Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

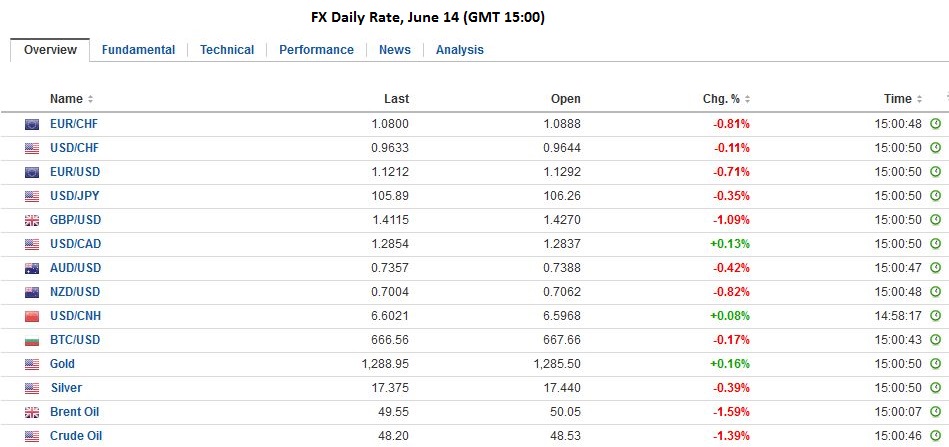

“The Swiss Franc was the strongest performer, EUR/CHF has fallen to 1.08 by 0.8%”.

A spate of opinion polls showing a tilt toward Brexit, and the leading UK newspaper urging the Leave vote on the front page, keep the global capital markets on edge. Equities are lower, though of note ahead of the MSCI decision first thing Wednesday in Asia, Chinese shares eked out a small gain. Core bond yields are 4-5 bp lower, which pushes the 10-year German bund yield into negative territory for the first time.

FX RatesSterling, which had rallied more than a cent in the US afternoon, gave it all back to return to yesterday’s lows. So far that low, near $1.4115 remains intact, but it seems premature to attach much significance to this. Separately, and largely inconsequential investors, the UK reported slightly softer than expected May CPI. The headline rose by 0.2%, keeping the year-over-year rate at 0.3% compared with a 0.4% median guesstimate. The core rate was unchanged at 1.2%. Producer prices warned of a squeeze on margins as input prices surged 2.6% or nearly three times more than the median, while output prices by a third of what the median expected or 0.1%. |

Click to enlarge. |

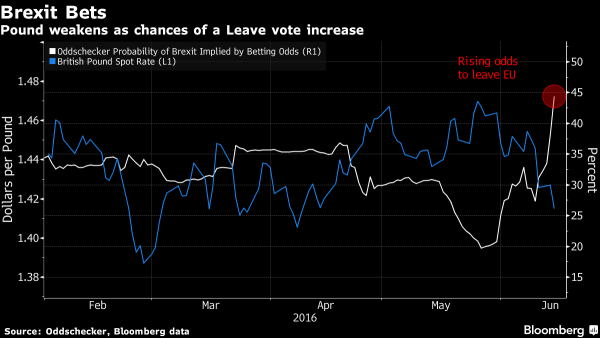

BrexitThe market response to the increasing recognition that Brexit is a real risk may not be so undesirable or causing the UK economy much harm. Sterling has fallen by nearly 4% on a trade-weighted basis since late-May. Given the large trade deficit and low inflation, sterling’s depreciation may be quietly celebrated in some circles. |

Pounds vs Brexit Odds, Source Zerohedge |

The UK 10-year yield has fallen by 22 bp in the past month. With the economy having slowed, this too is not problematic. The FTSE is off 1.3% today. This loss accounts for nearly half of the loss that has been recorded over the past month. Over this period, the FTSE is among the best performers in Europe and within the G7, it has trailed only the S&P 500 and the Toronto Stock Exchange.

Only yen among the major currencies has bested the US dollar since June 8. The yen has gained 1.2% against the greenback, which returned to within spitting distance of the May 3 low near JPY105.55. The New Zealand dollar has bested the other often sought safe haven, the Swiss franc. The Swiss franc has fallen 0.7% against the greenback over the past four sessions but has gained 0.8% against the euro during the same time. Speculators in the futures market were carrying their largest net short franc position of the year as of last week’s CFTC report.

