Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Four central banks meet, but expectations for fresh action are low.

The US latest election news does not appear to be altering the projected electoral college outcome.

UK press are speculating about Carney possibly resigning. We are skeptical.

The week ahead features four central bank meetings, the PMIs that begin the monthly cycle of high frequency data, and the US employment report.Here was sketch out the main impulses from the US, EMU, UK, Japan, Canada, and Australia.

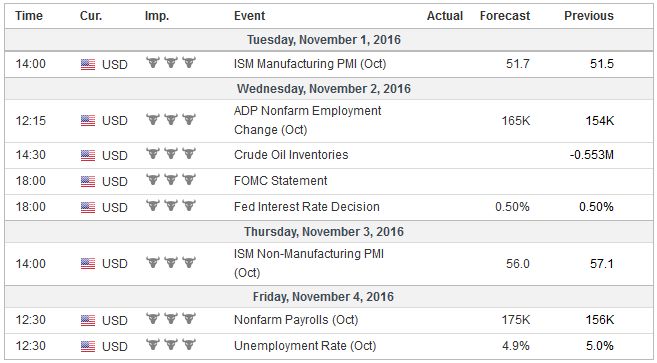

United StatesThere are three drivers: politics, FOMC meeting, and the employment report. First, as we saw before the weekend, despite most polls and predictive markets showing Clinton with a large lead, investors realize that as unlikely as a Trump victory may be the impact could potentially be huge. In addition, even though most polls shows the UK referendum was a close call, many insist that polls underestimate the strength of insurgency movements. Barring a specific “smoking gun,” we do not expect the re-opening of Clinton’s email investigation to significantly alter voter preferences. The probability of a Trump victory had already begun stabilizing and recovering a little. A few swing states seemed fluid and may have swung toward Trump, but not enough to change the likely electoral college outcome. The odds also favor the Democrats taking the Senate by a slim majority. The Democrats had little chance to garner a majority in the House of Representatives, and this does not appear to have changed either. The reaction to the news in thin pre-weekend activity gave investors a sense of what to expected our assessment is wrong. Speculators will likely sell the Mexican peso, and the Canadian dollar will underperform. The euro and yen may be among the biggest beneficiaries. Stocks will sell-off and bonds will rally. Second, there is practically no chance that the Federal Reserve changes policy at this week’s FOMC meeting. A move this close to the election would be unprecedented. The Fed’s forecasts (dot plot) will not be updated, and there is no press conference scheduled. While these obstacles are not impossible to overcome, they are formidable. Moreover, the hawks on the Fed recognize this and do not appear to be pushing for a hike now, but that does not mean that there won’t be any dissents. To the contrary, we expect 2-3 dissents. The FOMC statement is unlikely to change substantively. There will be some minor tweaks to recognize the recent data and the improved growth. Last October, the FOMC statement pre-committed itself to a hike in December. We don’t think the Fed has to go to this extreme now. The market is pricing in a 70%-75% of hikes before the end of the year. A year ago the odds were around half as much. The Fed can indicate that the bar to a hike is low, needing only continued improvement in the data and no major negative shocks. Third, the US employment data is one of the most important high frequency economic reports. It often sets the tone for the economic data for the entire month, and the Federal Reserve has shown that it is sensitive to the monthly prints. We expect job growth slowed a little, but it will not challenge the December hike scenario, especially if we are right about the FOMC guidance and the economic threshold for the second hike in two years. We expect that the proximity of full employment and the emerging skills shortage will see wage pressures continuing to increase. As seen with the initial estimate of Q3 GDP, which at 2.9% was stronger than most forecasts, there was a little reaction, so too we expect little sustain reaction to the employment data. Barring a significant surprise, it will not impact policy expectations, and there the Fed will see another job report before the December meeting. |

