Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Bryan Caplan: Why Housing Costs DOUBLED

Bryan Caplan: Why Housing Costs DOUBLED11 Jun 2024

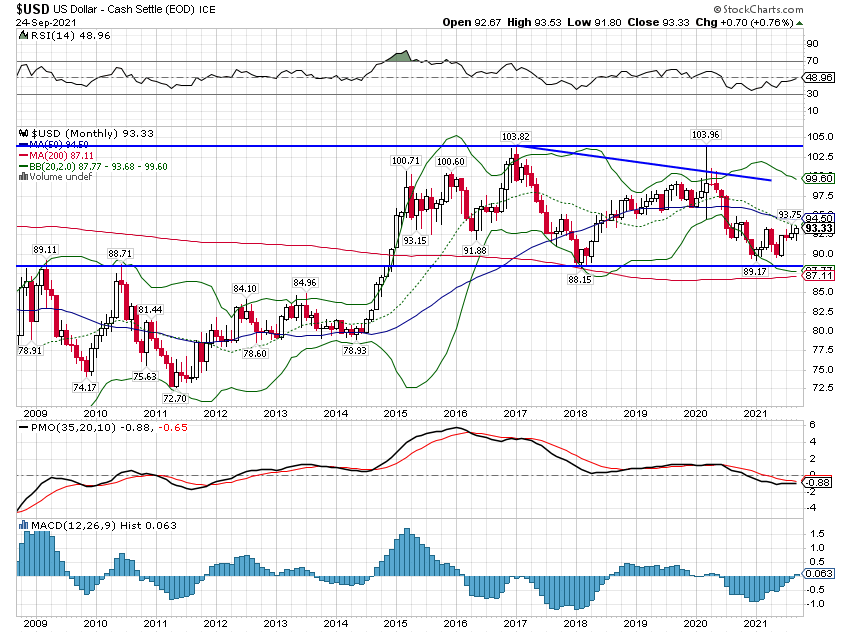

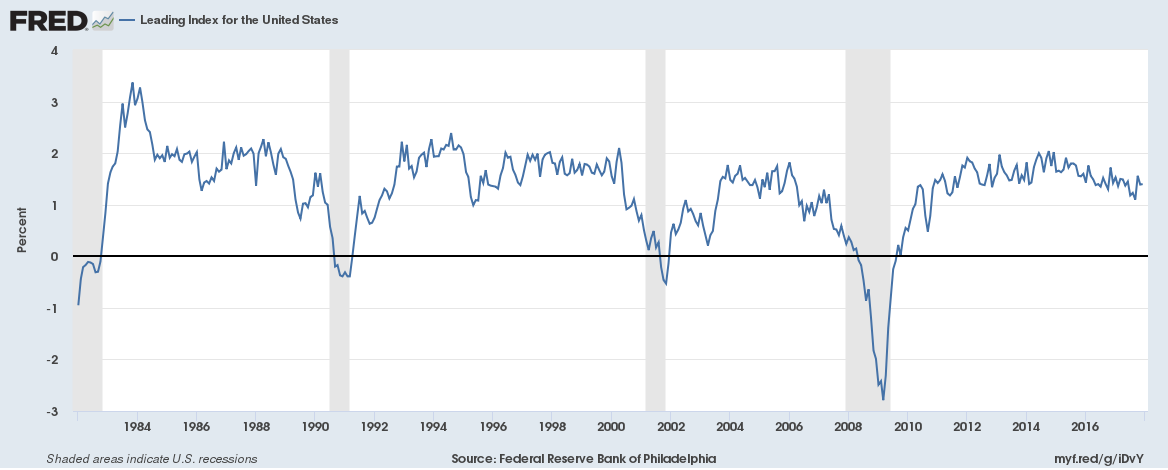

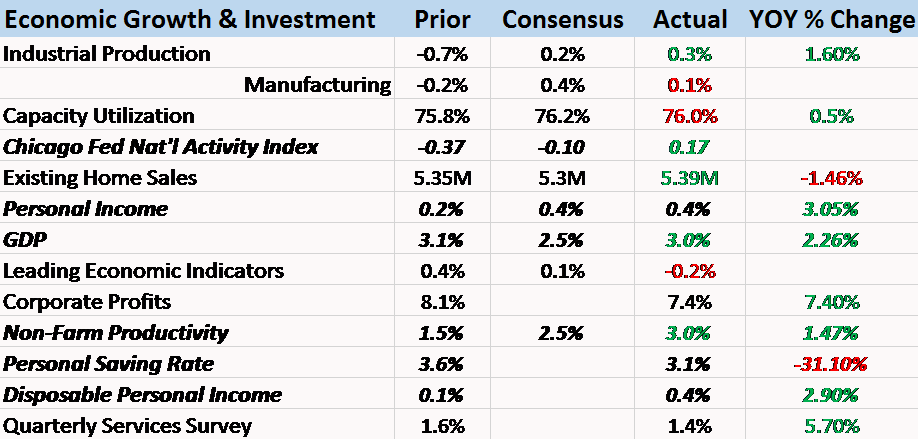

Weekly Market Pulse: Not So Evergrande

Weekly Market Pulse: Not So Evergrande27 Sep 2021

Monthly Macro Chart Review – March8 Mar 2019

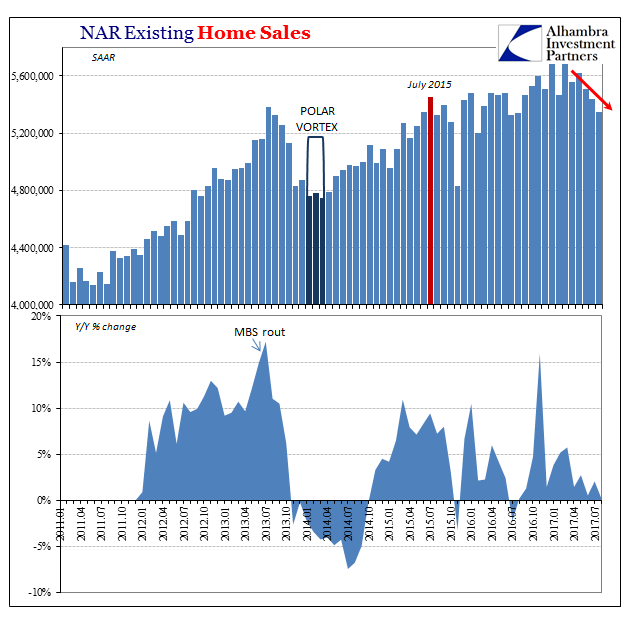

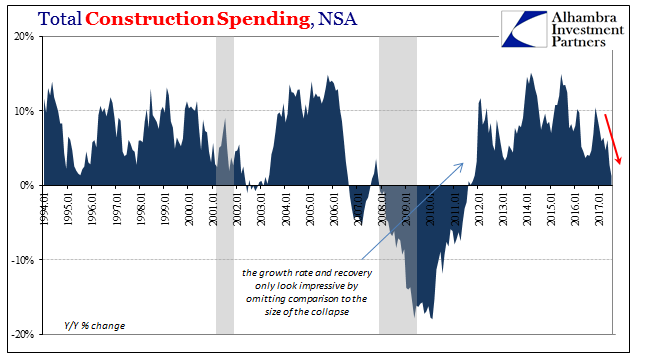

The Fate of Real Estate27 Feb 2019

Bi-Weekly Economic Review20 Jul 2018

Bi-Weekly Economic Review: Growth Expectations Break Out?22 May 2018

Bi-Weekly Economic Review: One Down, Three To Go

Bi-Weekly Economic Review: One Down, Three To Go1 Mar 2018

