Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Investors have become unhinged. The increased volatility and dramatic market moves challenge even the most robust investment strategies. This sets off a chain reaction of money and risk management that further amplifies the price action, like an echo chamber. Then a cottage industry of reporters, analysts and bloggers offer explanations often without distinguishing the initial sound from the echo.

At the same time, that which we have come to think of as terra firma has turned into quicksand. Interest rates are bounded by zero. Of course, there had been a few exceptions, like when Germany and Switzerland in the 1970s discouraged speculative foreign inflows, but it was not a generalized phenomenon. Now it is widespread. German and Japanese yields are negative out eight to nine years while Switzerland has negative rates through 15 years. All told more than $8 trillion of debt has a negative yield.

Negative yields in Europe and Japan complement the expansion the central banks’ balance sheets. Such extremely accommodative monetary policy is associated with depreciating currencies. Yet, the yen has surged, and the euro has rallied against the greenback, despite the dollar being backed by higher interest rates.

In 2008, when oil prices were near $150 a barrel, and peak oil was the rage, the concern was that it was a major headwind on growth. Oil prices have plunged since mid-2014. They have fallen below $30 a barrel, but now this has been associated with weaker economic activity. Capital expenditures have slumped. Industrial output has fallen. Even Japan, which imports nearly all of its energy (slowly a few nuclear plants have re-opened) has not benefited.

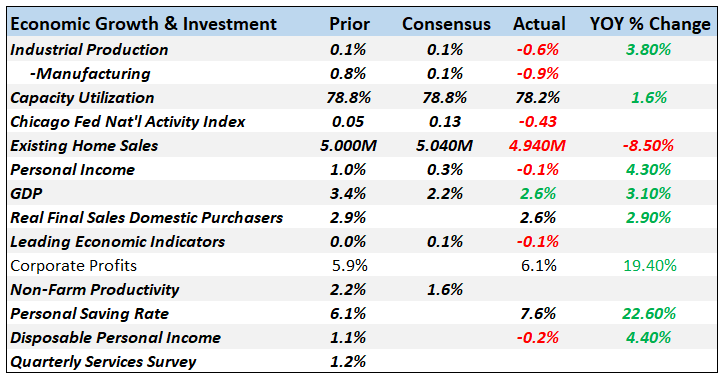

In fact, Japan Q4 15 GDP will be released in the week ahead, and it will likely confirm that the economy is still struggling to find any positive traction. The world’s third-largest economy contracted in Q2 15 while the contraction that was initially reported for Q3 was revised away. However, weakness in consumption and residential investment likely more than offset the stronger foreign demand, pointing to a contraction of around 0.2% in Q4.

Nearly a year after the Federal Reserve wound down its asset purchase program, it raised interest rates. However, the world’s largest economy nearly stagnated in Q4 15, and neither the decline in oil and gasoline prices nor still low interest rates and a very accommodative Federal Reserve have deterred recession talk.

The pendulum of market psychology has swung too far. China is not seeking a large devaluation, and to the contrary is spending billions of dollar resisting pressure, some of which is clearly coming

from speculators and hedge funds that take to the airwaves talking their position. A similar attempt to sell the bonds of the largest debtor in the world, Japan, failed miserably as the 10-year yield briefly fell below zero last week.

The decline in oil prices is, in fact, good for consumers. US consumption rose 3.1% last year, the most in a decade. American consumers also bought a record number of autos and light trucks. Even if the recovering labor market and low interest rates helped, so did the drop in oil and gasoline prices. European growth, which seemed to approach what many economists consider trend growth (1.0%-1.25%) was boosted more by domestic demand than exports.

The pessimists have confused Wall Street with Main Street. It is true that the sharp drop in equities, rising risk premiums, and the tightening of lending conditions can undermine the real economy. It is too early to reach that conclusion. There have been many dramatic losses in the equity markets that did not drag the economy down.

Indeed after nearly stagnating in Q4 15, the US economy is reaccelerating in Q1 16. Despite the market turmoil, more people are working for slightly better pay, and longer hours in January, and they went shopping. Core retail sales (excluding autos, gasoline, and building materials) rose 0.6% in January.

The poor Q4 15 growth in the US cannot be laid at the Fed’s feet, as it did not raise rates until the quarter was nearly over. In her testimony before Congress, Yellen showed no remorse for the Fed’s unanimous decision to hike rates last December. The Atlanta Fed’s GDPNow tracker projects Q1 16 GDP to be near 2.7%. The Fed’s 25 bp hike did not derail the US economy.

