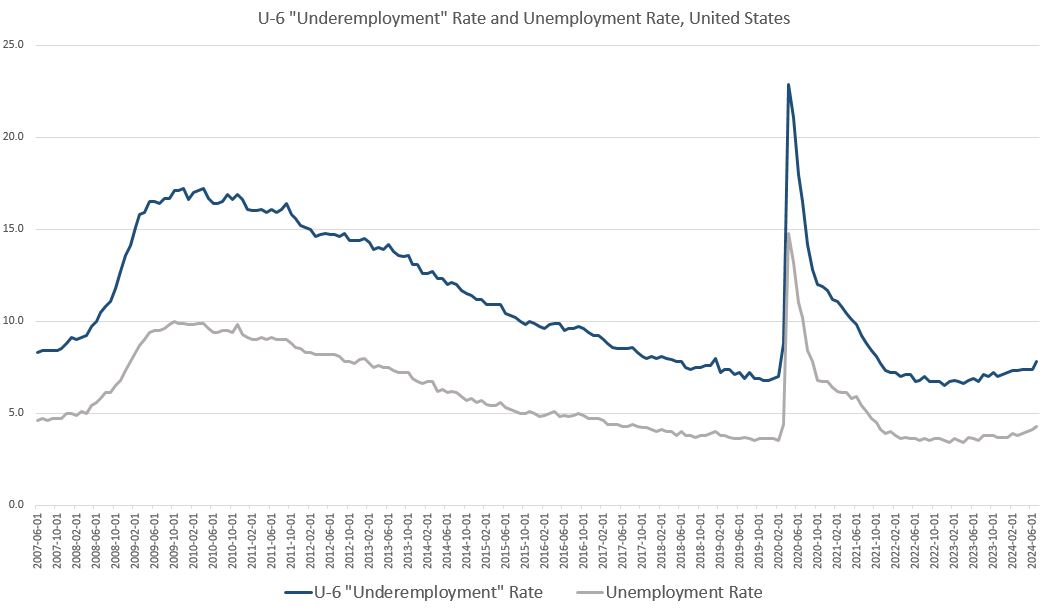

According to the most recent report from the federal government’s Bureau of Labor Statistics, the US economy added 114,000 jobs (according to the establishment survey) during July. This was a lackluster number that came in below expectations, and it wasn’t enough to prevent a surge in the unemployment rate up to 4.3 percent. Moreover, the “underemployment” rate, the “U-6” unemployment rate, jumped substantially from 7.4 percent to 7.8 percent. Excluding the Covid Panic, that’s the largest year-over-year increase in U-6 since the Great Recession.

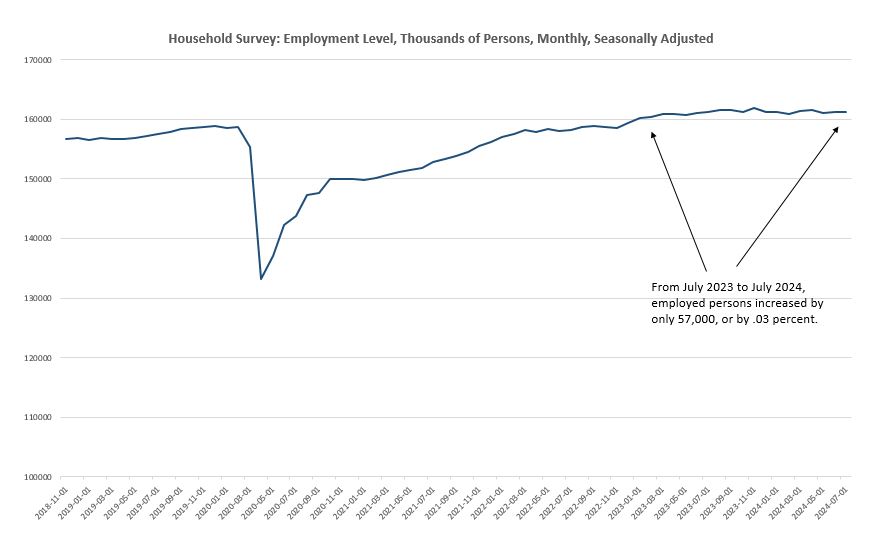

At the same time, the BEA’s other employment survey, the household survey, showed that the year-long stagnation in employment continued into July. According to the household survey, total employed persons in the United States increased by only 57,000 from July 2023 to July 2024—an increase of a mere 0.03 percent. Since September of last year, the number of employed persons has fallen by 284,000.

Moreover, the establishment survey continues to be suspect in light of the so-called “birth-death” model as well. This model is used to estimate how many new jobs were created by new businesses—i..e, “births”—that are missed by the actual survey results. The BLS says it must use “non-sampling methods” to add in these newly created jobs. “Non-sampling methods” means the numbers are made up by number crunchers. They don’t show up in any survey. In July, the establishment survey simply assumed the creation of 246,000 jobs.

