery, though the real impact requires this to be sustained. |

Economic Events: Germany, Week February 27 - Click to enlarge |

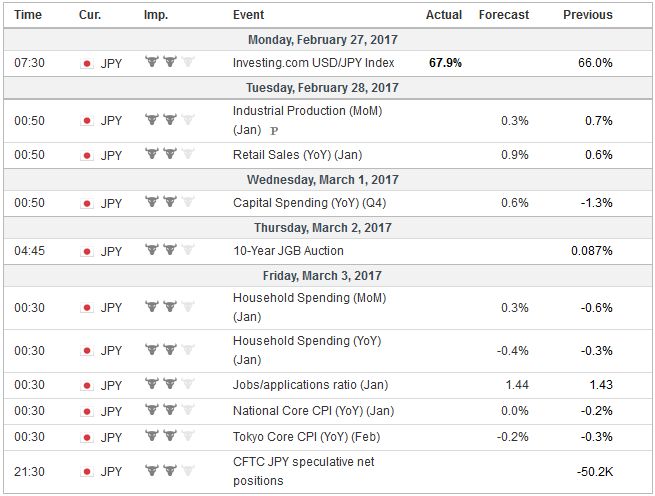

JapanJapan has a full slate of economic reports but the consensus view is unlikely to change. Japanese growth may be improving, but it is not firing on all cylinders. Industrial productions, exports, and government spending are largely offsetting the drag of consumption and domestic demand. A small increase in Q4 capex appears to be mostly in the export sector, and industrial output is accelerating. The median expectation is that capex rose 0.6% in the last three months of 2016, recouping less than half the decline in Q3. Household consumption in January is not expected to improve from the 0.3% year-over-year contraction reported in December. The poor consumption is not a function of the high level of unemployment as is the case in parts of Europe. The Japanese unemployment rate is expected to slip to 3.0% in January, matching the cyclical low, from 3.1% at the end of last year. Also, Japan is the last of the large high income countries that continue to wrestle with deflation. The core measure, which excludes fresh food finished 2016 at minus 0.2% year-over-year. It is expected to be at zero in January when it is reported at the end of next week. The core measure more comparable to the US measure, which excludes food and energy fell to 0.1% in December, the lowest year-over-year pace in three years. The recent peak was 1.3% at the end of 2015. It may have risen to 0.2% in January. |

Economic Events: Japan, Week February 27 - Click to enlarge |

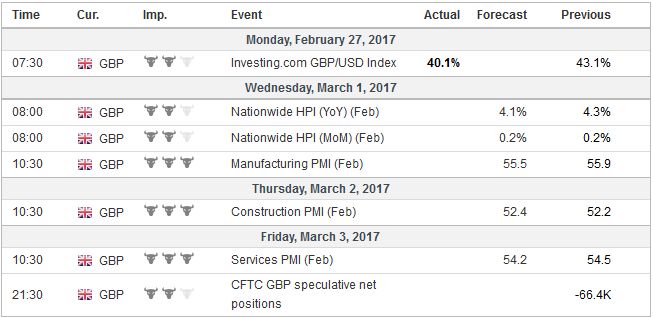

United KingdomThe UK reports the January PMIs starting in the middle of the week. The economy remained firm in H2 16 despite the wobble and fears around the referendum. While the low rates and sterling’s depreciation have been important shock absorbers, the risk seems to be on the downside. Most of the benefits will likely dissipate by Q3. The PMIs are likely to be largely steady with a slight softer bias. |

Economic Events: United Kingdom, Week February 27 - Click to enlarge |

ChinaSimilarly, China’s official and Caixin version of the PMI also be a touch lower than at the end of last year. The February times series are likely to be skewed by the Lunar New Year celebration and will most likely not elicit an important market response. Capital outflows appear to have slowed, and the February reserve figures are expected to be reported March 6-7. Recall that the $12.3 bln draw down of reserves in January was the smallest since last July. The yuan has edged higher against the US dollar this month, but the 0.2% gain is more a sign of stability than an appreciating trend. The implied volatility of the yuan has fallen sharply. This is consistent with less bearish outlooks. The implied 12-month volatility is near 6%, the lowest since late 2015. It had finished last year above 8%. The implied 3-month vol is near 4.7%, which is a four-month low. It was near 7.3% at the end of last year. Also since early January, the offshore yuan (CNH) has traded at a premium to the onshore yuan (CNY). |

