Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

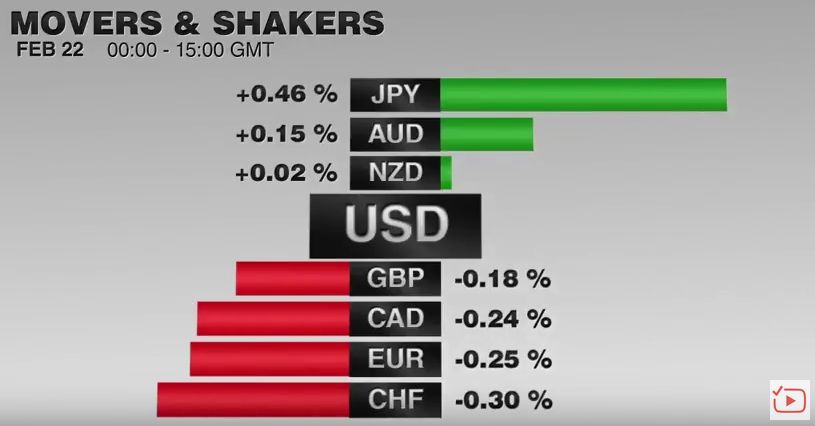

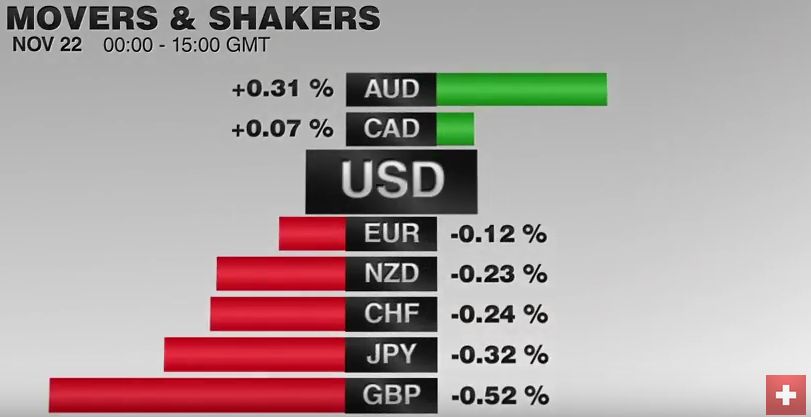

The foreign exchange market is becalmed, leaving the US dollar narrowly mixed in uneventful and light turnover. The euro has been confined to less than a third of a cent range. Yesterday it briefly dipped below its 20-day moving average for the first time since the ECB met earlier this month. It remains in the upper half of the two-range ($1.08-$1.10) that has confined prices most of this month. There was only one close outside of this range (December 9) since that ECB meeting.

The dollar is little changed against the yen. It remains in the narrow range established Monday between about JPY120.15 and JPY120.65. Sterling briefly slipped below $1.48 yesterday to record its lowest level since April. It is trapped in its trough today. The dollar-bloc is slightly softer, perhaps the retreat in oil prices spurred some profit-taking after yesterday’s advance.

Equities are a little lower today though Asian markets were mixed and both Japan and China registered minor gains. The MSCI Emerging Market equity index is off by about 0.5% as is the Dow Jones Stoxx 600 in Europe. The US S&P 500 are tracking a lower opening as well.

Sovereign bond markets are mixed. Core European bond yields are firmer while the periphery is lower. The US 10-year yield reached almost 2.32% yesterday, though has pulled back below 2.30% today. Of note, the US 10-year premium to Japan widened yesterday to 204 bp, which is the widest this year. The two-year spreads we have been tracking closely (vs. Germany, UK, and Canada) are all 1-2 bp narrower today.

API showed an unexpected 2.9 mln barrel build in US oil stocks. EIA estimates later today were expected to show a 1.76 mln drawdown. The February light sweet contract is trading about $1 a barrel lower than where it finished last week, which puts it near $37. Separately, reports indicate that Kuwait will budget for $30 a barrel and Iran expects $35-$55. The Russian ruble, among the most sensitive currencies to oil prices, is moving lower again. It is at new lows. Note that Russia enjoys a week-long holiday at the start of the New Year.

