Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

High frequency economic reports will be not be among the key drivers of the capital markets in the week ahead. The light schedule, consisting mostly of industrial production in Europe, inflation for Scandinavia, and US retail sales, will have minimal impact on rate expectations.

A November rate Fed move was never very likely. The September employment report needed to be amazingly strong to boost the chances, and it was not. To overcome tradition, and the logistical difficulty of arranging a unscheduled press conference, without word leaking out, a greater sense of urgency would need to be present. Recent comments by the Fed’s leadership, especially most recently Fischer and Dudley expressed no such thing.

Our own calculation based on the November Fed funds futures contract that the market is discounting about a 7% chance of a hike on November 2. The CME puts the odds a little above 10%, while Bloomberg has it at 17%. The most important real sector data in the week ahead is the retail sales report. Like the employment data, a solid even if not spectacular retail sales report is expected. American households are not shopping like they did in Q2 when consumption rose 4.3% at an annualized pace, but a 2.8%-3.0% rate should be sufficient to lift growth above what the Fed now estimates as trend (1.8%).

EurozoneGerman, French, and Spanish industrial output were released before the weekend, and each was better than expected, suggesting a robust aggregate report. The ordoliberalism that Draghi acknowledges is part of the ECB’s DNA does not see monetary policy as a tool to stimulate growth. It is primarily to regulate the general price level. Draghi had also indicated that the asset purchases would not stop abruptly. This meant it seemed that the ECB would decide to taper its purchases, like the Fed, did in QE3, rather than stop them cold. The press report confirmed that. We are skeptical in reading any more into it. There was no indication that the ECB was considering an early exit, and indeed, the original report acknowledged that the 80 bln euro a month asset purchases could be extended. We suspect there is reasonably strong chance that the asset purchases are extended beyond the current soft end date of March 2017. Risks are still biased to the downside. However, even if it decides to taper after March, that would still imply purchases all next year, and the likely need to modify its self-imposed rules to ensure minimal disruption via shortages of particular instruments. The least controversial measure may be to have the deposit rate (minus40 bp) yield floor apply to portfolio averages rather than individual instruments. It has not been Greek or Italian banks that have roiled the market. It has been Germany’s largest bank. What the problem has is not a function of bad loans, but asset valuation and capital needs, especially in light of what may still be a steep fine for its handling, presentation and sales of residential mortgage securities in the United States. Deutsche Bank stock rose in the last four sessions of the week, to make for a second weekly advance. The share price in Germany has approached an important technical area. On September 16, shares gapped lower, and subsequent price action has left the gap unfilled. It is found between 12.48-12.81 euros. Share closed near 12.17 before the weekend. A move above the gap, and ideally 13.00 would neutralize some of the bearish technical pressure. However, the new found stability may be challenged by new reports that contrary to earlier claims, there has been no compromise struck between the US Department of Justice and Deutsche Bank executives to reduce the fine.. |

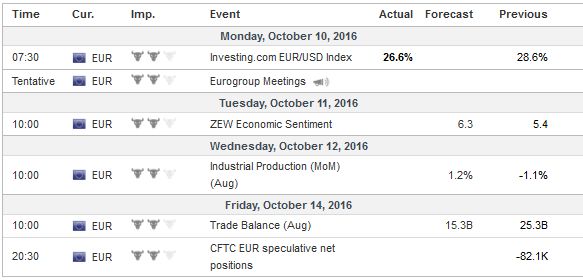

Economic Events: Eurozone, Week October 10 Economic Events: Eurozone, Week October 10 - Click to enlarge |

United KingdomEconomic data does not help very much to explain sterling’s movement. The fact of the matter is that the UK has fared well in the three and half months since the referendum. The Bank of England took pre-emptive moves. These included deferring regulatory capital increase for banks, low interest rate loans, a formal cut in the base rate, and a new asset purchase plan that includes corporate bonds for the first time. Sterling has depreciated by nearly 16.5% against the dollar since the referendum and about 13.5% on a trade-weighted basis. Even before the flash crash on October 7, sterling had been under pressure over the past several weeks. Most recently Prime Minister May gave official sanction to talk that Article 50 will be triggered at the end of Q1 17. Just as importantly, her comments suggesting an increase risk of a hard exit, whereby the UK would give up access to the single market in orders to gain more control over its immigration, weighed on the currency. Both Merkel and Hollande have also signaled their unwillingness to compromise on the basic principles. In effect, investors have voted with their wallets that the UK out of the EU is less attractive, and have marked down the value of all the assets in the country. The rally in stocks (FTSE 250) have not offset the decline in sterling for foreign investors. UK bond yields have fallen since the referendum, but as global yields rise, UK yields rose fastest. Last week, for example, the UK 10-year gilt yield increased 23 bp. The US 10-year yield rose almost 10 bp, while the Germany 10-year yield increased by a little more than 11 bp. The same is true at the shorter end of the coupon curve. The UK two-year yield increased by eight bp. EMU yields were 1-3 bp higher, and the US two-year yield was increased by nearly four bp. The UK is at risk of a vicious cycle. For structural reasons, there is an efficient pass through of inflation from a weaker currency. There is also a relative quick pass-through of higher rates to UK households via the prevalence of adjustable rate mortgages. UK rates can rise even while the BOE is buying gilts. The depreciation of sterling will have an impact on the UK current account balance. It will be reduced, but do not be surprised if it comes from reduced volume imports as much as an increase in value exports. |

