Charles Hugh Smith

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterFacebookYoutubeAmazon

| It would be very irritating to have a rally suck in all the bears salivating for a crash from a bear-market rally peak and then decimate the shorts with a rally that soars rather than collapses to new lows.

As a contrarian, I’m always squinting at the consensus and wondering if it is really that easy to be right.Now that everyone is bearish for reasons we all know–global recession, a hot war, energy scarcities and stagflation– I’m thinking, you know what would be really irritating? A bat-dung crazy rally to new highs in U.S. equities. Irritating, indeed, because few are positioned for this eventuality due to odds of it happening appearing to be near-zero. What’s odds-on is all the assets that bubbled up in the Everything Bubble sagging back to pre-bubble levels, or lower as global growth craters and stagflation stymies the easy fixes of money-printing and fiscal stimulus. How could stocks soar in such confounding, catastrophic circumstances? It doesn’t seem remotely possible, but when the herd starts running, rationality is not high on its list.When the herd is spooked and panics, rationality is not exactly the order of the day. The herd might thunder off a cliff absolutely convinced of the rightness of the stampede. Alternatively, rationalists stare with growing annoyance at a rally that makes no sense, and then with great reluctance are forced to join the herd in its irrational euphoria lest the rationalist fail to match the returns of the herd and suffer banishment to Financial Siberia. |

. |

| What could cause such an irritating, bat-dung crazy rally? I see three potential sources of bat-dung craziness:

1. Market contrariness. As Jesse Livermore observed, the market tends to take along the fewest possible punters in big moves. Some will say sentiment is poor but positioning is still bullish, so sentiment doesn’t matter. Perhaps. But a global recession is generally bad news for stocks, ditto hot wars, energy scarcities and stagflation (inflation in essentials and stagnant growth in employment, GDP, etc.). What’s the most punishing move for punters and pros alike–a crash or an irrational rally? I tend to think it’s not a crash, as too many people expect that now and punters who HODLed or bought the dip have been ill-treated by this year’s erratic decline. The smart money sold early and heavily, rotated out of tech into commodities, but alas, that hot trade is blowing up, too as the speculative positioning that pushed commodities to the moon is evaporating like mist in high-noon Death Valley. There are numerous powerful reasons to be in cash and remain wary of bear-market rallies. Given that backdrop, the most punishing move would be higher, tempting punters to short the bear-market rally every step higher, and then forcing them to cover with face-ripping losses. 2. Things aren’t as bad as everything now expects. The consensus is the economy is going over the waterfall and the only sound we’ll hear above the roar is the screams of punters who went long. But just suppose the blow-torch of inflation cools, employment holds up and the consumer ignores all the prognosticators of doom. Weirdly, consumers have deleveraged during the pandemic and the debt to income ratio isn’t that bad. Corporations that overshot staffing are slashing headcount by attrition and hiring freezes, along with layoffs. But lots of jobs are still going begging. Corporate profits will take a hit but as commodity inflation cools and their super-costly headcount drops, profits will look better a quarter out, and the market being what it is, a bizarre combination of irrationality, price discovery and forward-looking crystal-ball gazing, the hope for fatter profits a quarter or two out could spark a frenzy. 3. Core and periphery. We tend to forget that we’re all currency speculators, regardless of the asset we’re holding, be it cash, commodities, bonds, stocks, cryptos or real estate. Everything is arbitraged against the super-liquid currencies, an exclusive club of the yen, euro and U.S. dollar. (The Chinese RMB, being pegged by the Chinese government to the USD, is a derivative of the USD). |

. |

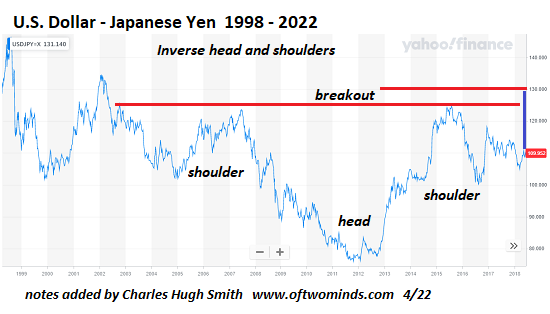

| As the charts below reveal, the USD has formed a long-term bowl-bottom and an inverse heads-and-shoulders in the USD-JPY pair.

Yes, the USD may sag back to support but the bottom line is the USD rising makes everything cheaper for those holding U.S. dollars and much more expensive for everyone holding other currencies or assets in other currencies. Capital goes where it’s treated well and U.S. markets are 1) a way to capture the gains of the U.S. dollar; 2) liquid and 3) relatively transparent compared to other markets. A couple of trillion seeking safe haven here, a couple trillion seeking safe haven there and pretty soon that influx of capital starts pushing U.S. markets higher. Note that everyone who sold assets priced in yen in January and moved their stash into USD cash just made 20% in six months. That’s a pretty nice return. Capital moves from the periphery to the core when things start wobbling. It would be very irritating to have a rally suck in all the bears salivating for a crash from a bear-market rally peak and then decimate the shorts with a rally that soars rather than collapses to new lows. The rally would be even more irritating if it left all the smart money on the sidelines because a rally simply doesn’t make sense. With great weeping and gnashing of teeth, the smart money is then forced to chase the rally higher. Yes, this is implausible, impossible, etc. That’s why it’s increasingly likely. Is it really that easy to be right? As a general rule, no. |

. |

Full story here Are you the author?

Tags: Featured,newsletter