Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Gesetzliche Rente nur Basisabsicherung

Gesetzliche Rente nur Basisabsicherung21 Apr 2026

Buchbesprechung: Hier stimmt was nicht von Frank Pöpsel – 60 Fakten, hinter den gängigen Narrativen

Buchbesprechung: Hier stimmt was nicht von Frank Pöpsel – 60 Fakten, hinter den gängigen Narrativen21 Apr 2026

What You’re Missing about the World War

What You’re Missing about the World War21 Apr 2026

Mercedes-Benz: Zwischen Finanzkraft und China-Krise

Mercedes-Benz: Zwischen Finanzkraft und China-Krise21 Apr 2026

Anton Hofreiter – Was ist los in Ungarn? #thorstenwittmann #geldpolitik #finanzstrategien

Anton Hofreiter – Was ist los in Ungarn? #thorstenwittmann #geldpolitik #finanzstrategien21 Apr 2026

The liquidity mechanism most investors miss and why it’s temporary

The liquidity mechanism most investors miss and why it’s temporary20 Apr 2026

La VERDAD sobre Irán (charla con Gustavo de Arístegui)

La VERDAD sobre Irán (charla con Gustavo de Arístegui)20 Apr 2026

Why gold sells off during acute market stress (and why that’s actually normal)

Why gold sells off during acute market stress (and why that’s actually normal)20 Apr 2026

Zinsen, Krieg, Unsicherheit: Stoppt das jetzt den Immobilien-Boom?

Zinsen, Krieg, Unsicherheit: Stoppt das jetzt den Immobilien-Boom?20 Apr 2026

Tanken zu teuer? Mehr verdienen!

Tanken zu teuer? Mehr verdienen!20 Apr 2026

Der Tag an dem du dein erstes Auslandskonto eröffnest #thorstenwittmann #geldpolitik #news

Der Tag an dem du dein erstes Auslandskonto eröffnest #thorstenwittmann #geldpolitik #news20 Apr 2026

Henryk M. Broder zelegt Aussage zur Wissenschaft

Henryk M. Broder zelegt Aussage zur Wissenschaft20 Apr 2026

Nächster Politschock für Brüssel: Bulgarischer Wahlsieger rechnet gnadenlos mit EU ab!

Nächster Politschock für Brüssel: Bulgarischer Wahlsieger rechnet gnadenlos mit EU ab!20 Apr 2026

USDJPY erases Friday’s losses on renewed US-Iran tensions as ceasefire deadline nears

USDJPY erases Friday’s losses on renewed US-Iran tensions as ceasefire deadline nears20 Apr 2026

The End of Financial Freedom? Why Your Money May Not Be Safe

The End of Financial Freedom? Why Your Money May Not Be Safe19 Apr 2026

ACHTUNG: Sie bauen ein neues WEF! Klingbeil als Vizekanzler bei Soros Event! Medien ahnungslos!

ACHTUNG: Sie bauen ein neues WEF! Klingbeil als Vizekanzler bei Soros Event! Medien ahnungslos!19 Apr 2026

El plan de Bessent para BAJAR el precio de la gasolina

El plan de Bessent para BAJAR el precio de la gasolina19 Apr 2026

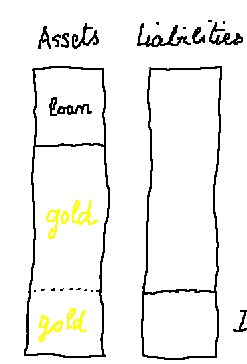

What central banks are quietly doing with their own reserves right now

What central banks are quietly doing with their own reserves right now19 Apr 2026

Reich werden ist erlernbar!

Reich werden ist erlernbar!19 Apr 2026

Reichelt: “Viele merken nicht, was gerade passiert!”

Reichelt: “Viele merken nicht, was gerade passiert!”19 Apr 2026