Reuters reports that at least two foreign banks have been suspended for three months from settling offshore clients CNY trades. This appears to be part of an effort to reduce the speculation that may be spurring the divergence between the onshore (CNY) and offshore yuan (CNH). That spread has widened to more than 1%, the widest since early-September. It is seen reflecting speculation of more yuan depreciation. Separately, a senior Chinese official caution Taiwan not to question the 1992 agreement that recognizes the principle of one China. Taiwan holds its presidential election in the middle of next month.

The ECB reported M3 money supply growth slowed to 5.1% in November from 5.3% in October. More importantly, lending to the private sector continued to improve. Lending to household rose to 1.4% from 1.2%. A year ago (November 2014) lending to households was still contracting (-0.4%). Lending to non-financial corporations rose to 0.8% from 0.6%. Lending to such businesses was still contracting as recently as June.

Sweden's Riksbank Governor Ingves warned that the krone's strength threatens the progress on inflation and that the central bank was prepared to intervene if necessary. This stopped the krone's momentum after it had risen to its best level against the euro since April.

Nationwide estimates that UK house prices rose 0.8% in December, the largest monthly increase since April. It lifts the year-over-year pace to 4.5% from 3.7%. Yesterday S&P/Case-Shiller estimated US house prices in 20-major urban centers rose 5.17% year-over-year in October.

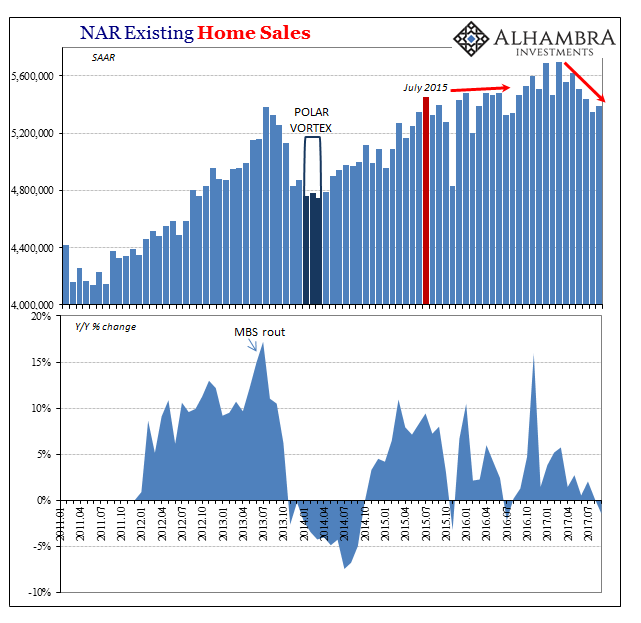

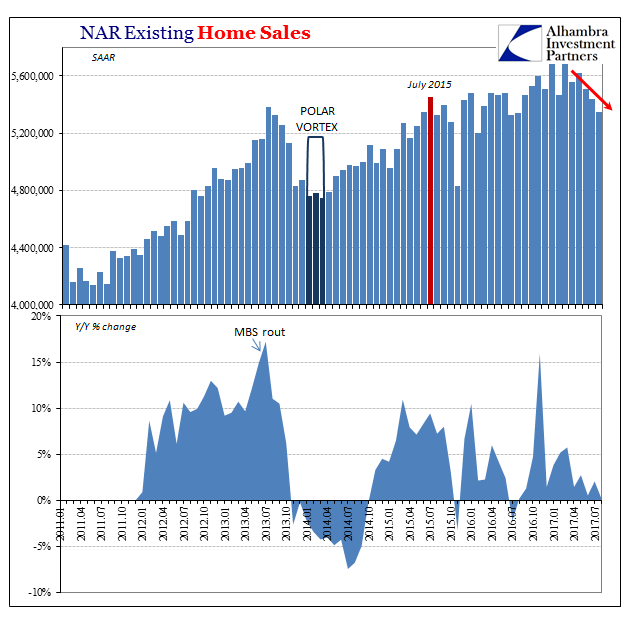

Besides the EIA energy report, the US reports November pending home sales. After rising earlier this year, a soft patch was hit near mid-year. Through September, pending home sales fell three times in four months. October saw a small increase (0.2%) and pending home sales are expected to have increased by 0.7% in November. This would be the first back-to-back monthly increases since April-May and bodes well for existing home sales in the first part of next year.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Existing Home Sales