Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk20 Jun 2022

It’s Not Nothing, It’s Everything (including crypto)

It’s Not Nothing, It’s Everything (including crypto)15 Jun 2022

Prices As Curative Punishment

Prices As Curative Punishment14 Jun 2022

Peak Policy Error

Peak Policy Error1 Jun 2022

‘Unconscionably Excessive’ Denial

‘Unconscionably Excessive’ Denial30 May 2022

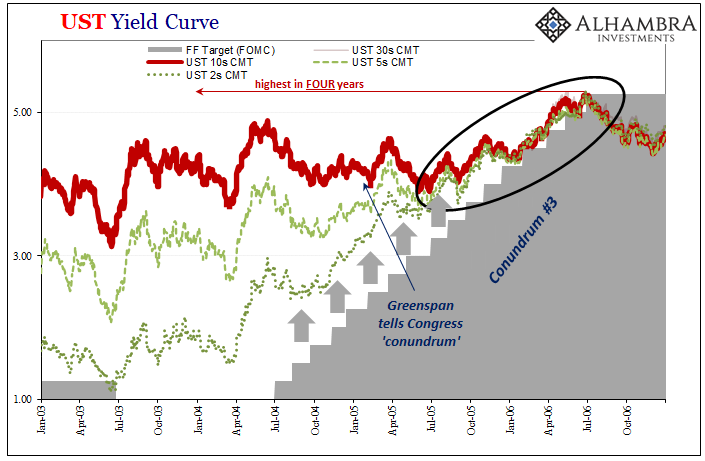

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

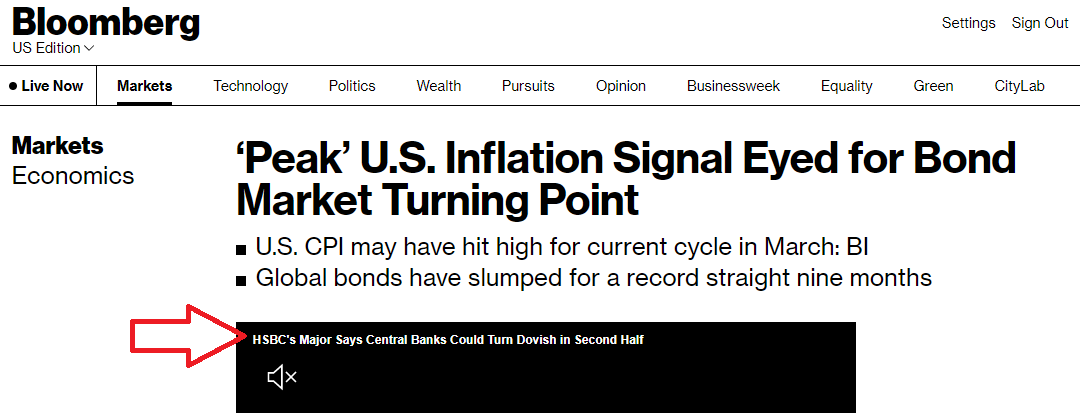

Peak Inflation (not what you think)

Peak Inflation (not what you think)15 May 2022

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets9 May 2022

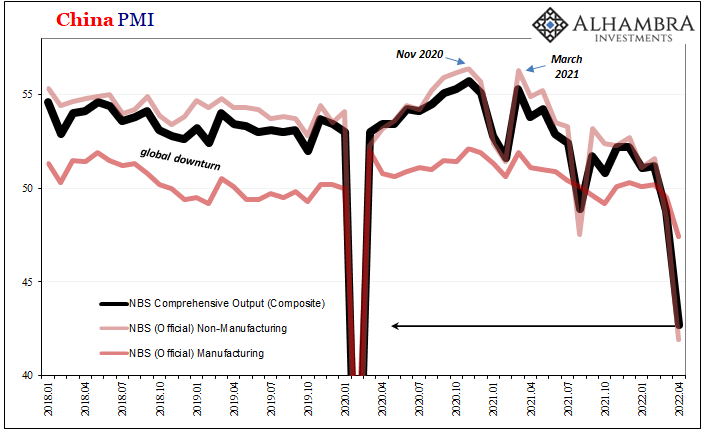

China Then Europe Then…

China Then Europe Then…8 May 2022

Media Attention All Over FOMC, Market Attention Totally Elsewhere

Media Attention All Over FOMC, Market Attention Totally Elsewhere19 Mar 2022

Another One Inverts, The Retching Cat Reaches Treasuries

Another One Inverts, The Retching Cat Reaches Treasuries15 Mar 2022

Consumer Prices And The Historical Pain(s)

