Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

|

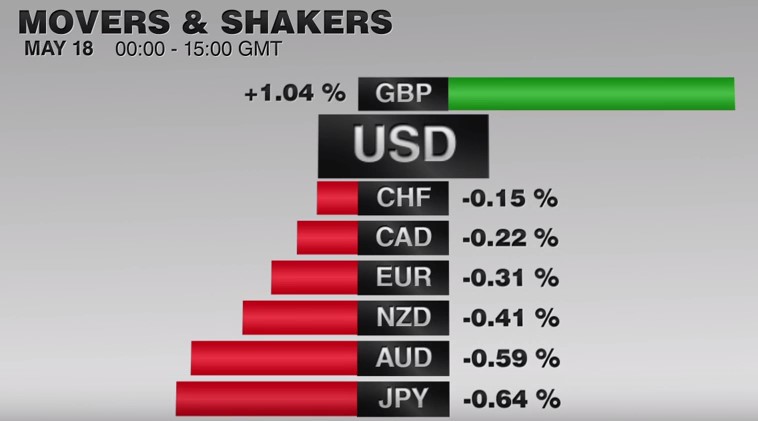

Apart from GBP, the US dollar is rising against all the major currencies today. The Australian dollar is retracing a sufficient part of its recent gains to suggest that the current phase of the US dollar’s recovery is not over. Given that the Aussie topped out a week before the other major currencies, it is reasonable that it begins recovering first. Its recent resilience was noted, but that has evaporated today, but a 0.8% drop by early European activity.

We had noted the divergence between what appeared to a constructive technical condition and interest rate markets that were largely unchanged. The recent price action is providing more interest rate support for the dollar. Specifically, consider the Fed funds futures strip. The August contract can be used to calculate the odds of a June or July rate hike. The implied yield has risen three bp this week. It may not sound like much, but its is the difference between almost 25% and 36% chance.

|

|

Bonds

The December contract is also interesting. The yield has risen six basis points this week. The implied yield now stands at 58 bp. If the Fed did not raise interest rates until December 14, fair value for the December contract is about 51 bp. The market has moved to discount one 25 bp move and about a third of the another move.

Look at what is happening to the US-German two-year interest rate differential. Despite that strong US retail sales report and consumer confidence on May 13, the US premium over Germany on two-year money rose a single basis point. However, this week it is already up 10 bp to reach the upper end of the range that has prevailed since late-March.

The euro has been pushed through last week’s lows and appears set to test important support in the $1.1200-$1.1220 area. That area corresponds to last month’s lows and a 38.2% retracement of the euro’s rally since the early-December upside reversal during the Draghi’s press conference. It probably requires a break of $1.12 to convince more participants that a high is in place.

Japan GDP

|

Japan reported stronger than expected Q1 GDP figures earlier today. The Bloomberg median was 0.1%, but instead, Japan reported a 0.4% expansion. This offset in full revised 0.4% decline in Q4 15, (from -0.3%). Consumer and government spending drove growth while business spending fell 1.4%. Consumer spending rose 0.5%, more than twice the pace the market expected (0.2%).

While GDP was flat in Q4 15-Q1 16 period, consumption fell. The rise in consumption in Q1 16 followed a revised 0.8% contraction in Q4 (from -0.9%). Consumption in Japan accounts for around 60% of GDP. It has fallen on average 0.2% a quarter of the past four quarters. It has risen 0.2% on average over the past 20 quarters (five years).

Business spending fell 1.4% in Q1, almost twice the pace expected, and the Q1 revision was not friendly (1.2% from 1.5%). During the past four quarters, business spending has fallen 0.3% on average. Over the past five years (20 quarters) is has averaged 0.5%. Our hypothesis is that the low level of business spending is due to the lack of capital, high-interest rates, or a heavy effective tax burden. If that is true, it means that lowering interest rates and cutting taxes are unlikely to business spending.

|

|

The policy outlook is unlikely to be changed by the GDP figures. The Abe government in still thought to be working on a fiscal package, which may include the postponement of the retail sales tax increase. While the details are expected to leak out, Abe expected to unveil it formally at the G7 summit at the end of the month that he hosts. Many continue to expect the BOJ to also expand its monetary stimulus. It may include buying more ETFs, and two new issues that meet its requirements are expected to come to market soon.

The US dollar has proven resilient against the yen despite the better than expected GDP report. It briefly dipped to almost JPY108.70 from above JPY109 but rebounded to begin the European trading at its session high near JPY109.55. The move above JPY109.50 resistance yesterday ran out of steam near JPY109.65. The market may be reluctant to take the dollar much through this area without fresh developments. The JPY110 area offers important psychological resistance that dollar will unlikely go through on the first approach.

As we have seen, rate interest rate differential shift is supporting the pullback in the euro against the dollar. However, the US premium over Japan for 10-year money is still not fat enough to draw strong interest. At 187 bp it has risen about seven basis point this week, but it is still off a few bps since the end of April.

The dollar’s gains against the yen does not mean that equity markets are stronger. In fact, Asian markets, including the Nikkei fell after the S&P 500 lost one percent yesterday, and the MSCI Asia-Pacific surrendered about three-quarters of yesterday’s gains. European shares opened around 0.3% lower, with nearly all sectors lower. It presently looks as if the S&P 500 will open just above yesterday’s lows (2040). Our technical analysis identified this as the upper end a band of support that extends to 2030. A break brings our technical of 1990-2000 into view.

The calendar is light for the US today. The main feature is the FOMC minutes from the April meeting. The minutes pick-up a range of views. The FOMC statement is one view, as nuanced as it may be. Given the discussions in March, with some regional presidents suggesting the possibility of an April hike (and Yellen at the NY Economic Club saying no), the minutes are likely to be more hawkish than the statement. This also seems obvious from recent comments from a few Fed presidents.

There was one dissent, Kansas Fed’s George. We suspect, but cannot prove, that there is an agreement about dissents. George’s dissent may represent others’ views. One need be Tyler Durden to appreciate that the Fed’s public persona is finely crafted, with much thought and consideration.

We continue believe that investors are best advised to hear what the regional president say, but listen to the leadership of Yellen, Fischer, and Dudley. Not to put too fine of a point on it, but a clearer sense of the Fed’s thinking will be likely found in Fischer and Dudley’s speeches tomorrow than the minutes today.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Bank of Japan,Janet Yellen,Japanese yen,newslettersent,SPY,U.S. Retail Sales