Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc(By George Dorgan) The EUR/CHF has arrived at the new floor level. We expect some SNB invervention here. It is also a good chance to buy some EUR longs. |

EUR/CHF - Euro Swiss Franc, October 20 2016(see more posts on EUR/CHF, ) . - Click to enlarge |

|

(By Matt Vasallo) GBP/CHF rates have fallen dramatically over the past month, as Sterling continues to find itself under pressure against the major currencies. However, despite these losses it is not all doom and gloom for those clients holding GBP, as Tuesday’s positive spike for the Pound proved. Currency does not move in a straight line and therefore we will see opportunities for those clients holding GBP to take advantage of, even if a sustainable Sterling recovery is unlikely in the short-term. As touched on Sterling received a welcome boost during Tuesday afternoon trading, following a host of inflation data, which came out above market expectation. Whilst this spike cooled during yesterday’s trading, the Pound was holding its position against the CHF following the latest UK employment data and official Unemployment rate. Whilst the official figure of 4.9% came in as expected, average earnings were up and this should help to support Sterling’s position ahead of some key economic data releases over the coming days. Today we have the latest European Central Bank (ECB) interest rate decision and subsequent monetary policy statement, which is likely to have a big impact on GBP exchange rates. This alongside UK Retail Sales figures are considered key economic releases by investors, so expect additional market volatility for Sterling as we head towards the end of the trading week. If you have an upcoming GBP or CHF currency requirement the current levels are a stark reminder as to how important it is to be kept up to speed with key market movements, ahead of any prospective currency exchange. The currency markets can move aggressively and without prior warning and this is where a proactive broker can help you time your trades and maximise your currency transfers. |

GBP/CHF - British Pound Swiss Franc, October 20 2016(see more posts on GBP/CHF, ) . - Click to enlarge |

FX RatesThe consolidation phase in the foreign exchange market continues. Narrow ranges prevail among the euro, sterling, and yen. The market seems to be in need of fresh incentives. The ECB meeting is next expected to yield fresh action, and the light US economic calendar facilities continued consolidation. |

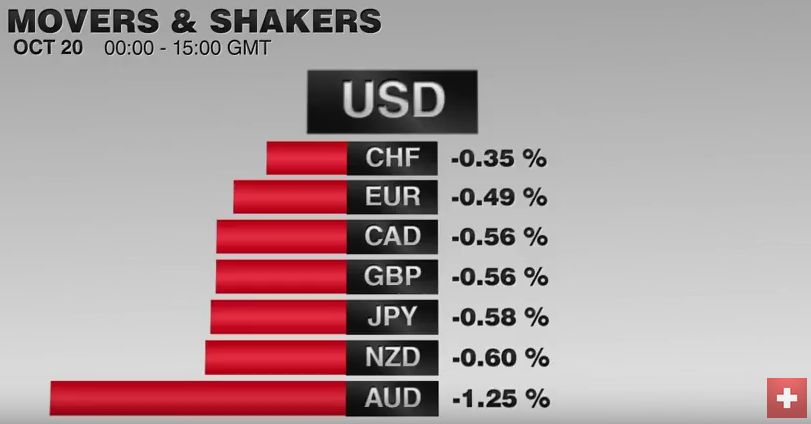

FX Performance, October 21 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Although it did not act, the admission cast a dovish spin to the central bank’s statement. The roughly balance risk assessment was an improvement to the downside bias previously, which had initially had driven the US dollar lower. Nearby resistance is seen in the CAD1.3200 – CAD1.3220 band. |

