Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

| The US dollar is little changed against the major currencies as yesterday’s moves are consolidated and traders wait for fresh developments. Global equities were higher after Wall Street’s advance yesterday. Asia-Pacific bond yields were firm, following the US lead, but European 10-year benchmark yields are lower, led by the continued rally in Greek bonds after an agreement was struck that will free up a tranche of aid. |

Source Dukascopy |

| The relative stable capital markets are itself news. Last summer and again earlier this year, weakness of Chinese yuan and equities were a major disruptive force. Earlier today the PBOC “fixed” the yuan at its lowest level since March 2011. The dollar has been trending higher against the yuan steadily even if slowly all month. Today it is at three-month highs. |

Source Investing.com |

Chinese equities were the only Asian market to weaken today. The MSCI Asia-Pacific Index advanced 1.5% today off seven-week lows seen earlier in the week. The HK China Enterprise Index was up 2.7%. China’s markets were off 0.25%, and year-to-date are off 20%-22%

Yesterday the Wall Street Journal thought it was news that China is not letting market forces drive the yuan. We have long discussed the gap between China’s declaratory policy and its operational policy. Today Bloomberg report that the Chinese delegation to the upcoming Strategic and Economic Dialogue talks (June 6-7) is keenly interested in whether the Fed hikes in June or July.

The report claims China would prefer July. Can it really make that much of a difference? Is this a topic for a strategic discussion? Even though the Federal Reserve may practice a type of democratic centralism that is familiar in China, can Yellen (Fed chair often attends the talks) commit one way or the other, and even if she could, would she (or the US) want to?

Moody’s downgraded Germany’s largest bank to start the week, and now the CEO of Italy’s largest bank has stepped down, clearing the way apparently for a capital campaign. The Dow Jones Stoxx 600 is up 0.8% as the financials continue to outperform (+1.4%). The news stream in Europe has been mostly limited to the German May IFO, which was better than expected, and the Italian industrial sales and orders were weak.

The EU-IMF/Greece deal is more of the same. Over the weekend, the Greek parliament approved numerous measures that tightened fiscal policy. It also adopted a contingency plan if it had not met its fiscal targets in 2018. The EU agreed to free up 10.3 bln euros so that Greece can service its debt, chiefly in official hands.

There has been tension between the EU and IMF over the sustainability of Greece debt. The IMF had called for “unconditional” relief. Germany appeared the most adamant: No. This seemed to be both a principled position as well as a political consideration ahead of next year’s election. The IMF capitulated. Rather than debt relief upfront, the IMF has agreed to give its blessings to debt relief after the completion of the current program in 2018.

There had been reports that the many of the non-European members of the IMF had been critical of the multilateral lender’s exposure to Greece. The major concession made today does not address that criticism. However, a new battle likely will be fought as later this year the IMF will conduct a new debt sustainability analysis and assess before committing new funds.

There are three highlights of the North American session today. First, the US advance merchandise trade report for April (expected to widen to $60 bln from $56.9 bln) will be plugged into Q2 GDP models.

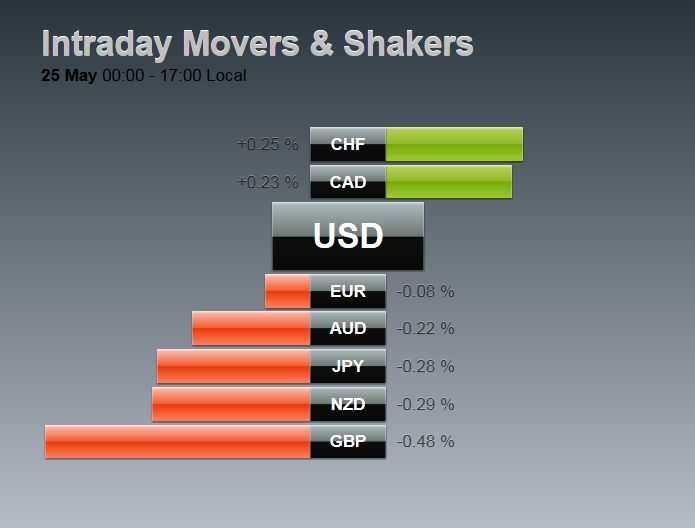

Second, the Bank of Canada will announce the decision of its monetary policy meeting. There will be no change in rates, but the accompanying statement will be quickly scrutinized for bias. The economy appears to have lost some momentum, and the Alberta fires won’t help. At the same time, the apparent recovery in the US after a six-month soft patch is welcome news for Canada. The recovery in oil prices is also a favorable development for Canada. Also, since the last meeting, the Canadian dollar’s four-month 14% rally ended, and it has pulled back almost 5% this month.

The third development is the oil market itself, or more to the point, the inventory data. Late yesterday, API estimated that oil inventories fell 5.1 mln barrels last week. This helped lift prices to seven-month highs. The EIA’s estimate is regarded as more reliable. The median was expecting a 1.6 mln barrel draw down before the EIA’s estimate. A larger liquidation of inventories could see the price above $50 a barrel for the first time since last October.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Bank of Canada,China,FX Daily,Greece,newslettersent