Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: An Energetic Market

Weekly Market Pulse: An Energetic Market18 Sep 2025

Weekly Market Pulse: Big Rate Cuts? Not Right Now

Weekly Market Pulse: Big Rate Cuts? Not Right Now18 Aug 2025

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Weekly Market Pulse: No Free Lunches

Weekly Market Pulse: No Free Lunches19 May 2025

Weekly Market Pulse: On The Road Again

Weekly Market Pulse: On The Road Again12 May 2025

Weekly Market Pulse: Peak America?

Weekly Market Pulse: Peak America?21 Apr 2025

Weekly Market Pulse: Tune Out The Noise

Weekly Market Pulse: Tune Out The Noise24 Feb 2025

Weekly Market Pulse: Is The Honeymoon Over Already?

Weekly Market Pulse: Is The Honeymoon Over Already?27 Jan 2025

Weekly Market Pulse: Questions

Weekly Market Pulse: Questions14 Oct 2024

Weekly Market Pulse: Did The Fed Just Make A Mistake?

Weekly Market Pulse: Did The Fed Just Make A Mistake?23 Sep 2024

Weekly Market Pulse: It’s An Uncertain World

Weekly Market Pulse: It’s An Uncertain World3 Sep 2024

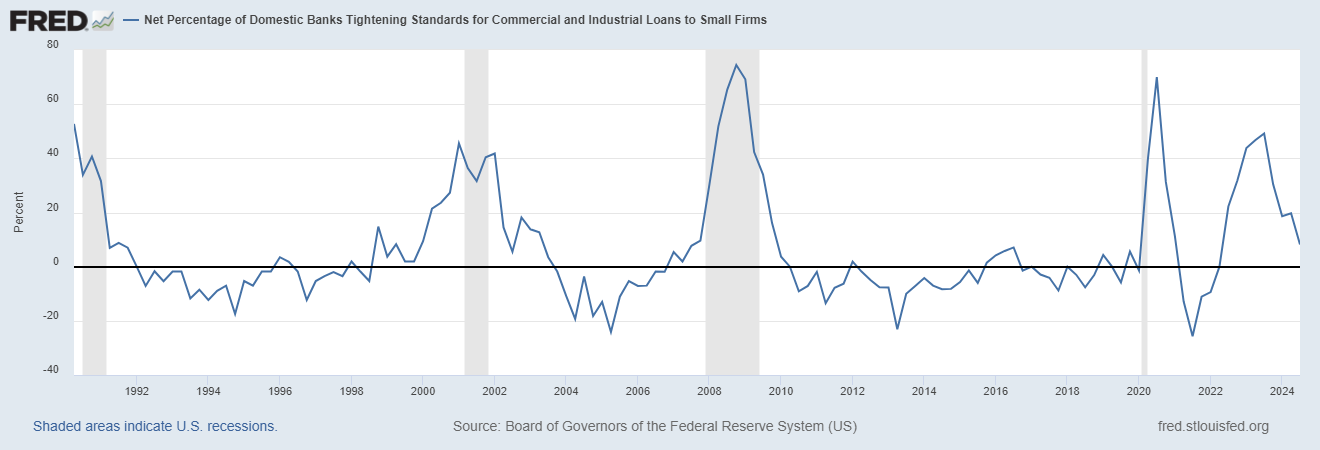

Market Morsel: SLOOSing

Market Morsel: SLOOSing6 Aug 2024

Q3 Cyclical Outlook

Q3 Cyclical Outlook25 Jun 2024

Weekly Market Pulse: The Sober Spending Of Drunken Sailors

Weekly Market Pulse: The Sober Spending Of Drunken Sailors24 Jun 2024

Market Morsel: How “The Market” Is Really Doing

