Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

A couple of weeks ago, the four central banks that meet in the coming days were thought to be a big deal. Numerous Federal Reserve officials were preparing the market for a summer hike. Risks of a new downturn in Japan spurred speculation that BOJ would ease policy.

A couple of weeks ago, the four central banks that meet in the coming days were thought to be a big deal. Numerous Federal Reserve officials were preparing the market for a summer hike. Risks of a new downturn in Japan spurred speculation that BOJ would ease policy.

On the other hand, the neither the Bank of England nor the Swiss National Bank were expected to move ahead of the UK referendum on June 23. Besides providing extra liquidity to the banks in the ahead of the vote, the BOE was understood as being in a reactive posture as was the SNB.

A June hike by the Federal Reserve seemed like a stretch to us. The risks posed by the possibility of a Brexit vote, we thought, forced the FOMC to wait six week for its next meeting, even if the May jobs data was not so poor. A move in July, when a press conference is not pre-scheduled, would have the added advantage of securing more degrees of freedom for the Fed, which is clearly reluctant to hold a press conference after every meeting like the ECB and BOJ. Until proven otherwise, the Fed moves appear limited to the quarterly meetings which include updated forecasts and are followed by a press conference.

The May employment data pushed expectations away from this week’s meeting. Yellen’s speech on June 6 sketched out the Chair’s views and confidence that the overall thrust of the economy is positive. Does this mean that the FOMC meeting is a non-event?

There are two issues that may determine the market’s response to the FOMC meeting. First, to what extent does the Fed keep the July meeting live? We expect the FOMC statement and Yellen’s press conference to indicate that the Fed could raise rates in July. The Federal Reserve is unlikely to be as dovish as some might expect given the disappointing 38k increase May’ s nonfarm payrolls, the 59k downward revision of job March and April, and the fall in the participation rate that reversed this year’s gains.

Second, to what extent does the Fed’s Summary of Economic Projection (dot plot) continue to see the appropriateness of two rate hikes this year? We expect the median dot to continue to be consistent with two hikes this year. Where the may be some tempering is in next year’s projection of four hikes. The market impact may not be particularly significant. The implied yield of the December 2017 Fed funds futures contract is 67.5 bp. Most recently the average effective Fed funds rate, which is what the contract settles at, 37 bp. That is to say that this market is fully pricing one hike between now and the end of next year and no more than a 20% chance of another hike.

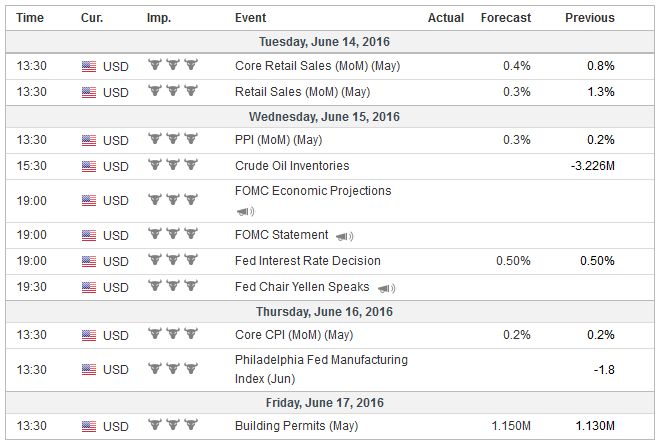

United StatesThe US reports economic data almost every day next week. Although the PPI and CPI reports straddle the FOMC meeting, we suggest that the most important information will come from retail sales. The only way the disappointing jobs data could be a prelude to a recession as some are suggesting, is if it were to undermine household consumption. Retail sales account for about 40% of consumption, which itself accounts for about 70% of GDP. Headline retail sales are expected to build on April’s 1.3% increase by rising another 0.3%.It would be the first back-to-back gain this year. It would put the two-month average at 0.8%, which is the highest since April 2014. The component that feeds into GDP is expected to be up 0.3%, which would match the 12-month average, after rising 0.9% in April. The retail sales data coupled with April business inventories will likely spur revisions to Q2 GDP estimates. The Atlanta Fed’s model has it tracking 2.5%. |

Important Economic Events

|

The industrial sector has been a drag on the economy in recent quarters. The three, six, and 12-month averages peaked between April and July 2014. They have all bottomed out and turned higher. However, following the strong April bounce, some payback is anticipated. Industrial output is expected to slowed by 0.2% after rising 0.7% in April. Similarly, manufacturing production rose 0.2% in April and is expected to have slipped 0.1%. The Fed and investors will see these reports before the FOMC decision on June 15.

None of the four central banks that meet this week are expected to do anything, but the BOJ would be the most likely to surprise. The BOJ’s meeting concludes the day after the Fed’s. A Fed rate hike could reduce some demand for yen while a signal that the Fed is less confident about the economy than before and the yen could strengthen.

Last week, the US dollar recovery coincided with the rally in bonds. Foreign demand for US debt appears to be increasing as more Japanese and European yields move deeper into negative territory. Japanese, German, and UK yields fell to new record lows. That foreigner investors or investors who would have invested in JGBs or core European bonds are drawn to the positive returns available in the US is not surprising.