In the week ahead, the US is expected to report housing starts rose in January after falling in December. Industrial output likely snapped a four-month slide, with the consensus call for a 0.4% rise. Manufacturing output is expected to post its first increase since October.

What of inflation? The unorthodox monetary policies in Japan, Sweden, and the eurozone is more about achieving the central banks’ inflation targets rather than growth per se. The US and UK report CPI figures in the week ahead. In the US, core CPI trended higher last year, despite the dollar’s appreciation and the drop in oil prices. In January, the core rate is expected to be unchanged at 2.1%.

UK headline CPI appears to have bottomed last year slightly in negative territory (-0.1%). It finished last year at 0.2% and is expected to have ticked up to 0.3% in January in part due to a favorable base effect. The core rate may have slipped to 1.3% from 1.4%. Airfare and apparel prices may be the culprit. Past sterling strength may also be feeding through. Separately, the UK’s labor market report will likely show a continued easing of wage pressures.

The pendulum of market psychology has swung toward pricing in a modest chance of a rate cut by the Bank of England. The March short-sterling futures contract implies a yield of 60 bp. However, all the contracts through March 2017 are implying lower yields, with the September 2016 contract indicating a 20% chance of a cut.

Some may be seeking protection in case of Brexit rather than “betting” on a rate cut. Supply and demand may be the more important driver than expectations. Nevertheless, further tightening in the labor market (the ILO measure of unemployment is expected to slip to 5.0% from 5.1%) and a healthy retail sales report may help sentiment recover. January UK retail sales, excluding auto fuel, are expected to have risen by 0.7% after the 0.9% fall in December.

The US, UK, Japan, and Germany have near full employment, by the respective central banks’ reckoning. Yet the upward pressure on wages is marginal at best. This remains another economic anomaly. To be sure, economists have offered various reasons, including that wages did not fall as much as “they should have” during the crisis, and hence, the rebound is less than what “it should be”. Other economists suggest that the labor market may have greater slack than is being reported.

The decision by a large UK-headquartered bank to abandon its plan of less than two weeks to freeze pay this year is instructive. The decision to freeze wages was not a comment about average or marginal productivity. Nor was the decision to reverse itself driven by productivity or inflation considerations. It is about power. The disparity of income (and wealth) reflects asymmetries of power.

Employers are reluctant to pay more for an input cost (labor) than they are compelled to. In Japan, where corporations are reporting record profits and have cash-rich balance sheets, wages rose 0.1% year-over-year in December 2015. Despite the moral suasion by government officials and central banks, the division of present (as well as past) productivity gains between profits and wages favors the former and will until forced otherwise, but that does not appear to be on the near-term agenda.

The Federal Reserve releases the minutes of last month’s meeting in the middle of the week. That the Fed left rates on hold was not surprising after the December hike. The market will be looking for some insight into how worried the Fed is by the market turbulence. The FOMC statement said officials were still trying to determine if their growth outlook or risk assessment needed to be changed.

Some observers saw this as a sign that the Fed was so bewildered that it did not offer a risk assessment. We read the FOMC statement differently. Since the Fed did not change its assessment, the previous one, articulated when it hiked rates in December was still operative. Yellen’s testimony seemed to lend credibility to our reading. The FOMC minutes may shed more light.

The record of the ECB’s January meeting will be published the next day. The issue here is the extent that the risks sketched out by Draghi in December, when a modest rate cut and extending of the asset purchase program was announced to the disappointment of many, have materialized. The market is anticipating, at least, a 20 bp rate cut next month and, perhaps, the introduction of a tiered deposit rate scheme, like many other central banks, including the Bank of Japan and the Swiss National Bank.

However, the ECB’s record, which has not been much of a market-mover in its brief history, may be overshadowed by the EC Summit of the heads of state. The Netherlands holds the rotating presidency, and two issues dominate the agenda: negotiations of the measures to avoid a UK exit, and the refugee/immigration challenge. Both issues are thorny, and there is risk that neither issue sees closure.

If there is no resolution, it puts more pressure on the March Summit. Indeed next month is shaping up to be critical. The ECB will most likely ease. The BOJ may ease. While the Federal Reserve won't hike rates, it will revise its forecasts (dot plots) but is unlikely to abandon all the rate hike projections as the market has done.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.K. Retail Sales,U.S. Housing Starts