George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

When Draghi extended QE in the November ECB meeting, it is was clear that Draghi was wrong. He is expecting lower inflation in 2018, maybe around 1%.

The SNB reduced her inflation expectation by 0.1% for both years again, 0.1% in 2017 and 0.5% in 2018.

Swiss National Bank leaves expansionary monetary policy unchangedThe Swiss National Bank (SNB) is maintaining its expansionary monetary policy. Interest on sight deposits at the SNB is to remain at–0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%. At the same time, the SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration. The SNB’s expansionary monetary policy is aimed at stabilising price developments and supporting economic activity. The negative interest rate and the SNB’s willingness to intervene in the foreign exchange market are intended to make Swiss franc investments less attractive, thereby easing pressure on the currency. The Swiss franc is still significantly overvalued.

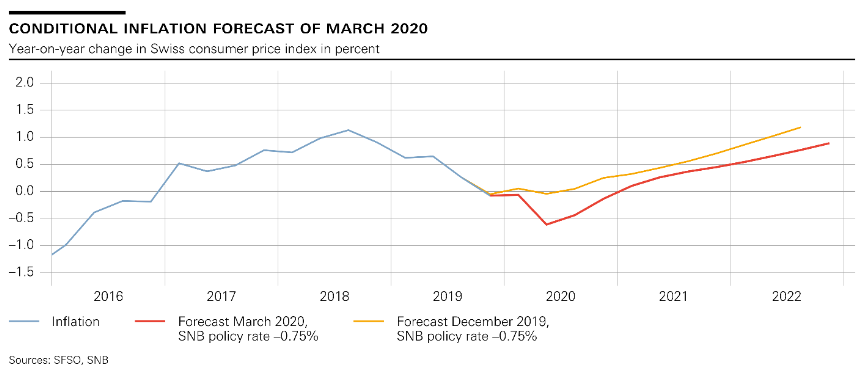

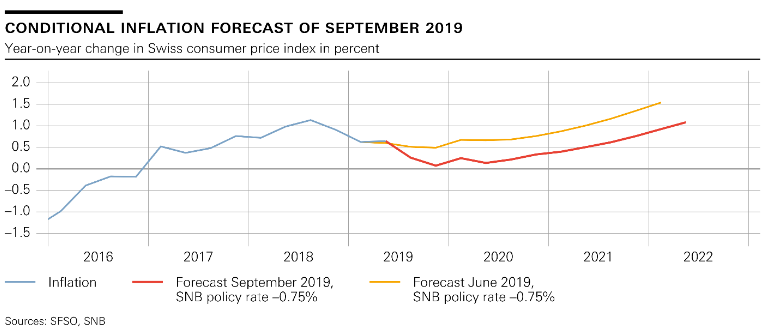

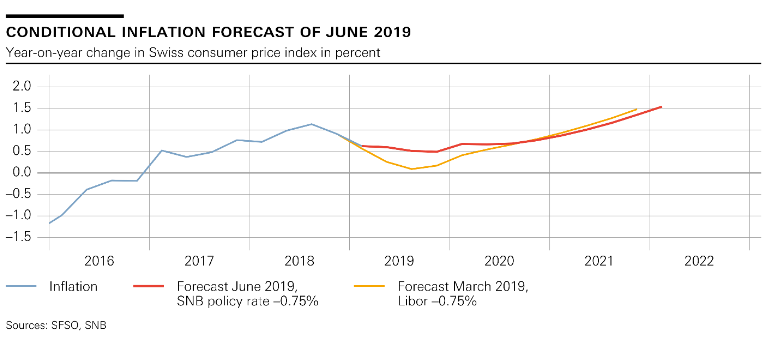

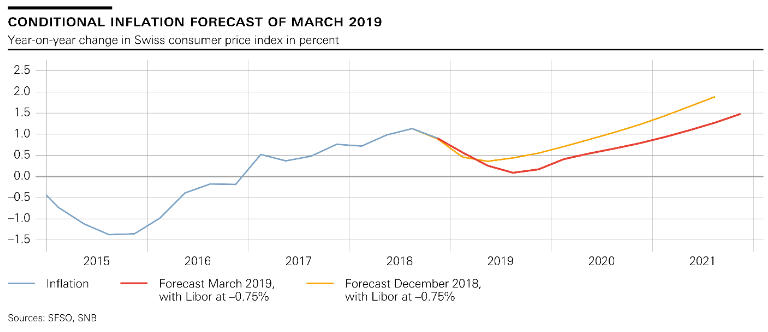

Compared to September, the new conditional inflation forecast has been revised slightly downwards in the short term. This mainly reflects the fact that inflation in October and November was slightly lower than expected. The SNB nevertheless anticipates an unchanged inflation rate of –0.4% for 2016. For 2017, however, the forecast is down to 0.1%, from 0.2% in the previous quarter. For 2018, the SNB now expects inflation of 0.5%, compared to 0.6% in the third quarter. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

The global economy has continued to recover inline with the SNB’s expectations. In the US, third-quarter GDP growth was again significantly above potential. Furthermore, the situation on the labour market continued to improve. The other major economic areas also recorded favourable economic activity in the third quarter. The euro area and Japan continued to register moderate growth, while in China, growth remained strong thanks to a variety of fiscal measures. In the UK, the economic impact of the Brexit decision has so far proved less pronounced than originally feared.

|

SNB Switzerland Conditional Inflation Forecast(see more posts on Switzerland inflation, ) Conditional Inflation Forecast - Click to enlarge |

|

The SNB expects the moderate pace of global growth to continue in 2017. The baseline scenario for the world economy is still subject to considerable risks, however. Structural problems in a number of advanced economies could negatively affect the outlook. Added to this are a multitude of political uncertainties which are particularly associated with the future course of economic policy in the US, upcoming elections in several countries in the euro area as well as the complex and arduous exit negotiations between the UK and the EU.

According to an initial quarterly estimate, GDP in Switzerland grew at an annualised rate of 0.2% in the third quarter. This small increase must also be seen in the context of high growth in the second quarter. Year-on-year, GDP rose by 1.3% in the third quarter. Overall, economic indicators point to a continuation of the moderate economic recovery in Switzerland and are thus consistent with our previous GDP growth forecast of around 1.5% for 2016 as a whole. Developments on the labour market support this view. Up until November, the seasonally adjusted unemployment rate for this year was stable at 3.3%. Survey-based labour demand indicators have recovered further.

The outlook for the coming year is cautiously optimistic. As for 2016, the SNB expects GDP growth for 2017 to be roughly 1.5%. Prevailing international risks mean that forecasts, including Switzerland’s, continue to be fraught with considerable uncertainties.

Over the last six months, growth on the mortgage and real estate markets has remained fairly constant at a relatively low level. At the same time, imbalances on these markets have decreased slightly overall due to developments in fundamentals. However, imbalances are still at a similarly high level as in 2014, when the sectoral countercyclical capital buffer was set at 2%. The SNB will continue to monitor developments on these markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

|

Switzerland Inflation and Inflation Forecast(see more posts on Switzerland inflation, ) Observed/Conditional Inflationn - Click to enlarge |

Full story here Are you the author?

The Swiss National Bank conducts the country’s monetary policy as an independent central bank. It is obliged by the Constitution and by statute to act in accordance with the interests of the country as a whole. Its primary goal is to ensure price stability, while taking due account of economic developments. In so doing, it creates an appropriate environment for economic growth.

Tags: newslettersent,Switzerland inflation