Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Goldilocks And The Three Central Banks

Goldilocks And The Three Central Banks7 Apr 2022

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed16 Mar 2022

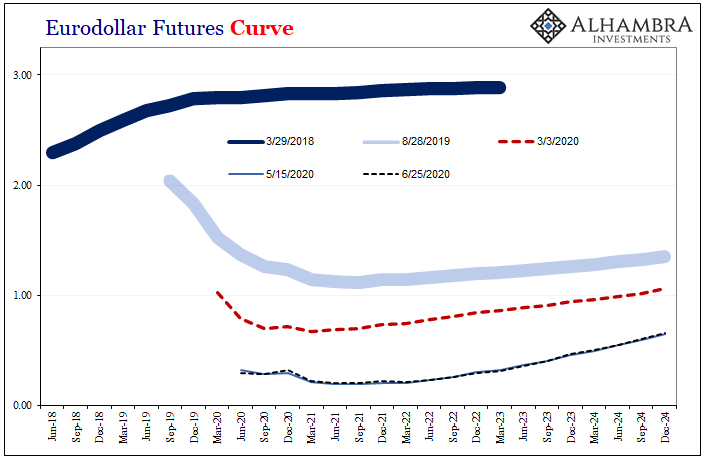

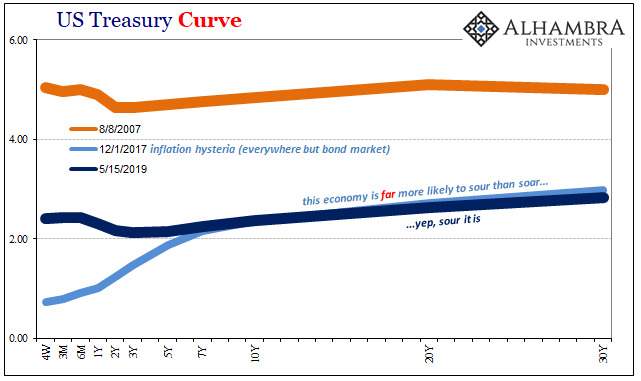

Wait A Minute, What’s This Inversion?28 Jun 2020

The Greenspan Moon Cult5 Mar 2020

A Day For Rate Cuts4 Mar 2020

Economy: Curved Again27 Feb 2020

Don’t Forget (Business) Credit5 Feb 2020

History Shows You Should Infer Nothing From Powell’s Pause2 Feb 2020

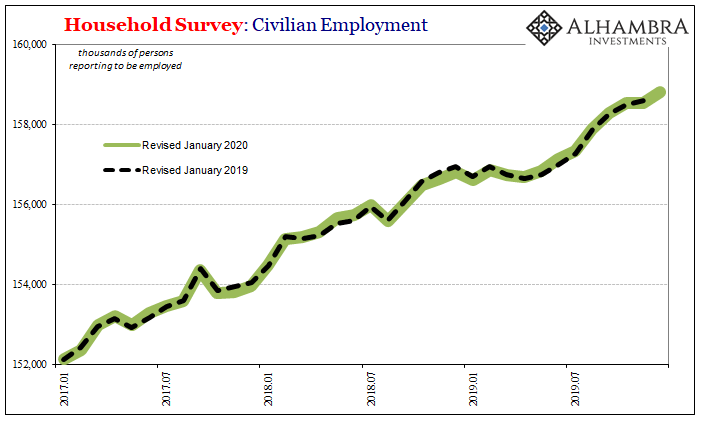

Very Rough Shape, And That’s With The Payroll Data We Have Now15 Jan 2020

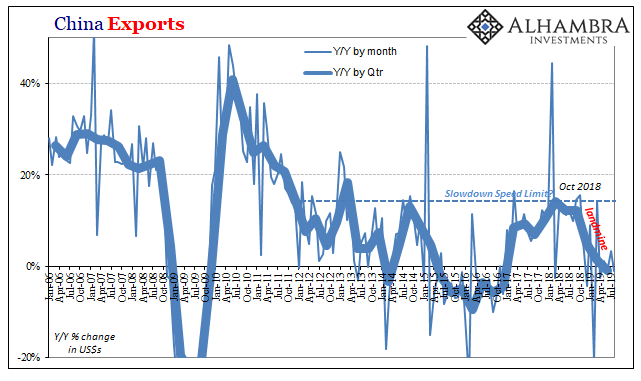

The FOMC Channels China’s Xi As To Japan Going Global13 Dec 2019