Economic Events: China, Week February 27 - Click to enlarge |

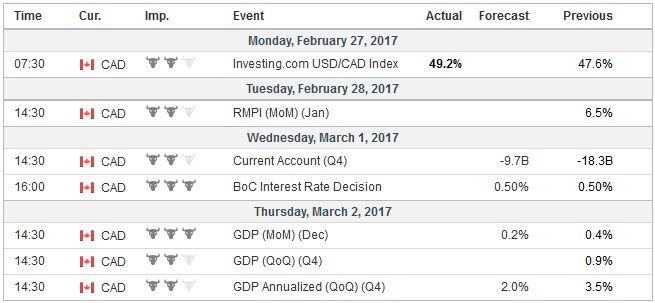

CanadaThe Bank of Canada is the only major central bank that meets in the week ahead. There is practically no chance of a change in policy, and there is little need to adjust the economic projections. The slow recovery continues, but there is still plenty of slack in the economy. There has been an improvement in the terms of trade, and the risk of a trade disruption given the new US administration appears to have slackened. However, non-energy exports have disappointed (-4.1% in December). Canada reports GDP figures the day after the BoC meeting. The economy is expected to have expanded 0.3% in December after 0.4% in November. Growth appears to have accelerated to 2.0% at an annualized pace in Q4 after a 3.5% pace in Q3, which was the strongest in a couple of years. |

Economic Events: Canada, Week February 27 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week February 27 - Click to enlarge |

Australia

Australia also reports Q4 GDP. It is expected to have bounced back after contracting 0.5% in Q3. A 0.7% expansion in Q4 would put year-over-year growth just below 2.0%. The risk is on the downside after last week’s disappointing capital expenditure figures.

The most important event next week for investors may be US President Trump’s speech to the joint session of Congress. Those hoping for detailed plans regarding tax reform and infrastructure spending are likely to be disappointed. He may offer some hint about the controversial border adjustment. Although he seems to want to punish importers and dismantle the global supply chains, there are legal and practical constraints. News that he will not support the currently construed board adjustment in the GOP plan helped spark a late rally in retail shares before the weekend.

Many investors continue to grapple with Trump’s concrete policies, and the priorities are becoming clearer. His infrastructure initiative does not appear to be a 2017 priority. Treasury Secretary Mnuchin suggested that he was hopeful of an agreement on taxes by the congressional recess in August. This may prove optimistic, especially if the repeal and replacement of the national healthcare take long. The end of taxes associated with it was expected to help fund the other tax cuts.

The threat to cite China as a currency manipulator on day one proved to be bluster. Mnuchin suggested that no judgment will be made until the April review as part of the Treasury’s Congressional mandated report on the international economy and the foreign exchange market. Under the current criteria, China is not guilty of currency manipulation. Both Bush and Obama had indicated, when they were on the campaign trail, that they would cite China too. However, as they became aware of the facts and the framework, they too refrained from citing China. If the Trump Administration moves toward a valuation metric, it would also be difficult to cite the yuan as many models suggest it is near fair value. The BIS measure of China’s real equilibrium exchange rate pulled back early last year but has been trending higher since last August.

As the macroeconomic developments seem fairly stable, the focus is on politics. The premium France offers over Germany narrowed last week in both the short- and long-end of the yield curve. The German two-year yield fell to new record lows and is approached minus 100 basis points. This has widened the spread between the US and Germany, for which the euro is particularly sensitive. As we noted previously, the 0.65 correlation (60-day on percent change basis) between the two-year spread and the euro is relatively strong. Similarly, the yen’s correlation with the 10-year differential between the US and Japan (60-day percent change basis) is 0.77, the strongest in more than a decade.

Lastly, we note that the correlation between the S&P 500 and the VIX futures contract has been inversed since at least 2004 when our time series began. However, now the inversion (~-0.44) is the least in two years. It has rarely gone above -0.40. We understand this to be partly an indication that there is some sort of floor the VIX. It may reflect the demand for insurance through the options market. It means that the equity market could continue to rise (the S&P 500 is on a five-week advancing streak), but without the VIX falling. Over the five-week streak, the VIX has been in a saw-tooth pattern, alternating on a weekly basis between gains and losses, and is net-net flat.

Full story here Are you the author?Tags: #USD,$AUD,$CAD,$EUR,$JPY,EUR/GBP,Federal Reserve,newslettersent