Summary

Stock MarketIn the EM equity space as measured by MSCI, Brazil (+2.8%), Qatar (+2.3%), and Czech Republic (+0.5%) have outperformed this week, while the Philippines (-4.5%), Indonesia (-4.2%), and Chile (-3.9%) have underperformed. To put this in better context, MSCI EM fell -1.7% this week while MSCI DM rose 0.1%. In the EM local currency bond space, Brazil (10-year yield -47 bp), Colombia (-24 bp), and Turkey (-24 bp) have outperformed this week, while Hong Kong (10-year yield +25 bp), Taiwan (+9 bp), and India (+4 bp) have underperformed. To put this in better context, the 10-year UST yield fell 5 bp this week to 2.54%. In the EM FX space, BRL (+3.6% vs. USD), ARS (+2.3% vs. USD), and RUB (+1.6% vs. USD) have outperformed this week, while KRW (-1.6% vs. USD), MXN (-1.0% vs. USD), and EGP (-0.8% vs. USD) have underperformed. |

Stock Markets Emerging Markets December 14 Source: Economist.com - Click to enlarge |

ChinaChina President Xi raised the possibility of sub-6.5% growth. He said he is open to growth falling below the government’s target due to rising debt and concerns about the global outlook after Trump’s election victory. Xi added that the target does not have to be met if doing so creates too much risk. Fitch moved the outlook on Indonesia’s BBB- rating from stable to positive. This past quarter, our own sovereign ratings model showed Indonesia’s implied rating rising a notch to BBB/Baa2/BBB. We agree with this move and note that actual ratings of BB+/Baa3/BBB- all have upgrade potential. PhiippineThe Philippine central bank raised its 2017 inflation forecasts for 2017 and 2018 to 3.3% and 3.0%, respectively. CPI rose 2.5% y/y in November, within the 2-4% target range but the highest since February 2015. Rates have been kept steady since it shifted to a new policy framework in May. In light of the new inflation forecasts and upside inflation risks, we believe the next move is likely to be a hike in H1 2017. HungaryThe Hungarian central bank lowered the cap on the amount commercial banks can keep at its 3-month deposit facility to HUF750 bln for Q1. The last adjustment was back in September, when the cap was set at HUF900 bln for Q4. This unconventional policy is akin to monetary easing, as it pushes funds out of the central bank’s deposit facility and into government bonds and the interbank market. The end result has been lower government borrowing costs and lending rates. TurkeyTurkish Energy Ministry met with major power companies and asked them to lower the price of electricity. If not, the companies will face the imposition of a price cap. Electricity prices hit all-time highs this week, driven by a natural gas shortage. We have been concerned about growing inflation risks due to higher energy prices, but an artificial cap on electricity prices would only make things worse in the longer run. BrazilBrazil President Temer announced a package of measures to help boost the economy. The measures include strengthening collective bargaining laws, allowing workers’ early access to their severance funds, and lowering credit card interest rates. The weekly central bank survey saw the consensus for 2017 growth fall to 0.58% from 0.7% previously, while the central bank cut its forecast to 0.8% from 1.3% previously. ColombiaThe Colombian central bank surprised markets last Friday with a 25 bp cut to 7.5%. This was the first move since the last 25 bp hike back in July. The vote to cut was 4-3. This move was risky in this current environment, but it appears that the easing cycle will continue under the new Governor next month. |

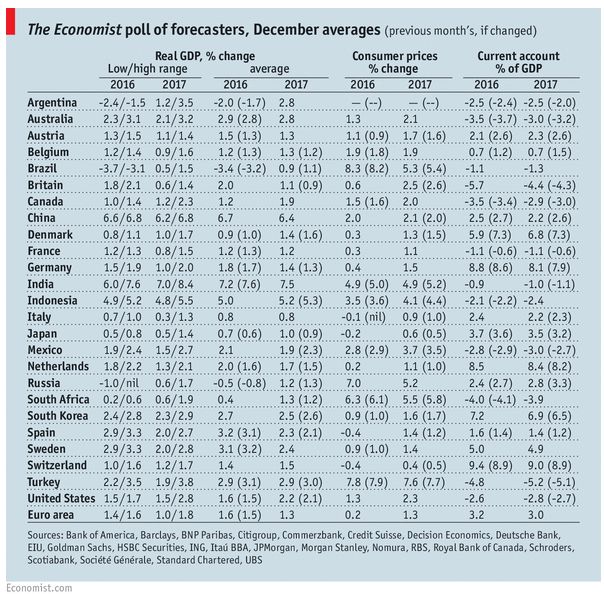

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, December 2016 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent