Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

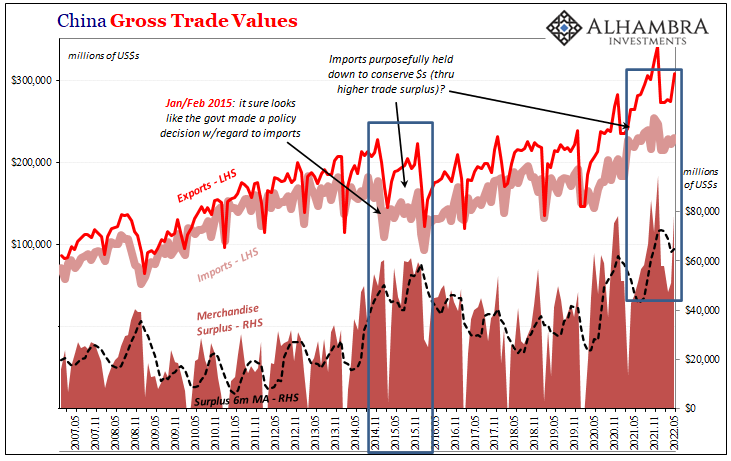

Wait A Sec, That’s Not Really An *RMB* Liquidity Pool…

Wait A Sec, That’s Not Really An *RMB* Liquidity Pool…1 Jul 2022

Peak Policy Error

Peak Policy Error1 Jun 2022

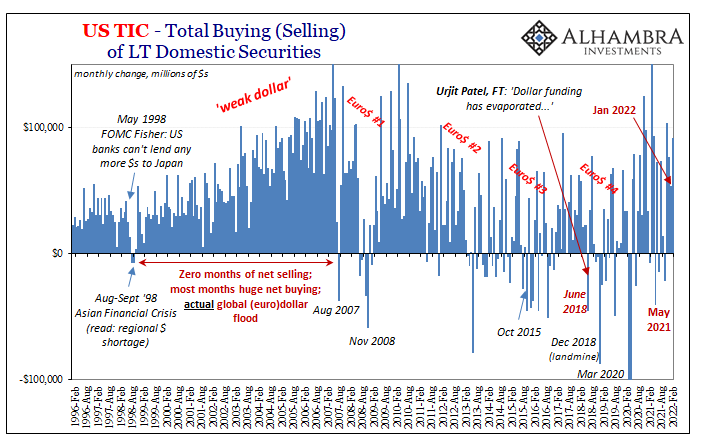

Looking Back At Chaotic March Through TIC

Looking Back At Chaotic March Through TIC20 May 2022

T-bills Targeted Target

T-bills Targeted Target20 May 2022

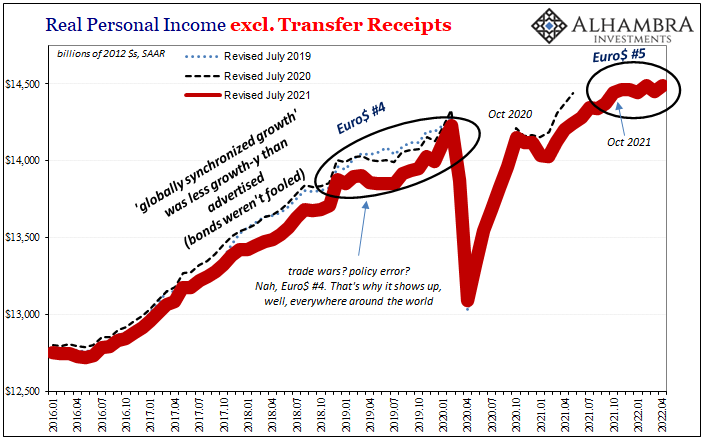

Industrial Synchronized Demand

Industrial Synchronized Demand11 May 2022

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets9 May 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

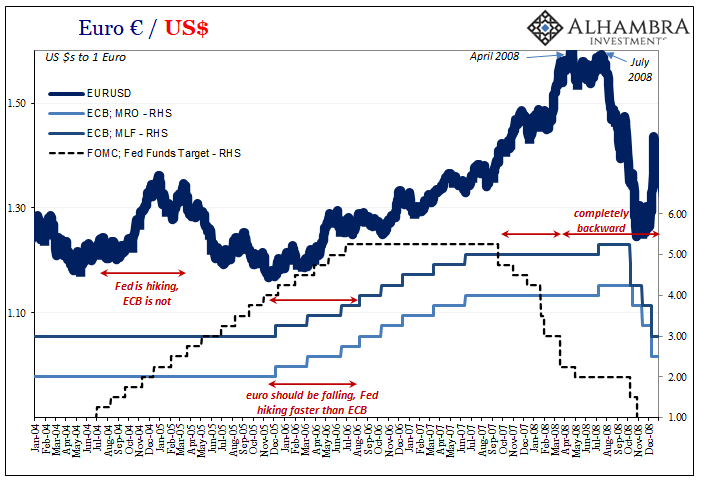

What Really ‘Raises’ The Rising ‘Dollar’

What Really ‘Raises’ The Rising ‘Dollar’3 May 2022

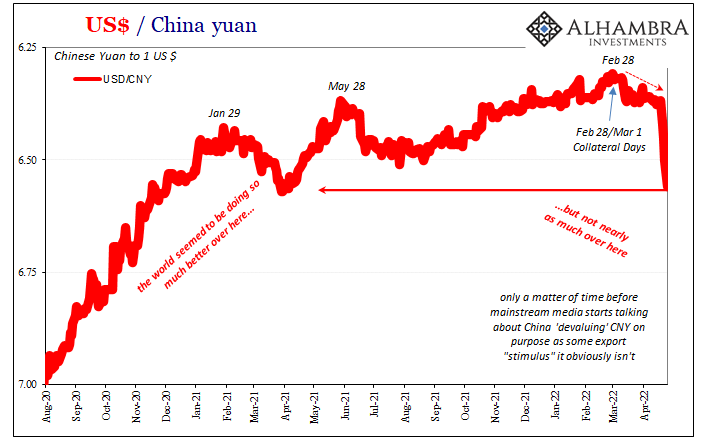

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now25 Apr 2022

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai25 Apr 2022

China, Japan, And The Relative Pre-March Euro$ Calm In February

China, Japan, And The Relative Pre-March Euro$ Calm In February22 Apr 2022

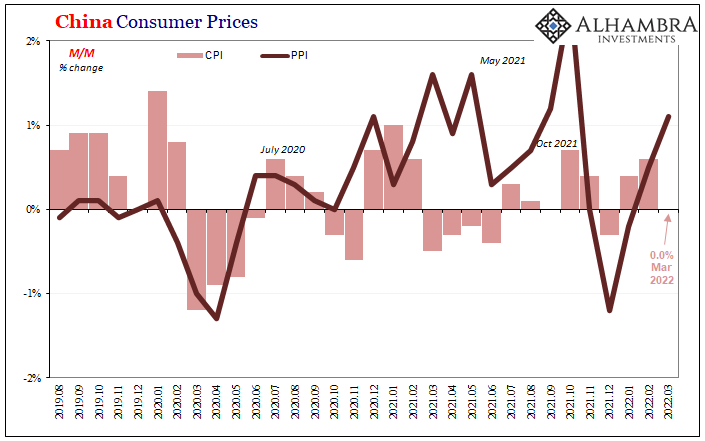

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’17 Apr 2022

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed16 Mar 2022

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift1 Mar 2022

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)14 Jan 2022

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed13 Jan 2022

Taper Rejection: Mao Back On China’s Front Page

Taper Rejection: Mao Back On China’s Front Page29 Dec 2021

White-Hot Cycles of Silence

White-Hot Cycles of Silence28 Dec 2021

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)25 Dec 2021

You Don’t Have To Take My Word For It About Eliminating QE

You Don’t Have To Take My Word For It About Eliminating QE24 Oct 2021