Read More »

Category Archive: 5.) Brown Brothers Harriman

EM Preview for the Week Ahead

Read More »

Recent Trade Developments Suggest Some Caution Ahead Warranted

Read More »

Dollar Firm as Risk-Off Sentiment Persists

Read More »

Dollar Firm as Risk-Off Sentiment Returns

Read More »

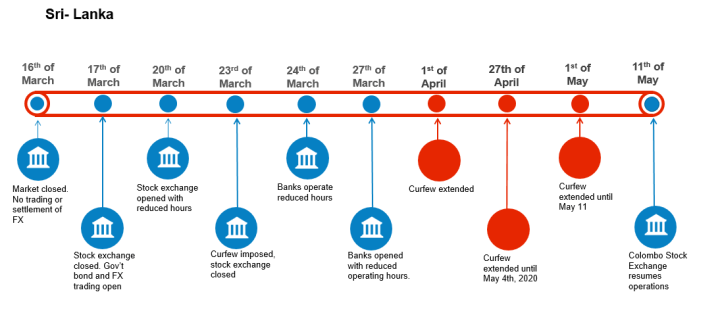

Restricted Market Trading Comments

There were minimal changes to the status quo as the week commences. Bangladesh has announced revised trading hours on the local exchanges. No change of status in Nigeria and Kenya as they both continue to face limited liquidity. Please see trading comments below.

Read More »

Read More »

Drivers for the Week Ahead

Read More »

Dollar Suffers as Stimulus Efforts Boost Market Sentiment

Read More »

EM Preview for the Week Ahead

Read More »

Dollar Firm as Risk-Off Sentiment Intensifies After FOMC Decision

Read More »

Dollar Firm as Risk-Off Sentiment Takes Hold

Read More »

Dollar Broadly Weaker Ahead of FOMC Decision

Read More »

Dollar Stabilizes as the New Week Begins

Read More »

Our Latest Thoughts on the Dollar

Read More »

Dollar Firm as Risk-On Sentiment Ebbs Ahead of ECB Decision

Read More »

Dollar Broadly Weaker After Reports of Possible Brexit Compromise

Read More »

Dollar Firm as US-China Tensions Continue to Rise

Read More »

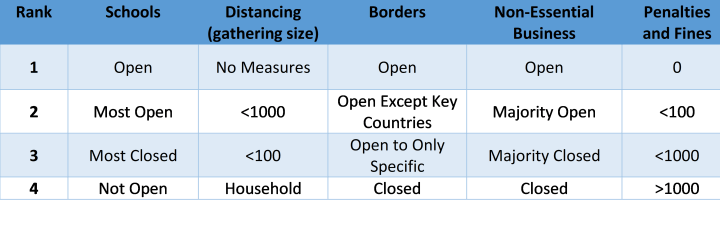

Asia Lockdowns vs. Re-Openings

Read More »

Hong Kong Turbulence Likely to Rise as US-China Relations Worsen

Read More »

Restricted Market Trading Comments

Read More »

Dollar Firm as China’s Hong Kong Gambit Triggers Risk-Off Trading

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: increased by 3.4 billion francs compared to the previous week

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

-

2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

-

SNB Brings Back Zero Percent Interest Rates

-

Hold-up sur l’eau potable (2/2) : la supercherie de « l’hydrogène vert ». Par Vincent Held

Main SNB Background Info

Featured and recent

-

Gekaufte Journalisten! Sogar BND involviert!!!

Gekaufte Journalisten! Sogar BND involviert!!! -

Ehrliche Antwort: Sondervermietung in Salzburg

Ehrliche Antwort: Sondervermietung in Salzburg -

Mega-Panne bei Wehrpflicht-Gesetz für Pistorius! Historisches Fregatten Desaster für die Bundeswehr!

Mega-Panne bei Wehrpflicht-Gesetz für Pistorius! Historisches Fregatten Desaster für die Bundeswehr! -

Achtung: FDP löst sich völlig auf! Kubicki und Strack-Zimmermann giften sich an!

Achtung: FDP löst sich völlig auf! Kubicki und Strack-Zimmermann giften sich an! -

IRAN: Spektakuläre Wendung! Krieg vorbei!? EU ist GROßER Verlierer!

IRAN: Spektakuläre Wendung! Krieg vorbei!? EU ist GROßER Verlierer! -

️ Exxon ist mehr wert als Nvidia?

️ Exxon ist mehr wert als Nvidia? -

I’m at a stage where I am passing along what I’ve learned.

I’m at a stage where I am passing along what I’ve learned. -

How Gold Moves Between East and West

How Gold Moves Between East and West -

Eilmeldung aus dem Finanzministerium! Klingbeil will Schuldenbremse sprengen!

Eilmeldung aus dem Finanzministerium! Klingbeil will Schuldenbremse sprengen! -

Constitutional Government and the Tenth Amendment

More from this category

Dollar Consolidates Its Gains Ahead of Jobs Report

Dollar Consolidates Its Gains Ahead of Jobs Report5 Feb 2021

Dollar Remains Firm Despite Dovish Fed Hold

Dollar Remains Firm Despite Dovish Fed Hold28 Jan 2021

Dollar Trading Sideways as FOMC Meeting Begins

Dollar Trading Sideways as FOMC Meeting Begins26 Jan 2021

Dollar Flat as Markets Await Fresh Drivers

Dollar Flat as Markets Await Fresh Drivers25 Jan 2021

Dollar Weakness Continues Ahead of ECB Decision

Dollar Weakness Continues Ahead of ECB Decision22 Jan 2021

Dollar Continues to Soften Ahead of Inauguration

Dollar Continues to Soften Ahead of Inauguration21 Jan 2021

Drivers for the Week Ahead

Drivers for the Week Ahead19 Jan 2021

Dollar Regains Some Traction as Markets Search for Direction

Dollar Regains Some Traction as Markets Search for Direction14 Jan 2021

Dollar Runs Out of Steam as Sterling Leads the Way

Dollar Runs Out of Steam as Sterling Leads the Way12 Jan 2021

- Drivers for the Week Ahead

21 Dec 2020

Dollar Continues to Soften Ahead of FOMC Decision

Dollar Continues to Soften Ahead of FOMC Decision20 Dec 2020

Some Thoughts on the Latest Treasury FX Report

Some Thoughts on the Latest Treasury FX Report18 Dec 2020

FOMC Preview

FOMC Preview15 Dec 2020

- Drivers for the Week Ahead

14 Dec 2020

Dollar Rally Running Out of Steam Ahead of ECB Decision

Dollar Rally Running Out of Steam Ahead of ECB Decision10 Dec 2020

Jittery Markets Keep the Dollar Afloat (For Now)

Jittery Markets Keep the Dollar Afloat (For Now)9 Dec 2020

Some Thoughts on a Potential US Government Shutdown

Some Thoughts on a Potential US Government Shutdown6 Dec 2020

Dollar Stabilizes but Weakness to Resume

Dollar Stabilizes but Weakness to Resume5 Dec 2020

Dollar Plumbs New Depths With No Relief In Sight

Dollar Plumbs New Depths With No Relief In Sight3 Dec 2020

- Drivers for the Week Ahead

30 Nov 2020