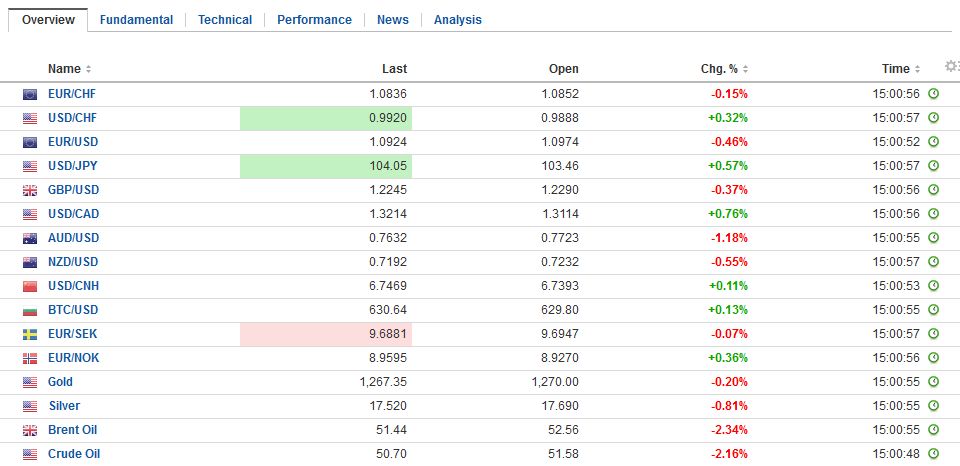

FX Daily Rates, October 20 (GMT 15:00) . - Click to enlarge |

| The $0.7700 is proving to be quite a formidable cap in the Australian dollar. It finished the North American session above there, spurring talk of a breakout. However, a disappointing jobs report has seen the Aussie reverse lower. This is potentially important price action. Initially, it had risen through yesterday’s high and had subsequently been sold through yesterday’s lows. A close below yesterday’s low (~$0.7660) could be regarded technically as a key reversal. A break of $0.7650 could spur an initially move toward $0.7600, and perhaps $0.7500.

|

FX Performance, October 20 . - Click to enlarge |

AustraliaThe Australian and Canadian dollars are the heaviest of the majors today. The US dollar continues to move higher against the Canadian dollar after yesterday’s upside reversal after testing CAD1.30, spurred by Bank of Canada Governor acknowledging that the central bank did discuss more stimulus. |

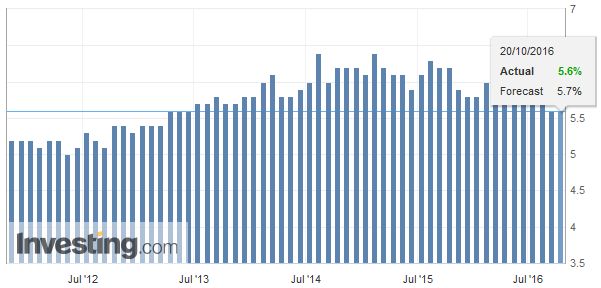

Australia Participation Rate, September 2016(see more posts on Australia Participation Rate, ) . Source: Investing.com - Click to enlarge |

| For the record, Australia lost 53.0k full-time positions and grew 43.2k part-time jobs. The unemployment rate, slipped to 5.6% from a revised 5.7%, while the participation rate unexpectedly fell to 64.5% from 64.7%. The net job loss of 9.8k contrasts with median expectations of a 15.0k gain. Adding insult to injury, the August job loss was revised to 8.6k from a 3.9k drop. |

Australia Unemployment Rate, September 2016(see more posts on Australia Unemployment Rate, ) . Source: Investing.com - Click to enlarge |