Economic Events: United States, Week October 31 . - Click to enlarge |

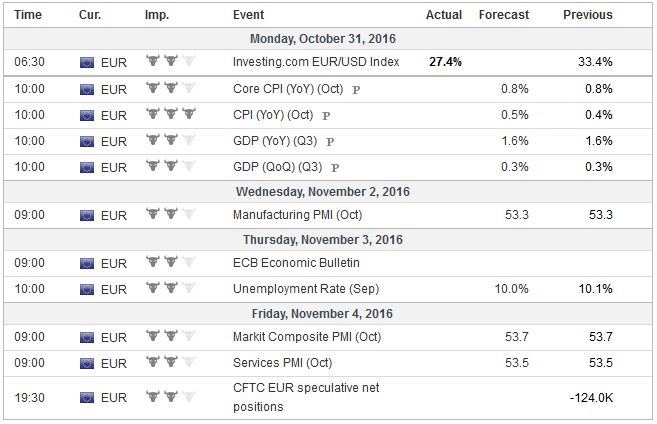

EurozoneThe eurozone reports the three most important macroeconomic data points: GDP, inflation, and unemployment. Eurozone growth in Q3 is expected to be at 0.3%, with the year-over-year pace near 1.6%, which is close to what economists regard as a trend. The preliminary estimate of October CPI is for a continued gradual move higher (0.5%-0.6%). However, the risk is that the gain is a function of energy prices. A fall in the core rate from 0.8%, which some economists forecast, would likely counter the headline increase and weigh on the euro on ideas that it make it more likely that the ECB extends its asset purchases when it meets in December. The unemployment rate may slip to 10.0% from 10.1%. The main weight on the euro has been renewed focus on the divergence of monetary policy. This is not simply a function of high frequency data. Both sides of the policy divergence are in play. There is a very strong likelihood that the ECB extends its asset purchases beyond next March. Barring a significant downside economic surprise or a new global shock, the Fed is likely to hike rates in December. The euro has found support near $1.0850. There is scope toward around $1.1050 within a near-term consolidative/corrective phase. |

Economic Events: Eurozone, Week October 31 . - Click to enlarge |

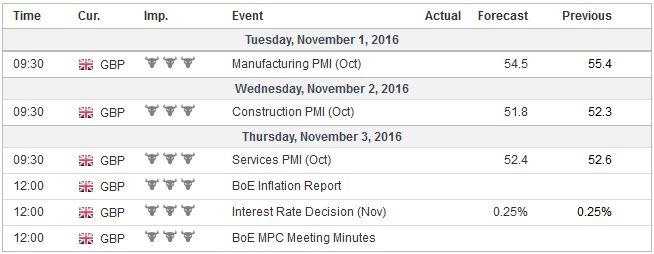

United KingdomOf the four central banks that meet, the Bank of England is the most likely to change policy.There are a few economists that expected the MPC to deliver a 10-15 bp rate cut. We expect no change in policy. Carney has been clear about his distaste for negative rates. This means that there is scope for one more and a small one at that. The does not have to be a hurry to deliver it, and it probably wouldn’t have much economic impact in any event. Although the economy continues to show little impact from the late-June decision to leave the EU, the growth risks are on the downside and inflation on the upside. Carney was also clear. Sterling is not a target of policy, though that does not mean the BOE is indifferent to it. Since the flash crash, it has begun stabilizing at lower levels against the dollar and the euro. The November inflation report will be issued at the conclusion of the BOE meeting. It has taken on new importance amid speculation that Carney may use that forum to announce his plans. There is much speculation in the UK press that Carney may resign. The ostensible reason is the broad criticism from government and several MPs. We suspect that what is really at stake is whether Carney signs on full-term (2021) or keep to the initial agreement to leave in 2018. Nevertheless, if we are wrong and Carney does step down early, investors will see this as a result of the encroachment on the central bank’s independence, and take sterling lower Ahead of the BOE meeting, the UK’s three PMIs ( manufacturing, construction, services) will be released. Sterling is not being driven by the high frequency data, but by the prospects of the UK losing access to the single market. The economy is presently growing near-trend, and the expected softening of the PMIs will likely be minor. |

Economic Events: United Kingdom, Week October 31 . - Click to enlarge |

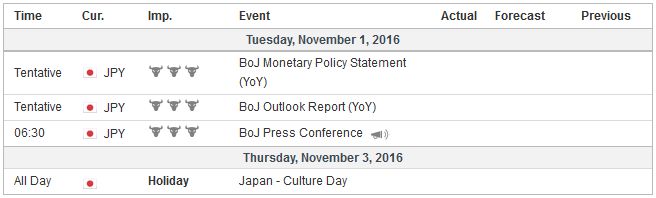

JapanThe Bank of Japan recently adopted a new policy framework. This week’s meeting is too soon to expect new changes. Two of the 43 surveyed by Bloomberg expect the BOJ to take the negative deposit rate, which applies to a relatively small fraction (compared with other central banks) of reserves, to minus 20 bp. There is some speculation that the BOJ could push out again when it will achieve its inflation target. We argue the BOJ may be better served to adopt the practice of other major central banks and have a medium-term inflation target, rather than a date-specific target. |

