Geopolitical events are among the most reliable drivers of bad investment decisions. When headlines are alarming, and markets are volatile, as they are today, investors instinctively overweight worst-case scenarios and underweight the likelihood that the situation resolves more quietly than feared. Behavioral finance calls this availability bias: the tendency to judge the likelihood of an outcome by how easily a vivid example comes to mind. Headlines like "Iran War Oil Shock Threatens Wave of Global Inflation" coupled with intense market swings are as vivid as it gets.

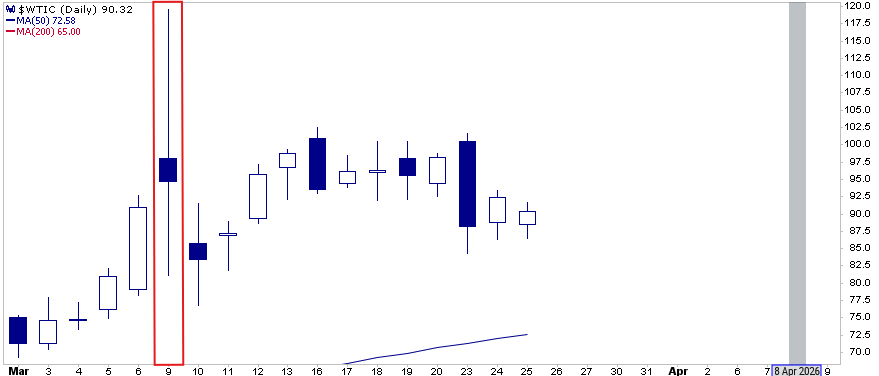

On March 9, crude oil spiked as investors priced in worst-case scenarios involving the closing of the Strait of Hormuz and supply disruptions. To wit, fears of a 1970s-style inflationary shock took hold. That day, crude oil opened $7 higher and rose another $21 to peak at $119.50. It then plummeted to $81, before closing at $94.75. Patient investors who did nothing were rewarded for their patience. Many investors who emotionally bought at the highs or sold at the lows paid a steep price. They made the mistake of treating the large price swings as information when it was largely noise.

History is consistent on this point. As we have seen, initial market reactions to geopolitical events, from the Gulf War to 9/11 to the more recent Russia-Ukraine conflict, are reminders that in many cases the initial price moves overstate the ultimate economic impact. The takeaway for investors, during times of geopolitical stress, is to let the market separate the signal from the noise before making rash portfolio decisions. It is never easy, but history suggests that patience during geopolitical crises is almost always the right instinct.

What To Watch Today

Earnings

Economy

Market Trading Update

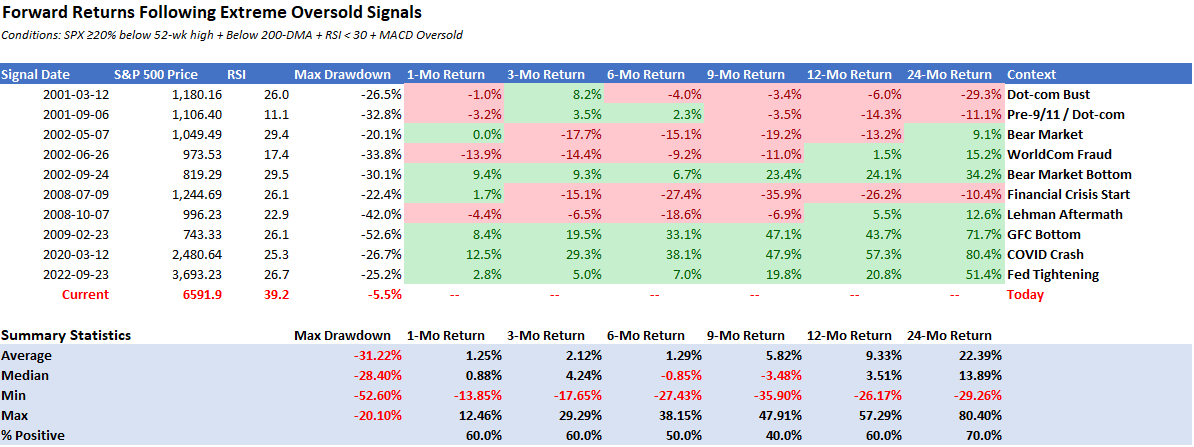

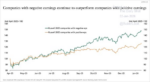

Yesterday, we discussed the forward returns of energy stocks when oil prices revert from crisis-related events. It has been a rough market as of late, and, as discussed earlier this week, a significant number of stocks are in a "bear market." Currently, approximately 42% of S&P 500 members are down 20% or more from their respective 52-week highs. The index itself has broken below its 200-day moving average, and both MACD and RSI have crossed into oversold territory. Three conditions, all aligning simultaneously, have certainly put investors into a more fearful position.

However, while the initial urge is to "panic sell" into the market, the data suggests patience. For a test, I went back and examined every historical instance since 2000 where all three conditions coincided:

- Widespread breadth damage with 40% or more of S&P 500 stocks in bear territory,

- The index is trading below its 200-DMA, and

- Momentum indicators are in oversold territory.

The setups include late 2002, the 2009 bottom, February 2016, December 2018, March 2020, and late 2022. Importantly, all those previous conditions are present when an "event" coincides with a recessionary impulse. That isn't the case today, at least not yet, but a notable difference.

However, as shown, one month out, average returns were positive, and the median is essentially flat. Three months out, returns are only modestly positive. While the pain tends to linger before it resolves, these are periods heavily impacted by economic weakness, declining earnings growth rates, and valuation reversions.

