Summary

Stock MarketsIn the EM equity space as measured by MSCI, Hungary (+4.3%), Russia (+3.2%), and Turkey (+2.3%) have outperformed this week, while Brazil (-3.8%), China (-3.6%), and Chile (-3.5%) have underperformed. To put this in better context, MSCI EM fell -2.3% this week while MSCI DM fell -0.1%. In the EM local currency bond space, Poland (10-year yield -15 bp), Korea (-4 bp), and Czech Republic (-4 bp) have outperformed this week, while the Philippines (10-year yield +41 bp), Indonesia (+32 bp), and Hong Kong (+32 bp) have underperformed. To put this in better context, the 10-year UST yield rose 12 bp this week to 2.59%. |

Stock Markets Emerging Markets December 14 Source: Economist.com - Click to enlarge |

ChinaChina will raise the sales tax on small cars to 7.5% in 2017. The tax will be increased further to 10%, according to the Finance Ministry. The government cut this tax rate from 15% in October 2015 after lobbying from China’s auto association. Automakers had asked for the tax cut to be made permanent. TurkeyNew methodology used by Turkstat to measure Turkish GDP has led to significant upward revisions. Using 2009 as the new base year, the size of the economy last year was revised up by $140 bln to $862 bln total. Furthermore, 2015 growth was revised up from 4% to 6.1%. The revisions also improved upon previously reported figures for 14 of the last 15 years, and boosted the average growth rate for the last five years to 7.1% from 4.4% previously. Yet the lack of any detailed breakdown has left many investors skeptical. Turkish authorities are growing more concerned about the weak lira. Deputy Prime Minister Simsek said the government would be willing to help companies manage gaps in FX liabilities and assets. He added that the government may have to limit the amount of foreign currency debt that companies can issue. The central bank also warned that it can intervene directly in the FX markets to support the lira. Gross reserves stood at $98.6 bln for the week ended December 2, which is the lowest since May. ChiliFitch moved the outlook on Chile’s A+ rating from stable to negative. The agency warned that a prolonged economic slowdown is leading to “the most rapid erosion” of the sovereign balance sheet in the single-A category. Our own sovereign ratings model has Chile at A-/A3/A- and so we think there are clearly downgrade risks to actual ratings of AA-/Aa3/A+. Chile’s central bank kept rates steady at 3.5% but shifted to an expansionary policy bias. We don’t think this sift in bias was expected so soon. Yes, easing may be in the cards in 2017 but we don’t think they can cut anytime soon. CPI ticked up to 2.9% y/y in November, and is just below the 3% target. ColombiaColombia selected Juan Jose Echavarria to be the new central bank governor. He was a member of the central bank’s Board of Directors from 2003-2013. Echavarria is seen as a close ally of President Santos, advising him on economic affairs during Santos’ 2014 re-election campaign. His 4-year term will run from January 2017 to January 2021. Outgoing Governor Uribe held the post for three terms since taking the post in January 2005. MexicoFitch revised the outlook on Mexico’s BBB+ rating from stable to negative. We don’t agree with this since our model has Mexico at BBB+, which is where Fitch currently has it. Fitch said the move was due mainly to downside risks to growth, but noted that “the US presidential election has increased economic uncertainty and asset price volatility in Mexico.” Banco de Mexico hiked rates by a larger than expected 50 bp. This was the right move, but we do not think that MXN will see much long-lasting relief since EM remains under pressure. The hike was about more than just the peso, though. Price pressures are picking up and are likely to continue rising, so the 50 bp move is warranted. That said, the tightening cycle is going to hurt an already sluggish economy. |

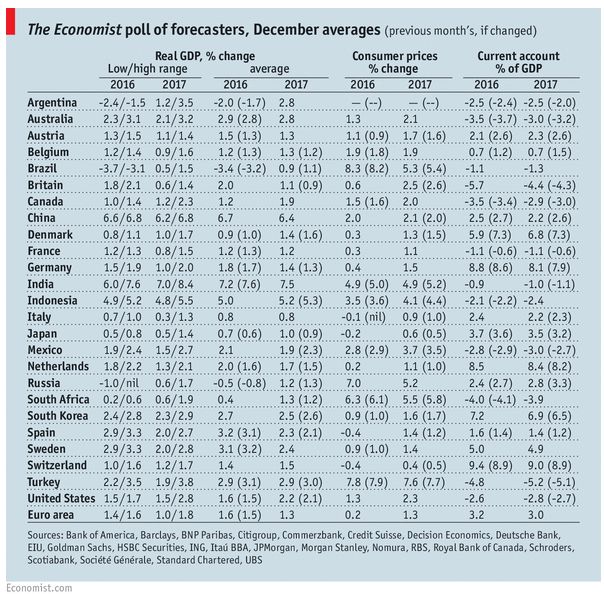

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, December 2016 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent,win-thin