Stock MarketsEM ended the weak on a soft note, as the hawkish Fed decision continued to have reverberations for global markets. Worst performers in EM last week were CLP (-3.3%), ZAR (-2%), and KRW (-1.5%). With little fundamental news expected this week, markets may take a more consolidative tone, especially with the holidays approaching. However, we continue to believe that the global backdrop for EM remains negative. Several EM central banks meet, including Turkey, Hungary, Czech Republic, the Philippines, Taiwan, and Thailand. None are expected to move except Turkey, which is likely to hike rates for the second straight month in response to the weak lira. We were surprised by Colombia’s rate cut last Friday, and expect the peso to open weaker this week as a result. |

Stock Markets Emerging Markets December 14 Source: Economist.com - Click to enlarge |

PolandPoland reports November industrial and construction output, real retail sales, and unemployment Monday. Consensus forecasts are 1.7% y/y, -18.9% y/y, 5.3% y/y, and 5.5%, respectively. Central bank minutes will be released Thursday. Recently, central bank Governor Glapinski said that the next move is likely to be hike but unlikely until 2018. CPI was flat y/y in November, the first non-negative reading since June 2014. Low base effects should see the y/y move sharply higher in 2017, and should move the timing of the first rate hike forward into 2017. TaiwanTaiwan reports November export orders Tuesday, which are expected to rise 6.0% y/y vs. 0.3% in October. The central bank meets Thursday and is expected to keep rates steady at 1.375%. The last move was a 12.5 bp cut back in June, and then left rates steady at its next quarterly meeting in September. November IP will be reported Friday, and is expected to rise 5.2% y/y vs. 3.7% in October. TurkeyTurkey’s central bank meets Tuesday and is expected to keep the benchmark rate steady at 8.0%. However, the market is split. Of the 20 analysts polled by Bloomberg, 11 see no hike, 7 see a 25 bp hike, and 2 see a 50 bp hike. Most see a 25 bp hike to the top of the rates corridor to 8.75%. CPI rose 7% y/y in November, the lowest since but still at the top of the 3-7% target range. With the lira remaining weak and oil prices rising, we think price pressures are likely to pick up and will require further tightening in 2017. HungaryHungary’s central bank meets Tuesday and is expected to keep rates steady at 0.9%. It has kept rates steady since the last 15 bp cut back in May. However, it has eased via unconventional measures since then, pushing market interest rates even lower to new record lows. CPI rose 1.1% y/y in November, the highest since September 2013 and approaching the 2-4% target range. Base effects should boost it further in the coming months. Taken in conjunction with the recent proposal to boost the minimum wage next year, we think further easing is unlikely. BrazilBrazil reports November current account and FDI data Tuesday. It then reports mid-December IPCA inflation Wednesday, which is expected to rise 6.77% y/y vs. 7.64% in mid-November. If so, this would be the lowest rate in December 2014. COPOM highlighted the possibility of a faster easing cycle at its November meeting. Next COPOM meeting is January 11, and CDIs are currently pricing in a 50 bp cut to 13.75%. The central bank’s quarterly inflation report will be released Thursday. MalaysiaMalaysia reports November CPI Wednesday, which is expected to rise 1.3% y/y vs. 1.4% in October. Even though the central bank has no explicit inflation target, low price pressures are likely to keep it on hold for now. Next policy meeting is January 19, and no change is expected then. The last move was a 25 bp cut to 3% back in July. ThailandBank of Thailand meets Wednesday and is expected to keep rates steady at 1.5%. CPI rose 0.6% y/y in November, below the 1-4% target range but the highest since December 2014. Low base effects should see inflation move back into the target range in the coming months. Inflation is unlikely to rise enough to warrant a rate hike, but it should keep the BOT cautious and on hold for now. PhilippinePhilippine central bank meets Thursday and is expected to keep rates steady at 3.0%. CPI rose 2.5% y/y in November, within the 2-4% target range and the highest since February 2015. Rates have been kept steady since it shifted to a new policy framework in May. We believe the next move is likely to be a hike by mid-2017. Czech Republic

|

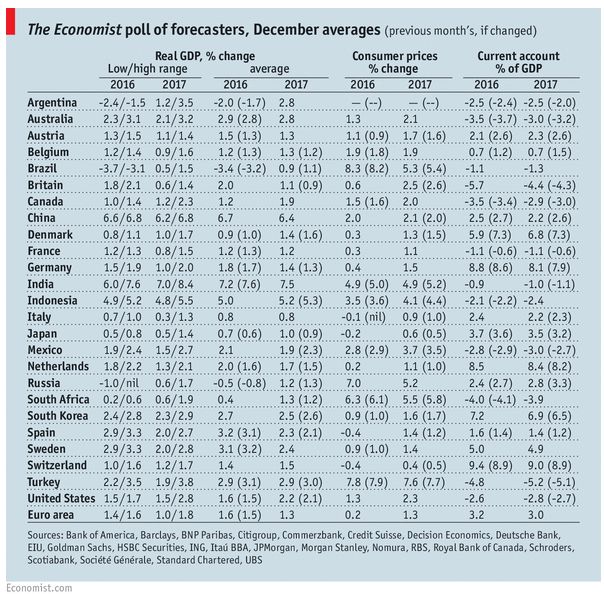

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, December 2016 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin