Stock MarketsEM FX ended the week mixed. Markets continue to grapple with the outlook for the so-called Trump Trade, which we believe is intact. MXN and TRY recovered from the relentless selling of recent days, but both remain vulnerable. Indeed, if the jump in US yields on Friday continues this week, most of EM should remain under pressure. |

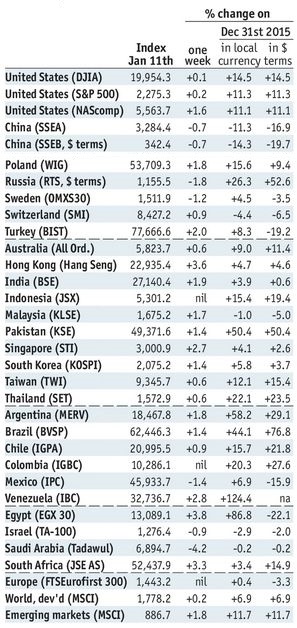

Stock Markets Emerging Markets January 16 Source: Economist.com - Click to enlarge |

IndiaIndia reports December WPI Monday, which is expected to rise 3.50% y/y vs. 3.15% in November. December CPI came in slightly lower than expected at 3.41% y/y, and so there are some downside risks to WPI. RBI next meets February 8 and it will be a tough call since the impact of the November demonetization is still being felt in the economy.

RussiaRussia reports November trade Monday. Exports are seen contracting -2.7% y/y, while imports are seen rising 5.1% y/y. As a result, the 12-month surplus is expected to narrow to $88.5 bln from $90.1 bln in October and would be the lowest since February 2005. Q4 current account data will be reported Tuesday and is expected at $7.4 bln. If so, the 4-quarter surplus would fall to $21.8 bln, the lowest since Q3 1999. Higher oil prices should prevent the external balances from deteriorating further in 2017.

SingaporeSingapore reports December trade Tuesday. NODX is expected to rise 7.0% y/y vs. 11.5% in November. Despite the trade data, the economy remains a bit soft, but rising price pressures are likely to keep the MAS on hold at its semiannual policy meeting in April.

MalaysiaMalaysia reports December CPI Wednesday, which is expected to rise 1.9% y/y vs. 1.8% in November. Bank Negara meets Thursday and is expected to keep rates steady at 3.0%. The bank has been on hold since the last 25 bp cut back in July. It does not have an explicit inflation target, but rising price pressures are likely to prevent any further easing for now.

South AfricaSouth Africa reports December CPI Wednesday, which is expected to rise 6.5% y/y vs. 6.6% in November. It also reports November retail sales that same day, which are expected at -0.4% y/y vs. -0.2% in October. Inflation remains above the 3-6% target range, but the firm rand has allowed SARB to keep rates steady since its last 25 bp hike to 7% back in March. Next policy meeting is January 24 and no change is expected.

ColombiaColombia reports November IP and retail sales Wednesday. With the economy remaining sluggish, the central bank is likely to continue the easing cycle with another 25 bp cut to 7.25% at its next policy meeting January 26. New central bank Governor Echavarria said he favors rate cuts “as soon as we can.”

IndonesiaBank Indonesia meets Thursday and is expected to keep rates steady at 4.75%. CPI rose only 3% y/y in December, near the cycle lows and right at the bottom of the 3-5% target range. Taken along with the firm rupiah, we see a small chance of a dovish surprise. BI has been on hold since the last 25 bp cut back in October.

BrazilBrazil reports mid-January IPCA inflation Thursday, which is expected to rise 6.14% y/y vs. 6.58% in mid-December. Falling inflation allowed the central bank to cut rates by a bigger than expected 75 bp last week, and it is likely to follow up with another 75 bp at the next meeting February 22. Minutes from this month’s COPOM meeting may be released on Tuesday.

PolandPoland reports December industrial and construction output and retail sales Thursday. Data is expected at y/y rates of 1.6%, -12.9%, and 6.9%, respectively. Meanwhile, price pressures are rising. CPI rose 0.8% y/y in December, the highest since October 2013 and likely to rise further. The central bank has said tightening was unlikely until 2018, but we think rate hikes will start this year.

ChileChile central bank meets Thursday and is expected to cut rates 25 bp to 3.25%. If so, this would mark the start of the easing cycle after rates have been kept steady since the last 25 bp hike back in December 2015. Inflation has been below the 3% target for three straight months and within the 2-4% target range for five straight. The peso has also remained fairly firm, giving the bank leeway to cut sooner rather than later.

ChinaChina reports December IP, retail sales, and Q4 GDP Friday. IP and retail sales are expected to slow modestly to 6.1% y/y and 10.7%, respectively, while GDP growth is expected to remain steady at 6.7% y/y. Despite concerns about capital outflows from China, we think CNY/CNH will follow the broader EM FX trend.

TaiwanTaiwan reports December export orders Friday, which are expected to rise 9.0% y/y vs. 7.0% in November. With the mainland economy improving, it’s no surprise that Taiwan is feeling some impact. Export orders have risen y/y for four straight months, while exports have risen y/y for three straight months and in five of the past six.

|

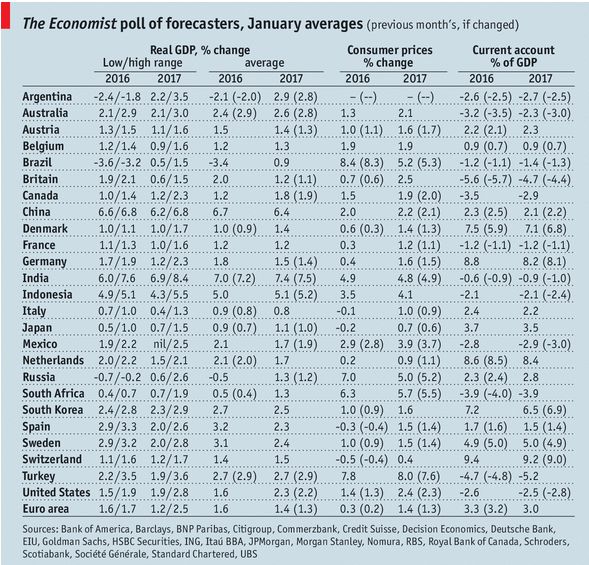

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, January 2017 Source: Economist.com - Click to enlarge |

Win Thin is a senior currency strategist with over fifteen years of investment experience. He has a broad international background with a special interest in developing markets. Prior to joining BBH in June 2007, he founded Mandalay Advisors, an independent research firm that provided sovereign emerging market analysis to institutional investors. He received an MA from Georgetown University in 1985 and a B.A. from Brandeis University 1983. Feel free to contact the Zurich office of BBH

Tags: Emerging Markets,newslettersent,win-thin