Economic Events: Japan, Week October 31 . - Click to enlarge |

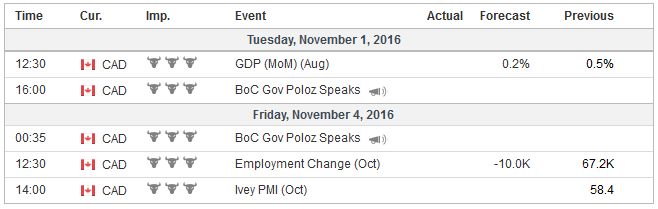

CanadaThe Fall Economic Statement on November 1 may not appear on many economic calendars, but it is an important input to monetary policy. Given the central bank’s recent cut in its GDP forecasts (to 1.2% this year from 1.4% and 1.8% next year from 2.2%) may induce the government to provide more fiscal stimulus, in addition to details for its infrastructure spending. Governor Poloz acknowledged that easing was actively discussed at the last Bank of Canada meeting. If the government does not provide more fiscal support, such discussions will likely continue. Canada is one of the only high income countries that reports monthly GDP figures. Shortly before the Fall Economic Statement, the August GDP estimate will be reported. A small gain (~0.1%-0.2%) is expected, owing primarily to manufacturing and wholesale trade. Mining (including oil and gas) recovered from the spring wildfires earlier and growth has flattened. Still, the Bank of Canada’s monetary policy review earlier this month offered a modest 3.2% Q3 GDP forecast. If the economy does expand by 0.2% in August, the forecast would seem to anticipate a weaker September. At the end of the week, Canada, like the US reports October jobs. The outsized 67.2k headline gain in September was misleading. It was three-quarters part-time jobs. Job losses in the service sector are expected to produce an overall 10k job loss in October. The unemployment rate is expected to hold steady at 7.0%. At the same time, Canada reports its September trade balance. The trade performance is gradually improving, and the trend is likely to remain intact. We do not see an immediate impact from the free-trade agreement with the EU. |

Economic Events: Canada, Week October 31 . - Click to enlarge |

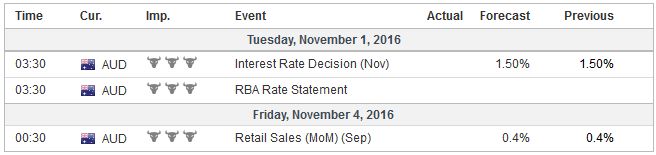

AustraliaThe Reserve Bank of Australia meets on November 1. Some economists expect a rate cut, but we do not. Former Governor Stevens and his successor Lowe indicated that the RBA would not respond mechanically to the undershoot of inflation. They have indicated provided growth, and the labor market does not deteriorate, the RBA is not in anxious about cutting rates further from the record low levels. The housing-related data remain firm. The Australian dollar remains resilient even though $0.7700 ceiling is proving formidable. Australia’s relatively high-interest rates and AAA rating are important attractors. The rally in industrial metals and better terms of trade are frosting on the fundamental cake. |

Economic Events: Australia, Week October 31 . - Click to enlarge |

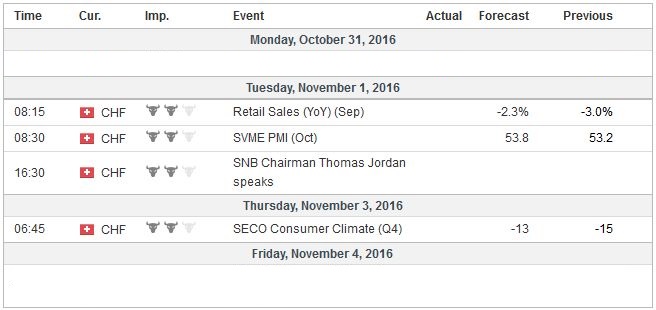

Switzerland |

Economic Events: Switzerland, Week October 31 . - Click to enlarge |

Tags: #USD,Bank of England,Bank of Japan,Federal Reserve,newslettersent,RBA