Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

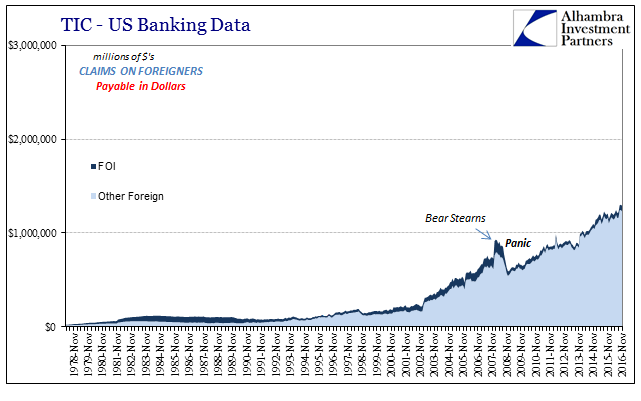

Do Record Eurodollar Balances Matter? Not Even Slightly

Do Record Eurodollar Balances Matter? Not Even Slightly7 Mar 2017

Effective Fed Funds and Money Markets

Effective Fed Funds and Money Markets21 Jul 2016

Great Graphic: Aussie Approaches Two-Month Uptrend

Great Graphic: Aussie Approaches Two-Month Uptrend20 Jul 2016

FX Daily, July 04: Four Things that Happened on the Anniversary of the Original Brexit

FX Daily, July 04: Four Things that Happened on the Anniversary of the Original Brexit4 Jul 2016