JapanWhat is surprising is that foreign investors continue to buy Japanese bonds. The weekly MOF data shows that barring March when foreigners sold Japanese bonds in three of the four weeks; foreign investors have been consistent buyers since the middle of January. The most recent data covered the week ending June 3. Foreign investors bought JPY611 bln of Japanese bonds, which is the most since mid-April. We see three reasons why even with negative yields some foreign investors could be attracted to Japanese bonds. First, many asset managers cannot take naked currency positions. The return on Japanese debt instrument will be driven by the exchange rate. Second, given the deflation Japan continues experience and weak growth, some investors may conclude that the BOJ ease policy further, which will drive down rates. They may be willing to accept aminus26 bp yield on a five-year JGB if they thought the rates would fall to -40 bp, for example. |

Important Economic Events

|

Third, there may be some financial arbitrage opportunities, like using cross currency swaps to move from dollars to yen to invest in a JGB. Sometimes, given a particular set of market conditions, a lucrative return can be secured.

The BOJ has surprised the market under Kuroda’s leadership. It is at least in part a communication issue, but whatever the cause, investors must be attentive. The case for easing is there if perhaps the BOJ was not so deep already in the rabbit hole of a rapidly growing central bank balance sheet and negative interest rates.

There is reason to be patient, including that Q1 GDP surprised investors to the upside and was subsequently revised higher. The proximity of the early-July upper house election may give cover as well for a stand-pat policy. The focus is squarely on fiscal policy with Abe’s formal decision to postpone next year’s sales tax increase. A larger fiscal package is expected to be unveiled shortly.

The fact that central bank’s do not apply the negative deposit rates to all deposits creates a new tool that can be used. The rules can be tweaked. This seems like a potential option for the BOJ, where the negative rate currently applies to only a small part of deposits. The SNB could explore this, as well.

Some observers who saw in the recent reported increase in Swiss reserves as a sign of intervention must be surprised by the recent price action. Last week the Swiss franc strengthened the most against the euro since the cap was lifted in January 2015. The franc’s 2.1% rise is more than twice as large as any other weekly increase this year. The franc rose every day last week against the euro and has risen in 12 of the last 15 sessions.

There are three strategies that could account for such price action. First, participants can be simply buying francs and selling euros. Second, participants could be selling the euro and ignoring the franc. Third, participants could be selling the euro more than they are selling the franc.

Of course, it is not wholly one thing or another. Most narratives emphasize the first strategy. The adjustment of speculative positioning in the futures market suggests the third strategy. Speculators trimmed gross long positions and increased gross short positions by a little more than a third. Speculators have the largest short franc position in four months.

Euro zoneBefore the Bank of England meets on Thursday, the latest prints on prices, consumption, and labor markets will be available. The strength of the April industrial production and manufacturing output, contrary to the PMI, warns against exaggerating the weakness of the economy to prove a point in the debate over the EU. Carney may wax on at the Mansion House Dinner about some financial matter, but Osborne will not miss the opportunity to paint the risks of Brexit. |

Important Economic Events

|

Indeed, Brexit trumps all other issues in the UK. The polls still seem to be pointing to a tight race, while the events and gambling markets have seen the gap narrow, they consistently point to a wider victory for the remaining in the EU than the polls. At the start of the new week, investors will be keen to learn of the impact of the violence at the Eurocup in France on the voting intentions.

The by-election in Tooting South England on June 16 may scrutinized for clues about the referendum outcome. However, there are other forces at work in the district that was previously represented by the Khan, the new Mayor of London. Khan had carried the seat last year with 47% of the vote. However, the Tories improved from 2010 and garnered 42% of the vote. It is also the first by-election since Corbyn become head of the Labour Party. In his mayoral campaign, Khan distanced himself from Corbyn.

In the middle of the week ahead MSCI is expected to formally announce its decision whether to include China’s mainland A-shares into its global emerging market indices, against which an estimated $1.7 trillion of investments are tracked. Many Chinese shares that trade in Hong Kong (H-shares) and in the US (ADRs) are already included.

ChinaChinese officials are eager for the A-shares to be included for two reasons. First, capital inflows would help offset the capital outflows that China is experiencing, and would help broaden the investor base. Second, it is yet another badge of honor like being included in the SDR. It is recognition of the significance of China. China A-share market accounts for 1/10 of global market capitalization. |

Important Economic Events

|

However, China’s stock market is dominated by retail investors. Is it really ready for global institutional investors? A year ago MSCI said no. Chinese regulators have been rushing through numerous reforms to facilitate a yes answer this year. It is a close call, and we lean against it. There is no harm in waiting another year, especially after last summer’s experience. On the other hand, a premature decision could cost the MSCI credibility. The limit on capital repatriation to 20% a month remains and this alone makes many skeptical.

There has been much anticipation of the MSCI decision. Activity in the options on the some ETFs for China’s large cap index increased markedly last week, for example. Yet, the immediate impact of any decision is likely to be minimal. A decision not to include the A-shares yet would leave the status quo.

Fund managers would have a year to adjust to a decision to include the A-shares. This would be a gradual process. At first, about 5% of the A-share market cap is anticipated to be included. This would give the A-share weighting about 1% in the MSCI Emerging market equity index. Still many asset managers will face an information challenge as this would still mean the inclusion of some 400 companies, whose reports and other data are primarily in Mandarin.

Eventually, China may account for as much as 40% of the emerging market equity index. Half may be accounted for by the offshore market (H-shares and ADRs) and half by the A-shares. This is process may take several years to complete, and it is set to begin slowly regardless of this week’s decision.

Full story here Are you the author?

Tags: Bank of England,Bank of Japan,China,Federal Reserve,newslettersent,Swiss National Bank,U.S. Nonfarm Payrolls,U.S. Participation Rate