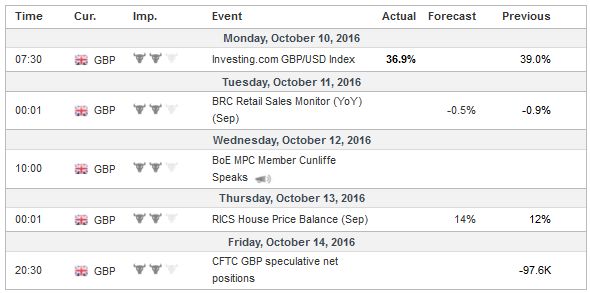

Economic Events: United Kingdom, Week October 10 Economic Events: United Kingdom, Week October 10 - Click to enlarge |

United StatesThe US corporate earnings season formally begins this week. In truth it has already begun; 5% of the S&P 500 have reported Q3 earnings. According to Factset, 20 have exceeded earnings per share expectations, and 15 surpassed sales expectations. Still, Q3 is still expected to be the sixth consecutive quarter that earnings per share will fall on a year-over-year basis. A 2.1% decline is expected. We note that US money market reforms are effective October 14. Recall that money markets that invest strictly in US government securities can be fixed at $1 a share and face no liquidation barriers. If one wants a higher yielding money market product, it comes with additional risks. The fund can invests in non-government paper but has the right to impose liquidation barriers, and the price fluctuates. This has pushed up LIBOR. Indeed the increase in LIBOR, which despite its shortcomings remains a key element in the pricing of derivatives, including cross currency swaps. Some have suggested that this may have been one of the considerations behind the Federal Reserve’s reluctance to raise the Fed funds target in September. Many foreign banks were chastened from using the US money market to secure dollar funding during the Great Financial Crisis. However, Japanese banks appear to have been a notable exception. Recent reports suggest a few large Japanese banks have been boosting their share of US deposits as an attempt to replace what has become high cost (higher interest rate) funds selling money market instruments. The Financial Times, citing publicly available documents, reported that one bank increased foreign currency deposits by $13.8 bln in Q2 and another by $28 bln in the year through June. Lastly, there has been much talk of an October surprise in the US Presidential contest. And indeed there has been such a surprise that could very well not only determine the national presidential race, but also the control of the legislative branch. There have been two such surprises. WikiLeaks show Clinton campaign as strategic opportunist, and may deepen fissure with Sanders’ supporters. However, there are a couple of mitigating factors. Sanders is not a Democrat. The Democratic Party helps its party members. In addition, since getting Sanders’ endorsement, Clinton has moved into the space seemingly abandoned by the Republican Convention of what are known as the three-Fs (faith, family and flag) to appeal to independents and the so-called Reagan Democrats. The other mitigating factor is the other October surprise, and that is the implosion of Trump’s campaign. Ironically, unlike the private email made public in the WikiLeaks, the Trump tapes have been in the public space. They have not been brought to the public’s attention by Trump’s adversaries. Until now neither the traditional or social media have not covered it. Struggling since the fallout from the first debate, Trumps tapes proved the final straw for many in the Republican establishment who had gone along with the results of the primary contests. Reports indicate that at least 15 Republican Senators, 25 Representatives, and six Governors have either retraced their previous support for called for Trump to step down. A poor performance in Sunday’s debate that lacks a contrite apology could see defections grow. Note that voting has already begun in a dozen states, and absentee ballots have been mailed. There does not appear to be a mechanism to force Trump off the ticket, and the candidate has denied such intentions. Reports indicate the Trump’s running mate Pence has canceled his scheduled appearances, and there is some speculation that he could step down. The impact on Senate and House races will be closely scrutinized. There is still a greater chance that the Democrats capture the Senate, but some polls suggest the House is in play as well. |

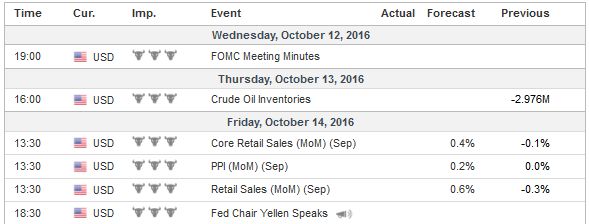

Economic Events: United States, Week October 10 Economic Events: United States, Week October 10 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week October 10 Economic Events: Switzerland, Week October 10 - Click to enlarge |

Understanding sterling’s pre-weekend dramatic price action requires sensitivity to both micro and macro forces. Micro factors can include things like uneven liquidity, role of computerized trading, changing market participation (few bank proprietary dealers), fragmentation of the foreign exchange market, and the role of derivatives (e.g. reverse knock-in or knock-out options, one-touch options). Macro factors may include central bank induced decline in volatility (higher bond and stock prices) and the occasional spikes.

Other currencies, like the Swiss franc, New Zealand dollar, and South African rand have experienced dramatic moves, often associated with a fundamental cause. There have also been large move in yen. Outside the currencies, there have been dramatic moves in a short period even in US Treasury bonds, one of the most liquid instruments in the world.

Sharp moves like sterling experienced before the weekend, clears the order books, in the sense that any reasonable stop (either to liquidate a long or enter a short position) below the market was probably triggered. In such a situation, we have found a period of consolidation is likely, but often those ghost prices–extremes–are revisited over the medium term.

OPEC and non-OPEC members meet in Istanbul in the week ahead. Oil prices remain elevated, after rallying for the past three weeks and four of the past five weeks. Technicals are getting stretched, and we would be on the lookout for a near-term reversal. Nothing new will likely come from the meetings. Details are due next month, and we remain skeptical. The difference in estimates could account for the bulk of the production adjustments.

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,$JPY,newslettersent,OIL