Kuroda and the BOJ15 Jun 2016

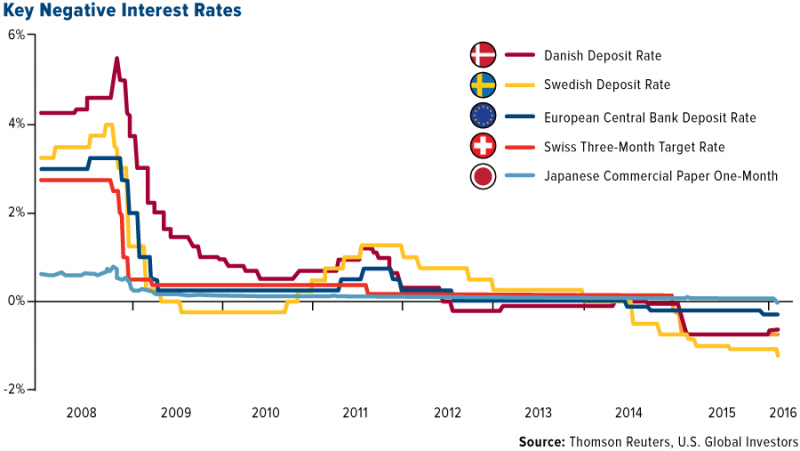

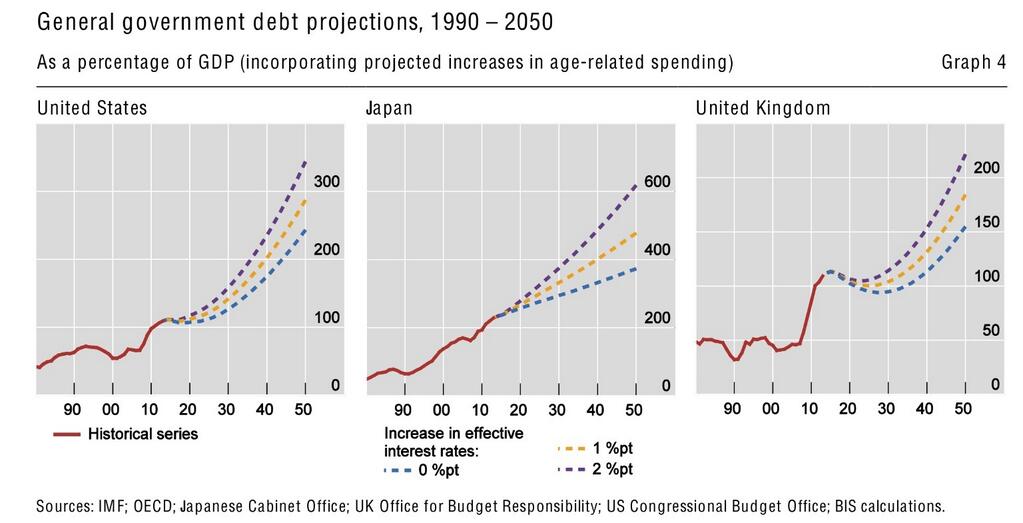

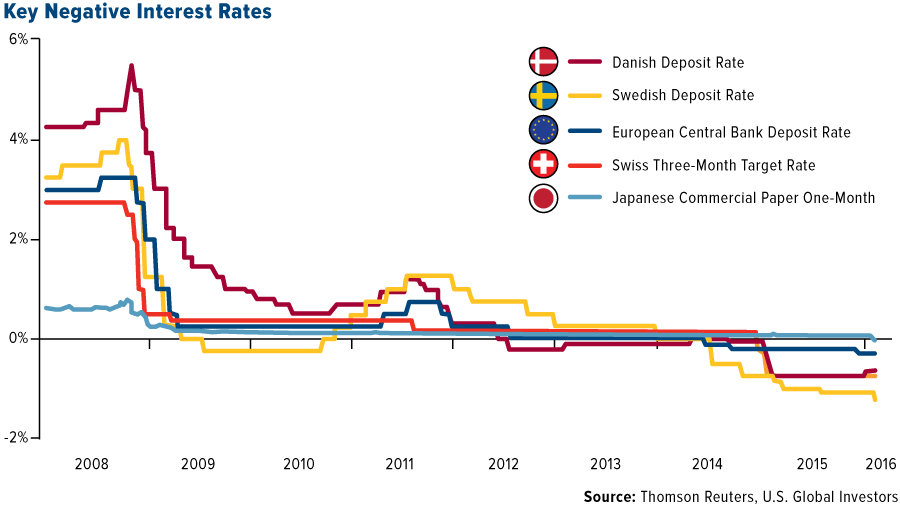

The Path to the Final Crisis and Negative Rates

The Path to the Final Crisis and Negative Rates1 Apr 2016

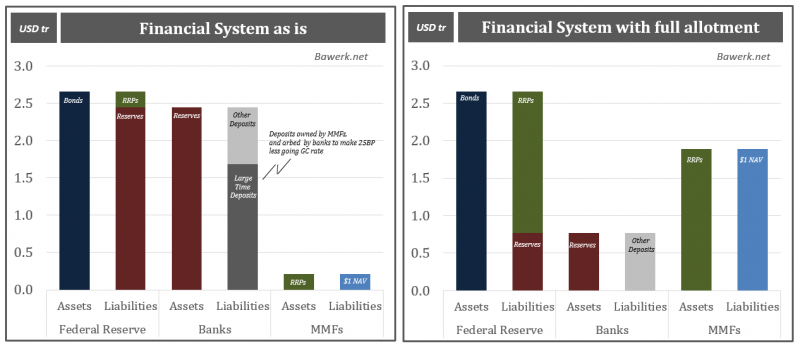

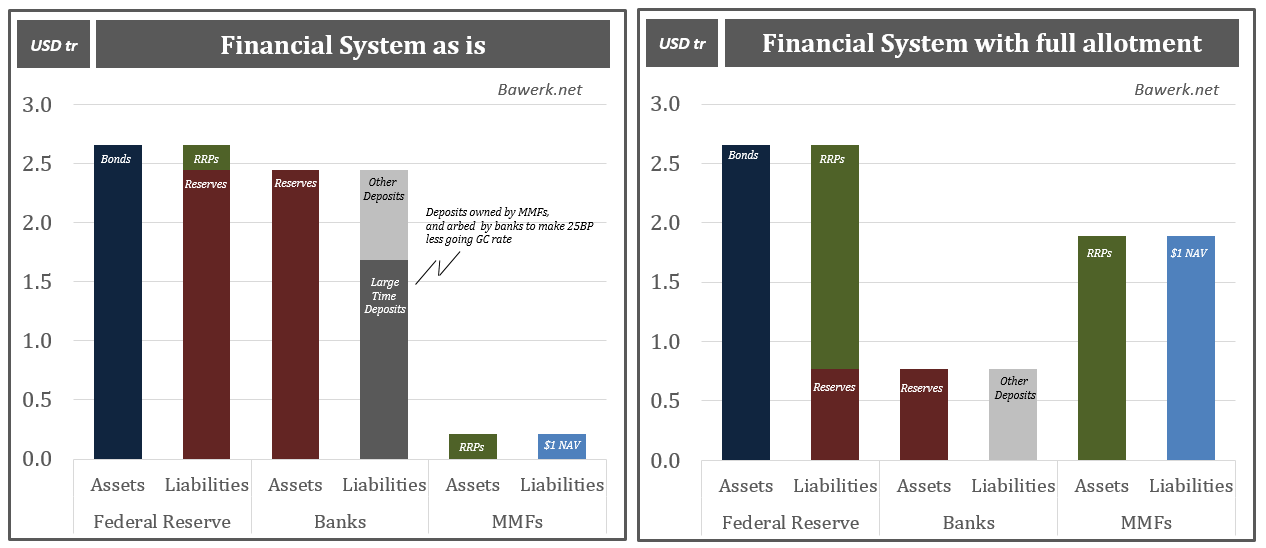

Unintended consequences of lift-off in a world of excess reserves

Unintended consequences of lift-off in a world of excess reserves28 Nov 2015

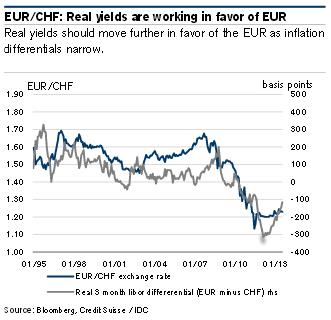

SNB Follows ECB? Pictet’s Negative SNB Interest Call3 Jun 2014

8 Nov 2013

Currency Positioning and Technical Outlook August 12: Corrective Pressures Dominate12 Aug 2013

Can The SNB Make Profit On Currency Reserves ?

Can The SNB Make Profit On Currency Reserves ?19 Sep 2012