Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

1. China's Central Economic Work Conference is responsible for setting the annual GDP target. Although it was not formally announced, President Xi previously indicated that the goal for the economy to expand by around 6.5% a year through 2020. More telling than the GDP target is the intentions expressed in the new slogan: flexible monetary policy, forceful fiscal policy. For Chinese officials, these are not ends in themselves but means to another end. In this case, the goal is to facilitate structural reforms. A more flexible monetary policy does not only refer to the yuan's link to the dollar, but also in adjusting the price of money to supply and demand. This is an ongoing process adopting a reference corridor for rates.

Chinese shares have gradually crept higher. On Tuesday, the Shenzhen Composite reached its highest level since mid-July. The 50-day moving average is about to cross above the 200-day average, which is sometimes referred to as the Golden Cross. The Shenzhen Composite closed at 2379. The next major hurdle is seen near 2485. The Shanghai Composite has lagged and is near last month's highs. While the Shenzhen is above its 200-day moving average, the Shanghai Composite is still a little more than 5% below its 200-day moving average. It closed near 3652. The 3740 area corresponds with a 38.2% retracement of the summer drop.

2. US Q3 GDP was revised to 2.0% from 2.1%, which was a little better than expected. The main source of the downward revision came from a smaller accumulation of inventories. There were two highlights. First, personal consumption expenditures was revised to 3.0% from 2.9%. This is roughly two-thirds of the US economy. This is solid, and being achieved with little new debt. It is being fueled by job creation, small increase in pay, and arguably helped by the lower energy prices.

Second, the core PCE deflator was revised to 1.4% from 1.3%. It has no bearing on November's monthly report due out tomorrow. The core PCE deflator is expected to be unchanged at 1.3%. The focus, however, may be on the consumption itself, It has disappointed, rising only 0.1 in both September and October. A 0.3% increase in November would go a long way toward dismissing the earlier reports as anomalous (if they are not revised).

Durable goods orders rose 2.9% in October, and a small pullback is expected in November. Although Boeing orders increased, reports indicate a concentration in the relatively lower cost aircraft. This may also weigh on headline optics. Shipments of core capital goods will likely rebound, and this will support forecasts for Q4 GDP of around 2%.

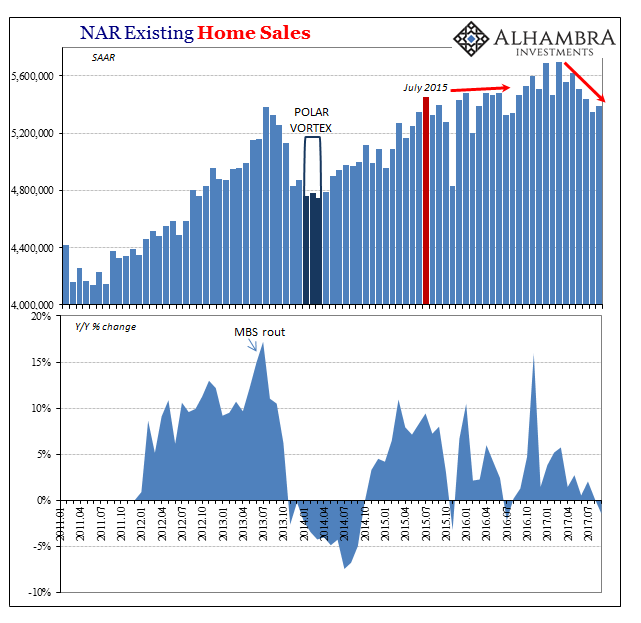

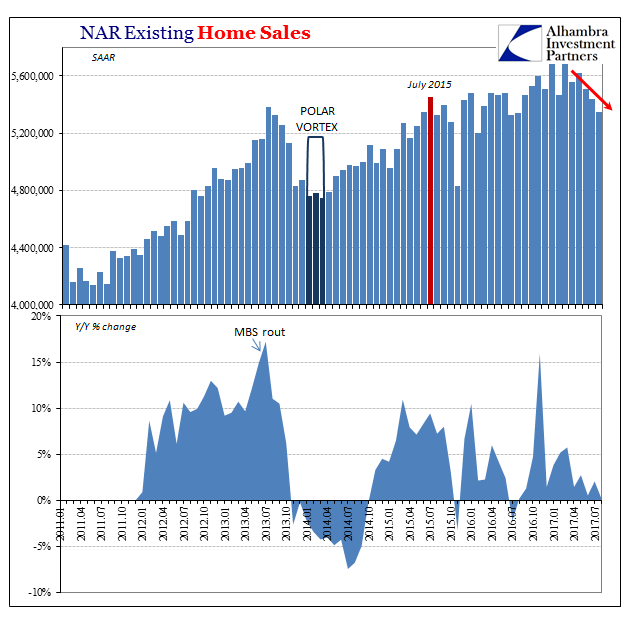

While existing home sales reported on Tuesday were disappointing (-10.5% in November compared with the Bloomberg consensus of a 0.2% decline), there are some mitigating factors, including new procedures. It was still the drop brings existing home sales to their lowest level (seasonally-adjusted annual rate) since April 2014. New home sales are expected to have fared better. The have stabilized since falling earlier this year. They are expected to have risen by 2.0% after a 10.7% increase in October.