Consumer Prices And The Historical Pain(s)12 Mar 2022

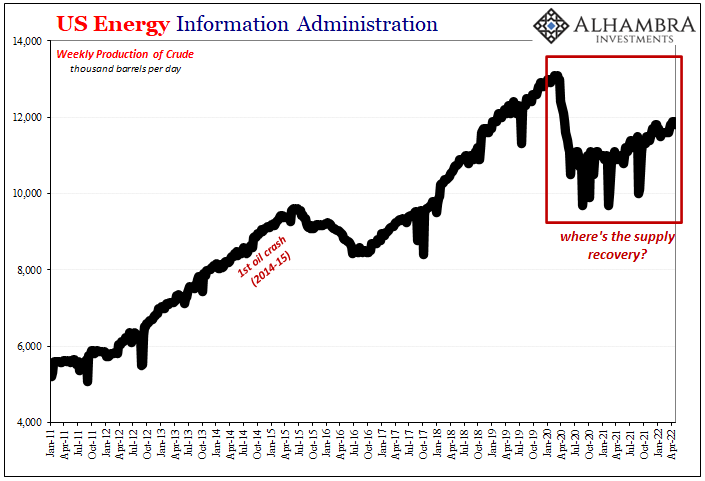

Houston, We Have An Oil (and inventory) Problem

Houston, We Have An Oil (and inventory) Problem7 Mar 2022

For The Fed, None Of These Details Will Matter

For The Fed, None Of These Details Will Matter6 Mar 2022

The Red Warning

The Red Warning24 Feb 2022

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**28 Jan 2022

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There26 Jan 2022

Taper Discretion Means Not Loving Payrolls Anymore

Taper Discretion Means Not Loving Payrolls Anymore10 Jan 2022

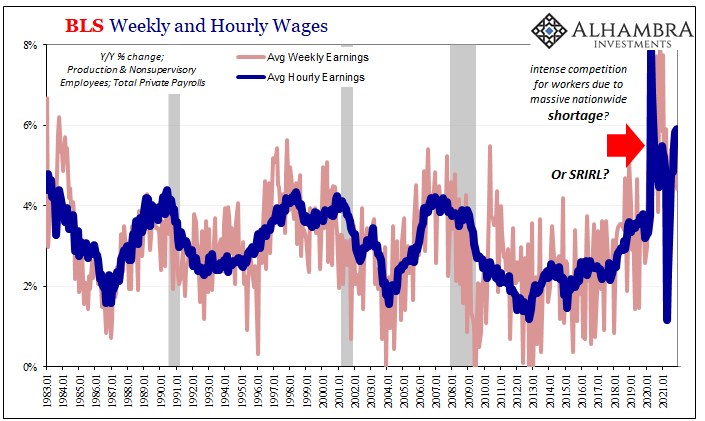

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?5 Jan 2022

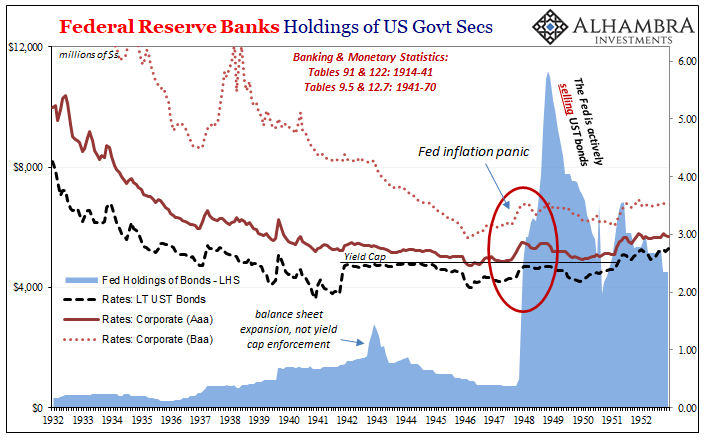

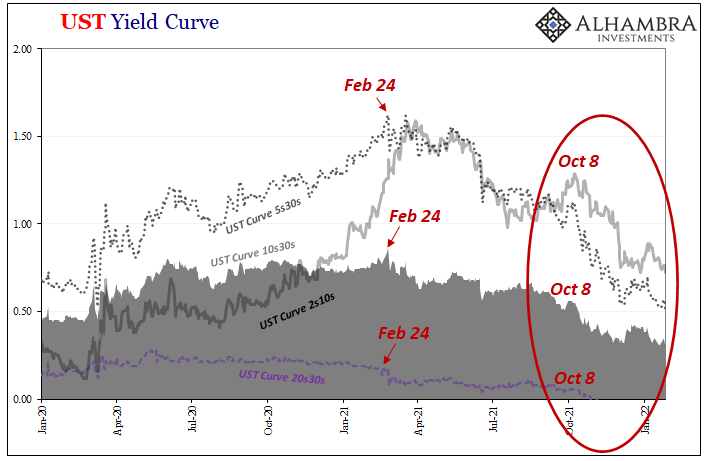

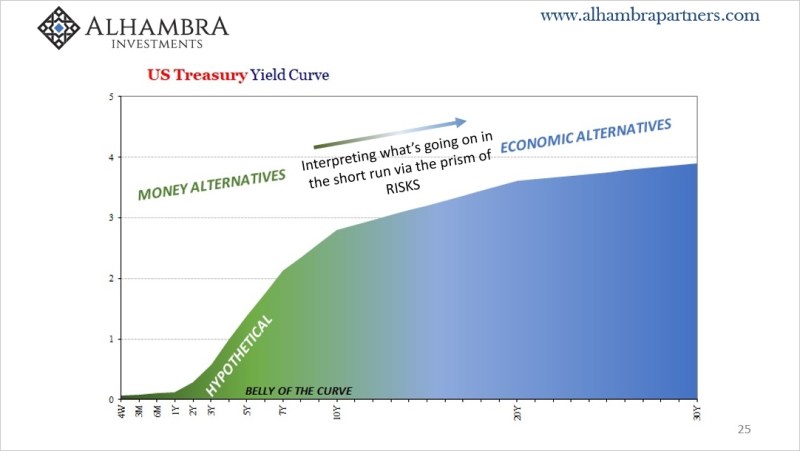

The Curve Is Missing Something Big

The Curve Is Missing Something Big21 Oct 2021