Market Morsel: How “The Market” Is Really Doing12 Jun 2024

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

Market Morsels: ISM and Recession

Market Morsels: ISM and Recession7 Feb 2024

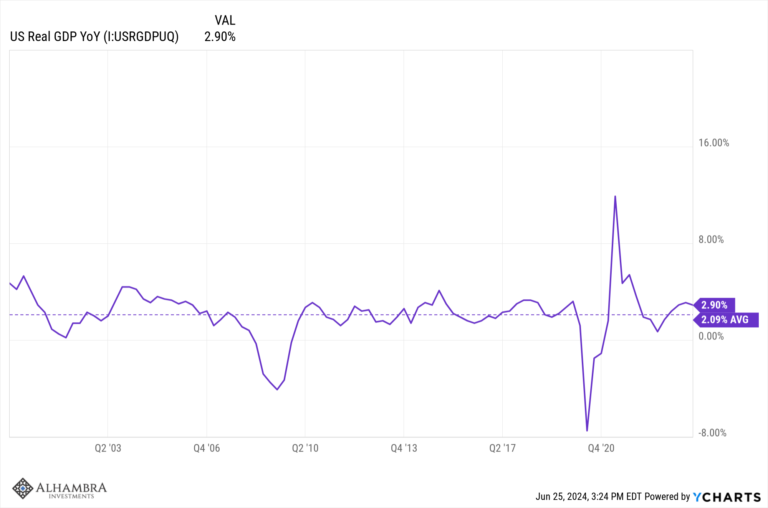

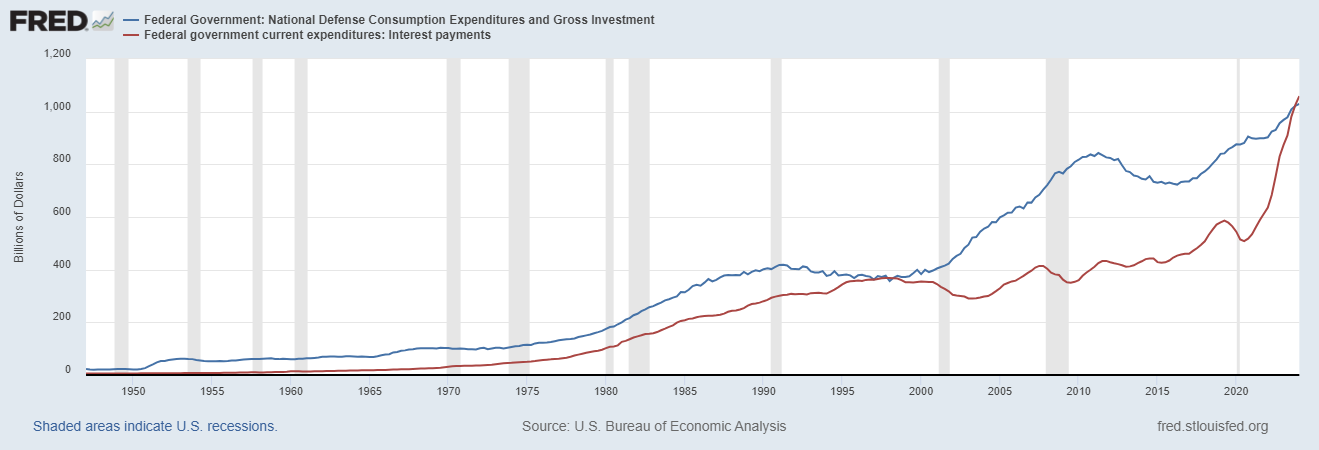

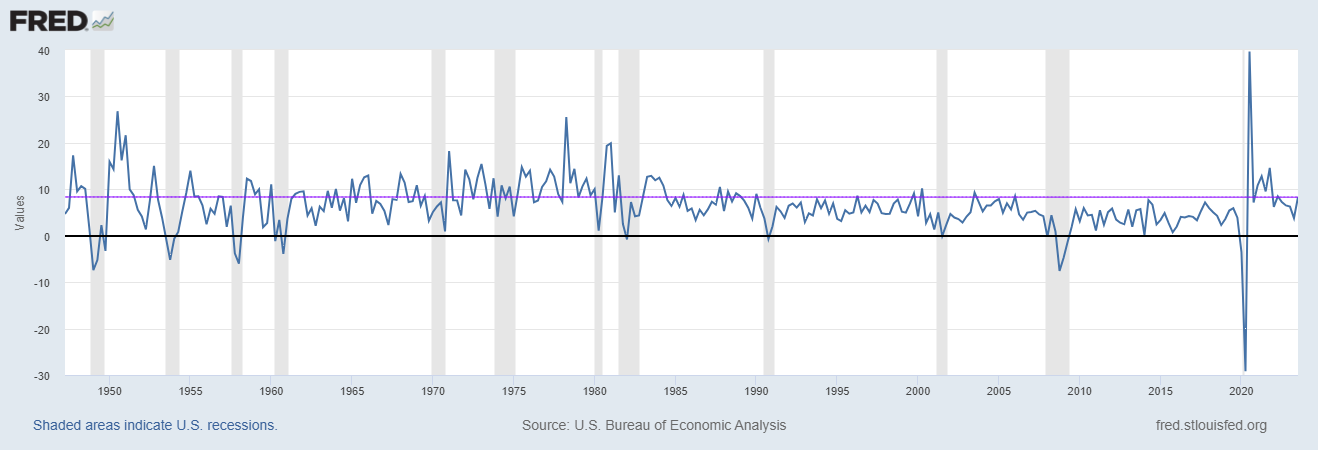

Macro: GDP Q3 — Inflationary BOOM!

Macro: GDP Q3 — Inflationary BOOM!22 Dec 2023

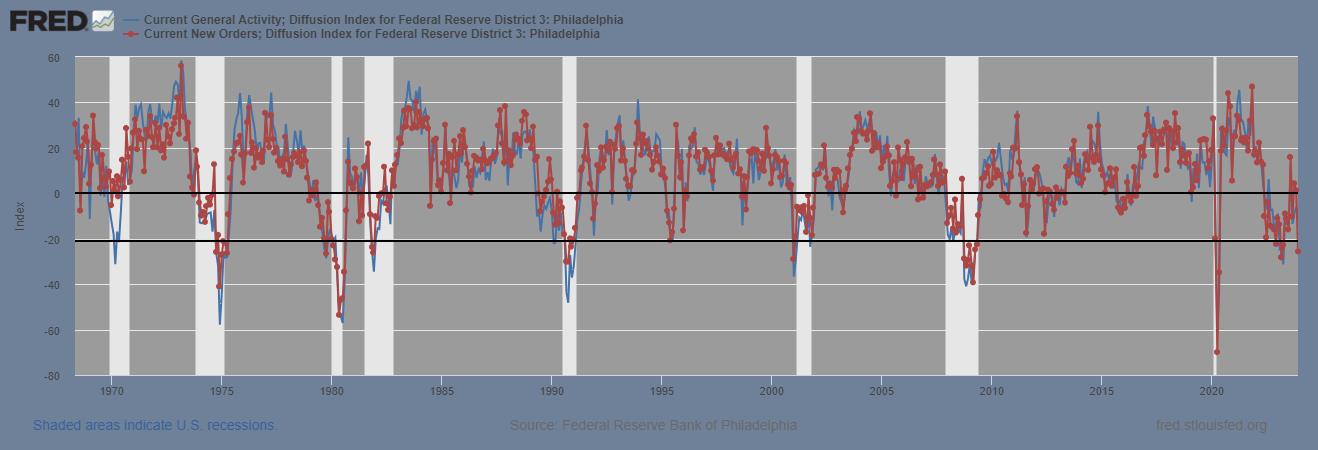

Macro: Philly Fed Mfg Survey — Umm

Macro: Philly Fed Mfg Survey — Umm22 Dec 2023

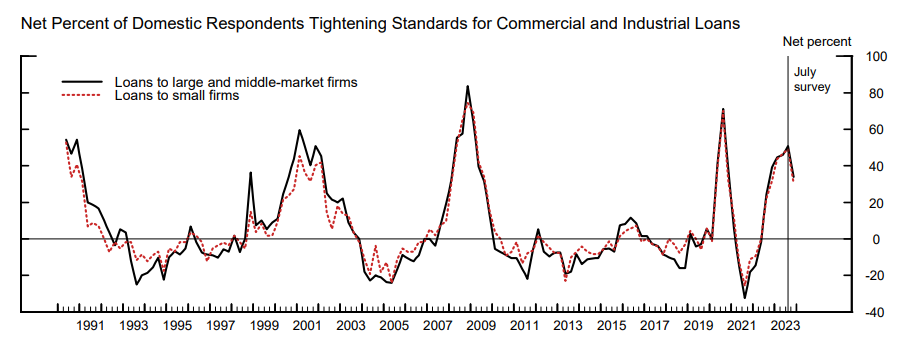

Macro: Banking: Senior Loan Officer’s Survey and Lending

Macro: Banking: Senior Loan Officer’s Survey and Lending8 Nov 2023