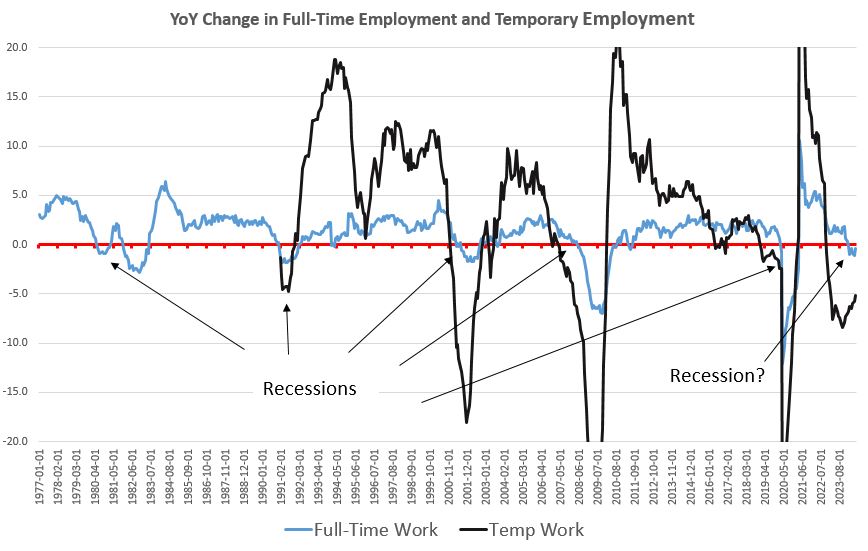

Other indicators have long pointed to a disappointing employment situation. The nation has been in a recession in full-time jobs for months. That is, part-time jobs have accounted for the vast majority of employment growth over the past year, while growth in full-time jobs has largely disappeared. Full-time employment has fallen, year over year, for the past six months. Meanwhile, temporary employment has been down, year over year, for the past 21 months. Both of these trends are strong recession indicators.

In spite of all these other indicators, the media over the past year has steadfastly doubled down on the establishment survey—the one indicator that continued to show significant job growth. Following the release of today’s report, however, it seems serious cracks are now appearing in the narrative. In the financial media, claims that the US is in the midst of a Bidenomics-fueled boom now appear all but dead. This may be due to the fact that the unemployment rate’s surge has triggered the so-called “Sahm rule” which is influential among finance media pundits.

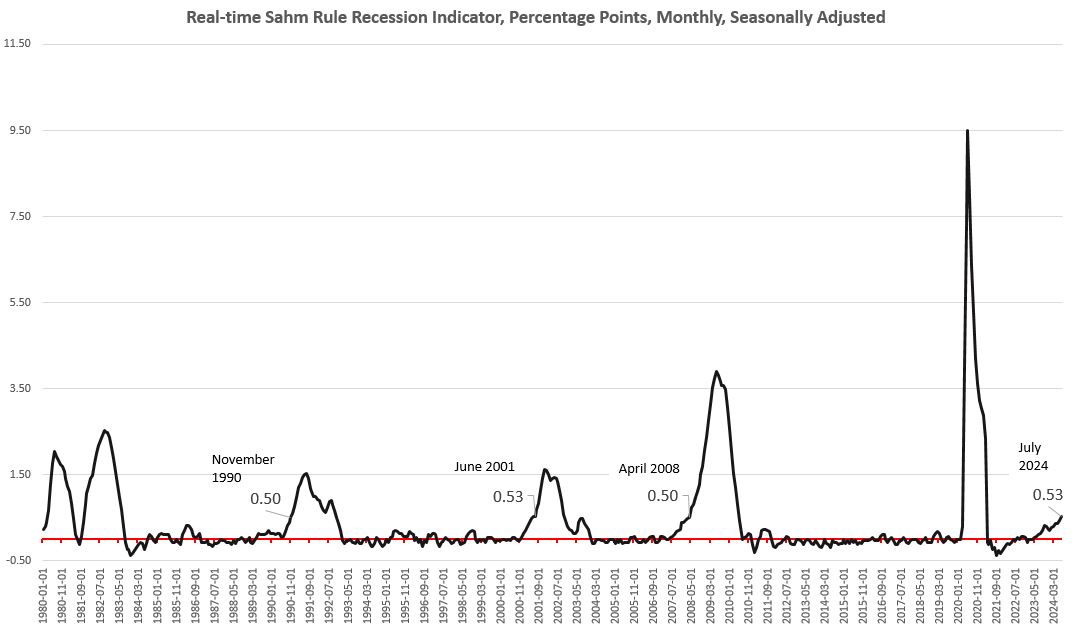

According to the Sahm rule, a recession is expected “when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to the minimum of the three-month averages from the previous 12 months.” In July, that three-month moving average hit 0.53 percent. That’s the highest since the Covid Panic, and it’s now following a pattern similar to Spring 2008 as the US entered the Great Recession.