3. Spanish asset markets stabilized though the political uncertainty remains heightened. It is, as always, difficult to separate the impact of thinner volumes from investor signals. Some sort of grand coalition is the obvious solution, but not very Spanish. Instead, a minority government seems preferred, but cannot be very stable. And a coalition government, where the traditional political elites come together to fend off an attacks, feeds into the hands of the populists that argue there is not significant difference between the two main parties. There seems to be an attempt to see if the fate of the Lib Dems in the UK or the Free Democrats in Germany (to lesser extent) holds a lesson for Podemos or Ciudadanos.

The outcome of both Portugal's recent election and now Spain's cannot be seen in favorable light in Berlin. Even if it held the economic, moral high ground, which under the precepts of ordo-liberalism, it did, it is suffering a political backlash. At home Merkel's standing in the polls took a hit as the immigration issue become the dominant story and has not recovered. There have been numerous articles in the press discussing a post-Merkel Germany. This said Merkel's ascent is part a story of an astute politician, but it is also a story of adversary underestimating her.

One of the consequences is that she is going to have to take an even tougher line within EMU to protect the German purse, such as staunch opposition to a cross-border deposit insurance scheme. It could help lead to a confrontation with Greece in Q1 16 over controversial pension reform. It has taken some time to emerge, but a bloc in opposition to what we once half-humorously referred to as FANG (Finland, Austria, Netherlands, and Germany). Italy's Prime Minister Renzi has been emboldened by an improving domestic economy, and sufficiently stung by criticism over its handling of the flood of refugee to have struck back.

Renzi's ultimate criticism is that the rules of engagement of too often for the benefit of Germany. The criticism of Germany's largest current account surplus in violation of EU rules has become nearly standard fare since both the IMF, EU and US Treasury have cited it. More telling was in recognition that while the EU resisted a southern Russian pipeline that would have gone through Italy, it permitted a northern pipeline directly to Germany.

The point is the years of economic misery are being laid at the feet of the political elite. This is producing political changes. The forces broadly labeled anti-austerity appear to be on the rise in Europe. Given the immigration challenge and the terrorist attack in Paris, the fight will not be over the 2016 budgets but the following year, which makes it a H2 16 issue.

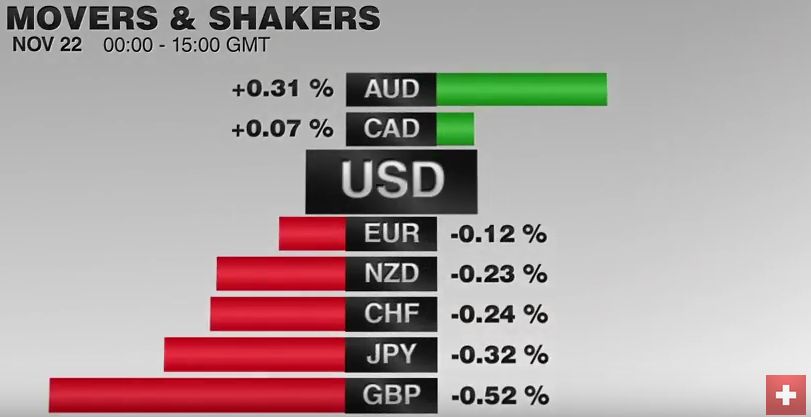

4. The pressure remained on sterling. It approached support at $1.48. It has fallen nearly 4.5 cents since December 14. Partly this unwinding of long sterling short euro cross positions. Since mid-November, the euro has rallied 6.3% against sterling in a large shakeout. This partly reflects the recognition that the BOE is not in a hurry to raise rates. UK wage growth, a critical argument for raising rates, has eased for a few months.

Many investors were surprised by the first budget of the majority Tory government, with limited spending cuts. Some suggested its was a budget that would bolster Osborne's candidacy as Cameron's successor. On Tuesday, the latest government report underscores what many have long suspected, the government is likely to overshoot its deficit target. Specifically, in the two-thirds through the fiscal year and the nearly GBP67 bln shortfall is GBP2 bln shy of the entire year's target. In the last fiscal year, the deficit of the final four months was almost GBP16 bln.

A move now above $1.4865 might help stabilize the technical tone for sterling. A convincing break of $1.4800, on the other hand, signs a test on the $1.4565 low from earlier this year. The key level for the euro is near GBP0.7500. It stopped the euro's advance in both May and October.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Existing Home Sales