New Home Sales (Predictably) Fall Out of the Boom, Too28 Feb 2018

Bi-Weekly Economic Review: Gridlock & The Status Quo

Bi-Weekly Economic Review: Gridlock & The Status Quo8 Nov 2017

The Real Estate View For A Second Lost Decade29 Sep 2017

Now Capex?9 Sep 2017

Industrial Production Recovers in March: Strong Franc Digested?27 May 2016

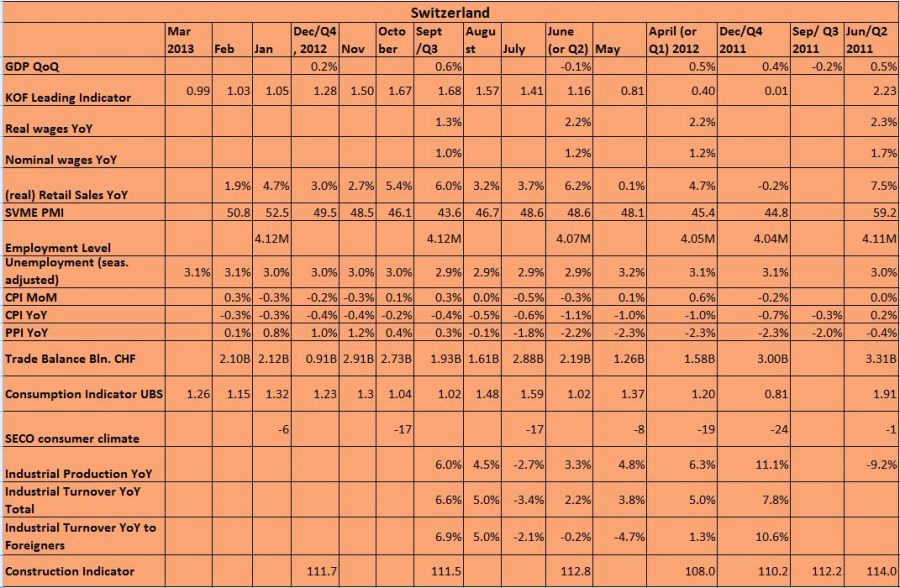

Swiss Economic Indicators, March 201327 Mar 2013

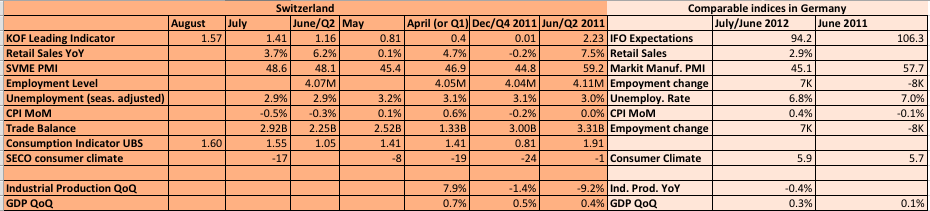

Swiss and German Economic Indicators, Update November 11 Nov 2012

Euro Crisis Has Affected Germany, Switzerland Still Immune26 Oct 2012

Economic Indicators: In Switzerland and Germany the Euro Crisis Seems to Be Far Away29 Aug 2012