Indeed, the response from Wall Street to today’s jobs report is quite different from what we’ve seen in most months during the age of Bidenomics. Over the past year—until today—the market’s reaction to an unimpressive employment report had generally reflected a “bad news is good news” attitude. The Dow and other market indices would often surge on “bad news.” It was assumed that bad economic news would trigger easy money from the Fed that would then lead to one of those mythical “soft landings” that the central bank claims is on the horizon.

The tone appears to be different today, however. As of this writing, the Dow is down more than 850 points, and the S&P 500 is “potentially on pace for its worst day since 2022.” There is a growing chorus of investment bankers calling for the Fed to intervene immediately, slash the federal funds rate, and flood the economy with easy money. Rising numbers of Wall Street pundits appear doubtful that the Fed can achieve its proposed soft landing at this point, especially if the Fed waits until its September meeting to slash the target interest rate.

In the Fed We Trust

This is quite a shift in tone from Wednesday when the Fed’s Federal Open Market Committee announced it would hold the federal funds rate steady at 5.5 percent—although the Fed strongly hinted that a rate cut was coming in September. In response to this news, markets were fairly serene. But what a difference 48 hours makes. With the September meeting nearly two months away, and in light of the new employment numbers, many on Wall Street would prefer to see the Fed panic right now and call an emergency meeting.

Frequent readers of mises.org will note the problem with this way of thinking. The fact that we hear these calls for the Fed to hit the panic button and “print the money” shows that many financial-sector analysts are still clinging to the false notion that the Fed can engineer a “soft landing” and somehow end the boom-bust cycle. A common sentiment one sees among investment analysts in social media and in the financial media is that the Fed can steer a painless path between high inflation and recession as long as the Fed doesn’t make a “policy error.” The policy error in question is usually assumed to be one in which the Fed allows interest rates to rise for “too long” and then cuts target rates “too late.” There is no evidence whatsoever to support this false hope. The Fed never delivered on any of its promised “soft landings.”

Moreover, the “policy error” we need to fear is not the Fed failing to pump easy money at the “right time.” The Fed’s policy error already occurred years ago. The real policy error was forcing down interest rates to near-zero or zero levels for more than a decade after the 2008 financial crisis. That was made worse by the additional and enormous policy error. That was the error of essentially printing trillions of dollars during the Covid Panic to bribe people to stay home and not work.

The best thing the Fed could do now is avoid yet another policy error by letting a real recession finally pop all those inflationary bubbles that the Fed has been maintaining since it first created a housing bubble after the 2001 recession. Thanks to the Fed’s asset purchases of mortgage-backed securities and government bonds after 2008, we are still looking at bubbles in home prices, bond prices, and other bubbles that have yet to be discovered. Only a recession and an unwinding of malinvestments can undo the many real policy errors of recent decades.

Without this, we’ll continue to face an increasingly fragile economy that perennially relies on ever greater infusions of easy money just to keep the economy afloat. The result will be ever mounting levels of price inflation with no deflationary periods to ever offset the rising prices that are crushing younger families and consumers.

Federal Reserve Forecasts Are Useless

As a final note, I just want to point to how today’s numbers show how utterly useless the FOMC’s economic projections are as an indicator of real world economic activity.

In its Summary of Economic Projections released on June 12, the elite economists and analysts of the Federal Open Market Committee reported their forecasts for where the unemployment rate is headed in the United States. The FOMC predicted a median unemployment rate of 4.0 for 2024, 4.2 for 2025, and 4.1 for 2026. The “longer run” projection for unemployment was 4.2 percent. Overall, the SEP makes it clear that few members of the FOMC were willing to say that the unemployment rate might rise much above 4.2 percent over the next three years.

Well, it’s already clear that those numbers are quite divorced from reality, and provide us with zero insight into how the economy is likely to look in 2025 and 2026. The employment numbers were so soft in July that the unemployment rate has already exceeded the projections of most FOMC members. Moreover, all experience points to the unemployment rate increasing further in coming months. That projected 4.2 percent unemployment rate for 2025 is looking like a whole lot of wishful thinking.

Of course, we should not believe for a minute that the published forecasts of the SEP reflect the actual opinions of the members of the FOMC. The SEP is a propaganda document designed to push a picture of the economy that supports regime policies and plans. The SEP, like the FOMC’s press conferences and “forward guidance” are tools of narrative management. They exist to manipulate public opinion about the state of the economy. Not surprisingly, the SEP virtually always predicts relative economic stability and predictability.

Image Credit: Alex Proimos via Wikimedia. This file is licensed under the Creative Commons Attribution 2.0 Generic license.

Full story here Are you the author?Tags: Featured,newsletter

.jpg){kind=link}