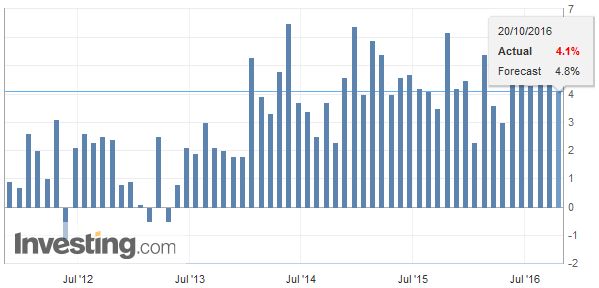

United KingdomUK retail sales disappointed, stagnating for a second month in September. The median had expected a 0.3% increase. The negativity may have been dampened somewhat by the upward revision to the August from -0.2% to 0. A combination of factors seems to be at work, including unseasonably warm weather and rising prices. For example, clothes and footwear sales were off 2.8%, which may have a seasonal component, while prices were up over 5%. Sterling has been unable to poke above $1.23 thus far today, for the first time since Monday. A $1.2220-$1.2320 range may be the most in sterling’s tank today. There is a risk of negative headlines coming from the EU heads of state summit that begins today. It is UK Prime Minister’s first summit. While Brexit may not be formally on the agenda, it will be among the 800-pound gorillas in the room (alongside national politics, which could produce new governments France, Germany, Netherlands, and possibly Italy). For many EU leaders, there can be no soft Brexit, if that means the UK retains access to the single market and limits EU migration. |

U.K. Retail Sales YoY, September 2016(see more posts on U.K. Retail Sales, ) . Source: Investing.com - Click to enlarge |

EurozoneThe ECB meeting is the main highlight, but with any firm decision about its asset purchase programs two months off, this may be nearly a non-event. At his press conference, Draghi may do little more than dangle a carrot in front of investors. He will likely reaffirm the inflation outlook is the key consideration, and the central bank has the tools, will and mandate to do more if necessary. The March 2017 end date of the purchases has always been rather soft, and this ECB’s flexibility likely will also be stressed. The euro continues to trade quietly, but with a heavier bias. It made a marginal new three-month low just above $1.0950 to match the July 25 low. Below there, the referendum low was closer to $1.0915. The euro is the largest component of the Dollar Index. As we noted in the weekly technical note, the 50- and 200-day moving, averages were poised to cross, and indeed today they have. Some technicians see what is dubbed the Golden Cross as a bullish signal. Ahead of the DBRS review of Portugal’s credit rating tomorrow, Portuguese bonds continue to rally and outperform other European bonds. The 10-year yield has fallen by more than 40 bp since peaking on October 10. It is now at its lowest yield since mid-September. The Finance Minister recently played down the risk of a change from the rating agency, and the minority left-of-center government delivered a 2017 budget proposal that maintained the fiscal consolidation which it had seemed to object. The coming clash, perhaps as early as next week, may be between the EC and Italy. The EC has given Italy a week to revise its budget proposal or face the start of a formal process to reject it. Renzi, who is fighting possibly for his political future over the constitutional referendum, may have little to lose by fight the EC. However, the issue seems minor. Renzi’s budget proposal projects a deficit of 2.3% next year from 2.4% this year, though it is higher than previously anticipated. |

Eurozone Current Account, September 2016(see more posts on Eurozone Current Account, ) . Source: Investing.com - Click to enlarge |

Germany |

Germany Producer Price Index (PPI) YoY, September 2016(see more posts on Germany Producer Price Index, ) . Source: Investing.com - Click to enlarge |

Switzerland |

Switzerland Trade Balance, September 2016(see more posts on Switzerland Trade Balance, ) . Source: Investing.com - Click to enlarge |

The earthquake and the migrant crisis may also be mitigating factors. Moreover, it may not be unreasonable to argue that rather than the bad loans holding back the economy, it could very well be that the weak economy is exacerbating the bad loan problem. The implication is that the emphasis may need to shift to a more pro-growth stance.

Lastly, we note that Brazil cut rates yesterday for the first time in four years. The Selic rate now stands at 14.0%. While this may be the start of an easing cycle, the central bank was clear what it needs to see: easing price pressures and a government that makes real progress in its fiscal reform. Political developments in Brazil can challenge this, however. Around the same time as the central bank was cutting rates, the former speaker of the House, who reportedly masterminded the impeachment, was himself arrested. If Cunha implicates ministers in Temer’s government, it could undermine support for fiscal reform.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$CAD,$EUR,Australia Participation Rate,Australia Unemployment Rate,Brazil,ECB,EUR/CHF,Eurozone Current Account,FX Daily,gbp-chf,Germany Producer Price Index,newslettersent,Switzerland Trade Balance,U.K. Retail Sales