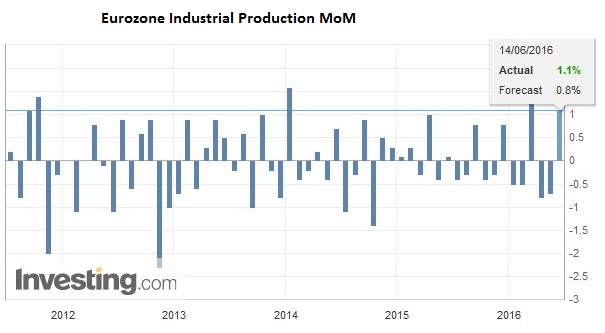

EurozoneThe euro is at its lowest level since the disappointing US employment report on June 3. At $1.1220 it retraced 61.8% of the rally since the May 30 low near $1.11. If the $1.1200 area is broken, there is little chart support until $1.1150. The eurozone slightly better than expected industrial output figures (1.1% instead of 0.8%)has no perceptible impact. The stronger Germany, French and Italian figures have suggested a robust report, and Brexit fears are overwhelming other considerations. |

Click to enlarge. |

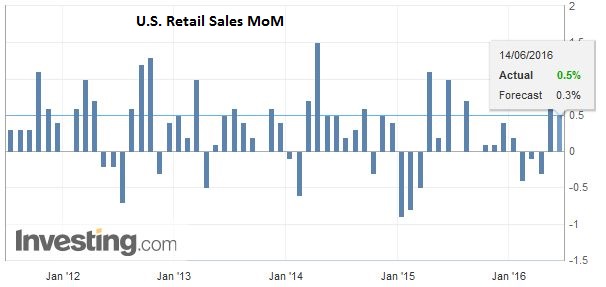

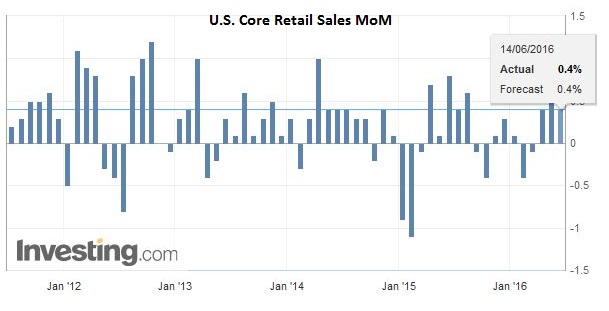

United StatesIn North America, the market will remain sensitive to new UK polls. Also, UK Labour leader Corbyn, who has shown little enthusiasm to oppose Brexit, is being called upon to step up his efforts and will be delivering a speech. The US reports import/export prices, but more importantly is the May retail sales report. |

Click to enlarge. |

| After the 1.3% jump in April, a softer report is expected. We suspect there is upside potential, though, from the median’s expectation for a 0.3% increase. Gasoline prices rose about 3%. Auto sales increased slightly on a sequential basis, and the warm weather may have helped the headline. |

Click to enlarge. |

| The components that feed into GDP are expected to have risen by 0.3% after the 0.9% surge in April. The quarter would be off to a good start. The two-month average would be a little more than 0.5%, which would be the best two-month period in two years. The retail sales report coupled with the April business inventories (due 90 minutes after the retail sales figures) may impact Q2 GDP forecasts. |

Click to enlarge. |

The market’s response may be asymmetrical. Disappointing consumption figures would likely undermine the odds of July hike by the Fed while a strong report would not boost the odds much, as the next back of jobs data is regarded as more significant.

Lastly, note that in early Hong Kong on Wednesday, MSCI will make its announcement about changes in its indices. The key issue for many is whether China’s A-shares are included in the emerging market index. It is a close call and on balanced, we lean against it. But even if we are wrong, we do not expect a large market reaction. Fund managers will have a year to implement and with the heavy tone (Chinese stocks are among the worst performing markets over the past year), suggests there is no need to be in a hurry. In addition, MSCI is expected to move slowly when it does move. The inclusion of 5% of the A-share capitalization, for example, would amount to about 1% of the emerging market index. Estimates suggest around $1.7 trillion tracks MSCI emerging market equity index.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: Brexit,Eurozone Industrial Production,FX Daily,Japanese yen,newslettersent,U.S. Retail Sales