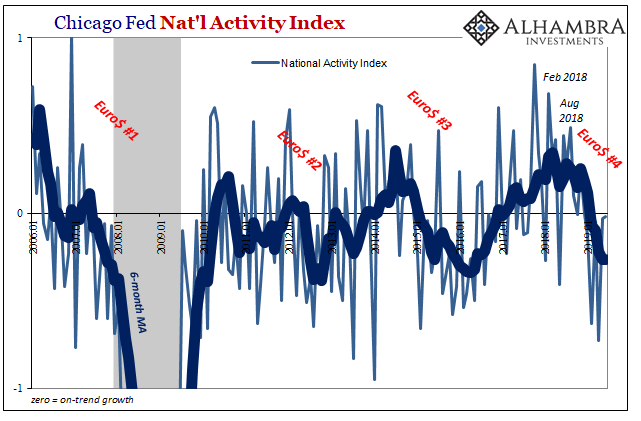

More (Badly Needed) Curve Comparisons23 Nov 2019

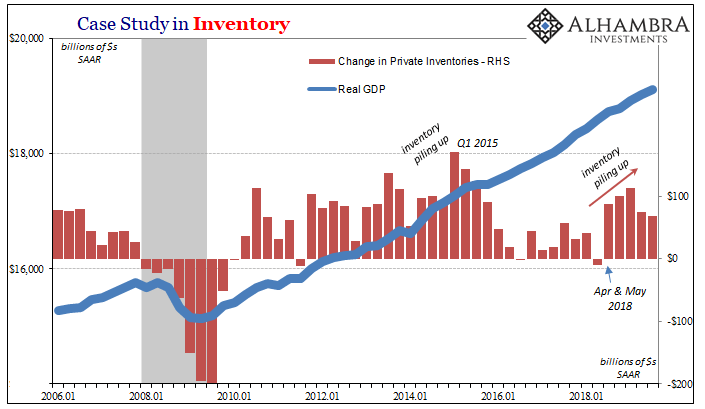

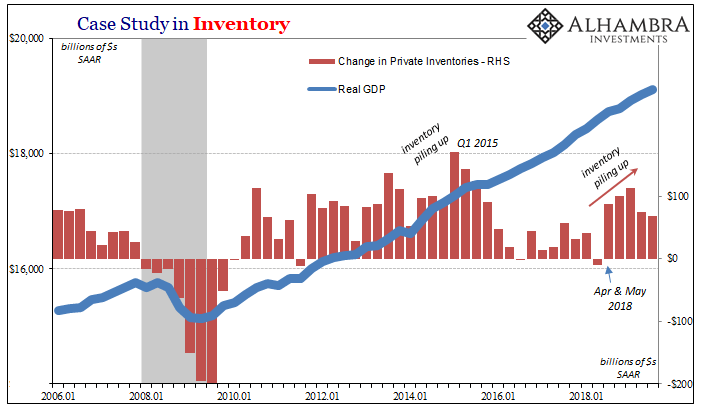

The Inventory Context For Rate Cuts and Their Real Nature/Purpose2 Nov 2019

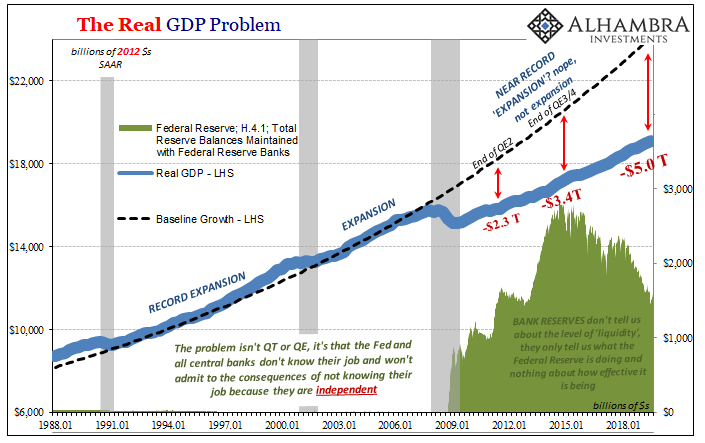

Three (Rate Cuts) And GDP, Where (How) Does It End?1 Nov 2019

The Inventory Context For Rate Cuts And Their Real Nature/Purpose1 Nov 2019

Macro Housing: Bargains and Discounts Appear24 Oct 2019

From JOLTS Series Shift To Series of Rate Cuts10 Oct 2019

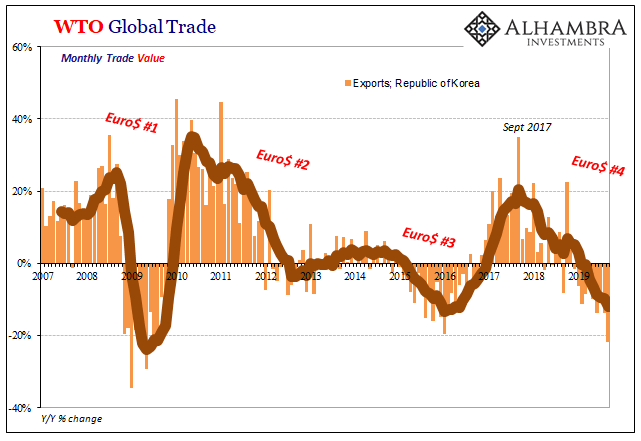

Waiting on the Calvary26 Sep 2019

Is The Negativity Overdone?10 Sep 2019

The Path Clear For More Rate Cuts, If You Like That Sort of Thing15 Aug 2019

US Economic Crosscurrents Reach the 50 Mark27 Jul 2019