Once you move away from the initial combination of declining stocks and an oversold market, forward returns begin to improve markedly. By 12 months, the average return climbs to roughly +9%. At 24 months, you're looking at average gains exceeding 22%, with 70% of comparable periods producing positive outcomes.

The point is not that you should not manage risk in the short-term. You absolutely should. However, it is important not to extrapolate current market action indefinitely into the future. This shall pass, and markets will begin focusing on what comes next.

Obviously, the worst outcomes in this data set were centered around the Dot.com crash and the Financial Crisis. These were recession-driven episodes in which the damage persisted for well over 12 months before recovery. If we're heading into a genuine contraction, those numbers look worse in the near term. If this is a sentiment-driven correction without an underlying earnings collapse, the recovery curve steepens much more quickly.

The current setup has features of both camps. The Iran conflict has injected a genuine macro shock. But the deeply oversold RSI reading at the 200-DMA break, combined with AAII bearish sentiment above 52%, is historically the ingredient of reflexive rallies, not capitulation spirals. As I noted last week, the goal isn't to go to cash and wait. It's to reduce the cost of being wrong while staying positioned for the recovery when it arrives.

Gates And Financial Ignorance Feed Private Credit Woes

The private credit industry is facing a problem largely of its own creation. According to a Bloomberg article, at a recent industry conference, two senior executives in private credit, Jim Zelter of Apollo and Doug Ostrover of Blue Owl, said their sales teams failed to adequately explain redemption restrictions to their retail and high-net-worth investors. As a result, those investors are now clamoring to sell, but in many cases are restricted in how much they can sell.

Apollo Debt Solutions capped redemptions at 5% of shares after investors sought to redeem 11.2%, and the $10.7 billion Ares Strategic Income Fund imposed the same cap after clients requested redemptions of 11.6%. Many other funds are limiting redemptions as well. This is a clear sign that the less sophisticated retail investor base, who were sold higher-yielding private credit funds, did not fully understand redemption gates and how their money/liquidity could be locked up.

The large redemption requests, coupled with the gates put in place for investors, are creating the appearance of a liquidity crisis. Yes, private credit losses are increasing, but the problem is being exaggerated by the many unhappy investors who are unable to sell. Furthermore, this provides evidence that, in the pursuit of higher returns, many investors were not paying attention to the potential risks and limitations of their investments. The funds clearly warn investors of the liquidity risks they could face. The highlighted sections in the graphic below are from page 2 of the BlackRock Private Credit Fund N2 SEC filing.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Geopolitical Headlines Can Be Hazardous To Your Wealth appeared first on RIA.

Full story here Are you the author?You Might Also Like

Corporate Debt Tranches: Why Issuers Are Slicing Jumbo Deals

Corporate Debt Tranches: Why Issuers Are Slicing Jumbo Deals

2026-03-24

According to a recent analysis by the Wall Street Journal, corporate treasurers are fundamentally shifting how they approach the capital markets to navigate record-breaking supply. Rather than offering debt in monolithic blocks, firms are increasingly utilizing multiple corporate debt tranches to better manage investor demand. This strategic shift has pushed the average number of pieces …

The Bear Market Hiding Beneath The Calm Surface

The Bear Market Hiding Beneath The Calm Surface

2026-03-20

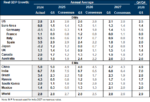

Many investors consider a 20% drawdown or more to be a bear market. Based solely on that definition, the table below, courtesy of Morgan Stanley, shows that 42%, or over 200 of the S&P 500 members, are in a bear market. For context, the S&P 500 is only down 4% from its 52-week record high, …

Warsh To Head The Fed

Warsh To Head The Fed

2026-02-02

The wait is over, and President Trump has nominated Kevin Warsh to head the Federal Reserve. To better appreciate Warsh’s views on monetary policy and what they may entail for markets, we summarize a recent Wall Street Journal editorial he wrote, The Federal Reserve’s Broken Leadership. Our market-related thoughts are below the bullet points. From …

Mainstream Expectations: Hope Vs. Potential Risk

Mainstream Expectations: Hope Vs. Potential Risk

2026-01-30

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure. As such, many institutional investors interpret this as a year of opportunity for markets and corporate earnings.That was a …

The Reflation Narrative Stumbles Out Of The Gate

The Reflation Narrative Stumbles Out Of The Gate

2026-01-26

With a 4.4% increase in economic growth in the third quarter and expectations that it could be higher in the fourth quarter, the so-called reflation narrative appears primed to dash out of the gates in 2026 at its current strong pace. The problem with assuming the reflation narrative will hold in 2026 is that it …

Does AI Capex Spending Lead To Positive Outcomes?

Does AI Capex Spending Lead To Positive Outcomes?

2025-12-12

As someone who views corporate finance through a pragmatic lens, I’ve been closely watching the current surge in capital expenditures (capex) tied to artificial intelligence (AI). The question I’m addressing here is this: when a company spends massive amounts of free cash flow and takes on increasing debt, in this case for AI CapEx, does …

Hawkish Or Less Dovish? QE Or Not QE?

Hawkish Or Less Dovish? QE Or Not QE?

2025-12-11

There is a growing divergence of views among FOMC members. Some remain dovish, favoring more rate cuts. Their argument is based on a belief that inflation will continue to move toward the 2% target and that the weakening labor market benefits from lower interest rates. On the other side of the aisle are hawkish views. …

Tags: Featured,newsletter