Stock MarketsEM gained some limited traction as last week ended. However, renewed concerns about China could limit this bounce as President Xi signaled the possibility that growth could fall below the government’s 6.5% target. China PMI readings out this coming weekend will be the first snapshot of December. Markets are likely to become more sensitive to Chinese data going forward. |

Stock Markets Emerging Markets December 14 Source: Economist.com - Click to enlarge |

IsraelBank of Israel meets Monday and is expected to keep rates steady at 0.10%. Deflation is persistent, with CPI at -0.3% y/y in November. Low base effects should move inflation into positive territory next year and into the 1-3% target range. This should prevent further easing by the central bank. Q3 GDP will be reported Thursday and growth is expected to remain steady at an annualized 3.2%. BrazilBrazil reports November central government budget data Monday, and the primary deficit is expected at -BRL38.0 bln. Consolidated budget data will be reported Tuesday, and the primary deficit is expected at -BRL54 bln. Recall that the October data were boosted by the tax amnesty scheme, and so November should show a return to the negative trend. December IGP-M wholesale inflation will be reported Thursday, and is expected to rise 7.02% y/y vs. 7.12% in November. KoreaKorea reports November IP Thursday, which is expected to rise 1.5% y/y vs. -1.6% in October. December CPI will be reported Friday, and is expected to rise 1.4% y/y. If so, it would be the highest since August 2014. Due to low base effects, inflation is likely to approach the 2% target next year, and this should keep the BOK in cautious mode. On Sunday, Korea reports December trade. Exports are expected to rise 4.6%, while imports are expected to rise 6.7% y/y. ThailandThailand reports November manufacturing production Thursday, which is expected to rise 0.3% y/y vs. 0.1% in October. The Bank of Thailand sees 3.2% GDP growth next year, about the same as 2016. However, it warned that the Thai economy faces greater uncertainty going forward due to the fragile global recovery. Trade and current account data will be reported Friday. ChileChile central bank releases its minutes Wednesday. Chile then reports November manufacturing production and retail sales Thursday. The former is expected at -1.2% y/y, while the latter is expected at +2.1% y/y. The economy remains weak, but we think inflation remains too high to justify a rate cut anytime soon. At 2.9% y/y in November, inflation is just below the 3% target. MexicoBanco de Mexico releases minutes from its December meeting Thursday. At that meeting, the bank hiked a larger than expected 50 bp to 5.75%. Mid-December inflation came in higher than expected, up 3.48% y/y. This is further above the 3% target (but still in the 2-4% target range) and the highest since December 2014. Next Banxico meeting is February 9. We had been thinking that if the Fed stands pat at its next meeting February 1, this would allow Banxico to stand pat too. But if renewed MXN peso weakness intensifies, Banxico may be forced into another hike. EgyptEgyptian central bank meets Thursday, and is expected to hike rates 25 bp to 15%. We see risks of a much larger move that would send a strong signal to the markets. CPI inflation accelerated to 19.4% y/y in November, the highest since November 2008. The Egyptian central bank hiked rates 300 bp to 14.75% when it floated the pound last month. It has not moved since. South AfricaSouth Africa reports November trade, money, and loan data Friday. Money and loan growth are both expected to slow from October. The trade balance has been improving in recent months, as exports have rebounded even as imports are constrained by sluggish demand. The current account gap rose to -4.1% of GDP in Q3, but could show improvement in Q4 due to the trade balance. TurkeyTurkey reports November trade Friday, which is expected at -$4.1 bln vs. -$4.2 bln in October. Exports have been weak in recent months. As higher energy prices boost imports, we expect the external accounts to worsen significantly next year. PolandPoland reports December CPI Friday, which is expected to rise 0.5% y/y vs. flat in November. If so, this would be the first positive reading since June 2014 and the highest since March 2014. This should prevent any further easing. Indeed, with low base effects likely to significantly boost inflation, the central bank may have to move up its forward guidance from the current view of the first hike in 2018. RussiaRussia reports December CPI Friday, which is expected to rise 5.6% y/y vs. 5.8% in November. If so, this would be the lowest since July 2012 and would justify the hawkish stance of the central bank this year. However, the bank said it could resume easing in H1 2017 if inflation continues to converge with the 4% target. ChinaChina reports official December PMI readings Sunday, with manufacturing seen at 51.6 vs. 51.7 in November. Markets were spooked by President Xi’s comments last Friday, when he said he is open to growth falling below the government’s target due to rising debt and concerns about the global outlook after Trump’s election victory. Xi added that the target does not have to be met if doing so creates too much risk. Markets are likely to become more sensitive to Chinese data going forward. |

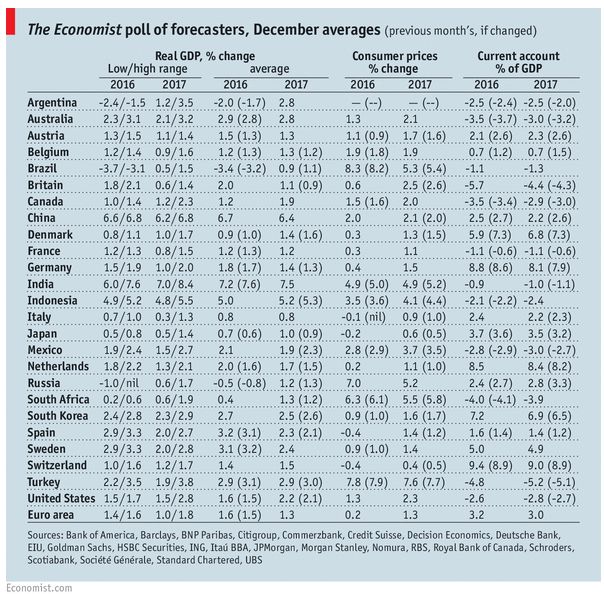

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, December 2016 Source: Economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Emerging Markets,newslettersent