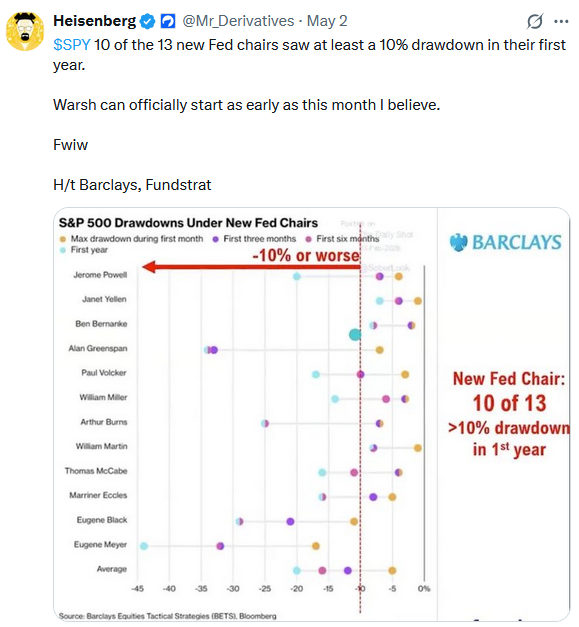

Michael Nicoletos wrote a thoughtful paper titled "The Index Trap," making a compelling case that active investing, i.e., picking individual stocks versus buying baskets of stocks (ETFs), will outperform in the future. If correct, that would reverse the trend over the last two decades, in which investors increasingly relied on passive investment strategies. The following is a brief summary of his thesis.

Low ETF fees, consistent outperformance relative to active managers, and instant diversification have led to passive strategies gaining popularity over active ones. The graph below shows that, at year-end 2025, indexed funds accounted for 52% of all long-term US fund assets. BlackRock, Vanguard, and State Street, the three largest ETF issuers, are now the largest shareholders in 88% of S&P 500 companies. This isn't a market anymore. As Nicoletos bluntly puts it,

A market in which a tiny group of price-insensitive intermediaries owns everything is no longer a market that prices things. It just rebalances.

Meanwhile, AI, the primary driver of recent market returns, isn't equally rewarding to all companies. It's splitting the corporate world into AI winners and losers. For instance, hyperscalers will spend over $700 billion on capex in 2026, likely generating significant profits down the road. To wit, he notes that Nvidia accounted for 20% of the S&P's 2025 return on its own. While some companies benefit, others, such as software companies, are grossly underperforming as the market anticipates weaker earnings due to AI-related competition. The technology-sector ETFs and the broad-market ETFs own both AI winners and losers. That's the trap he sees:

Mechanical buyers do not look at price, do not read earnings, and cannot tell the difference between Nvidia and a commoditized software vendor. They buy both, in proportion to whatever weights they have been given. In the future, it means owning the AI winners and the AI losers in the same vehicle, dragged down by every name the index cannot rotate out of. The same robot that bought stocks without thinking will, on the way down, sell stocks without thinking

It’s a trap, but he sees an opportunity for active investors. To wit:

The allocators who will win in the next decade will not be those who buy the average. They will be those who build a deliberate basket of AI infrastructure, AI native software, disruption-resistant compounders, and adjacent winners, and who avoid the long tail of names the index has no choice but to hold.

There is much more to his paper than we shared. But to sum it up, there is now an opportunity for disciplined, concentrated stock picking that hasn't been around for many years. Below, we provide a counterpoint to his thesis.

What To Watch Today

Earnings

Economy

Market Trading Update

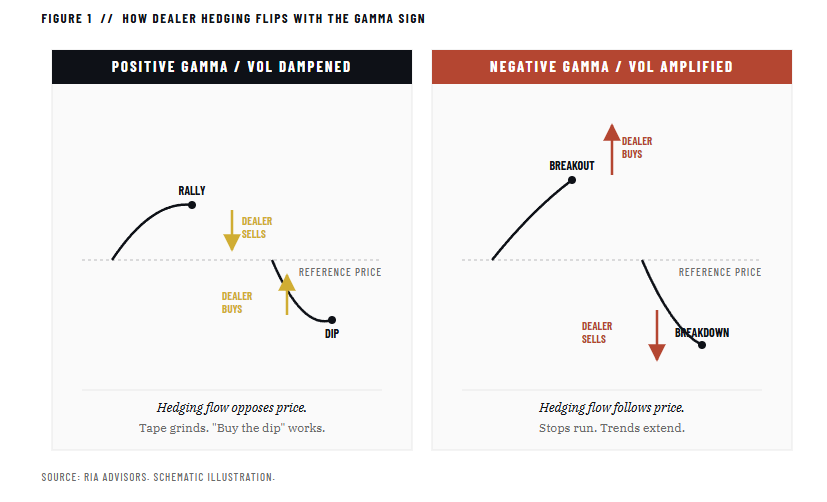

Yesterday, we discussed how Gamma affects the market. Last weekend, we discussed the Q1 earnings season, which has been stellar on most fronts. In this coming weekend's report, we will do a deeper dive into forward estimates, but I will give you a bit of a preview here.

The Q1 2026 earnings season is delivering a result Wall Street rarely sees. With roughly two-thirds of the S&P 500 reported, blended earnings growth has climbed to 27.1% year-over-year, more than double the 13.2% consensus modeled at quarter-end. 84% of companies have beaten EPS; the average surprise is 20.7% (nearly three times the 5-year norm), and the net margin of 14.7% is the highest reading in over 15 years.

That's the surface. The more interesting story is why analysts were so wrong heading in. The 2026 EPS estimate index cratered to 0.96 last summer during the Iran shock, then turned vertical. By May, it's broken above 1.06. In a normal year, analysts walk estimates down from 1.00 to roughly 0.92 by year-end. We're looking at a 14-point swing versus the historical pattern. Morgan Stanley calls it “fairly unprecedented,” which is analyst-speak for something they don't have a clean comparison for.

Three things are driving the upside. First, the AI capex cycle is finally landing on income statements. Communication Services is reporting +53%, Tech +50%, Consumer Discretionary +39%. The Mag 7 alone moved from a 22.4% expected growth rate at quarter-end to a 61% blended print today. Four of the top five contributors to S&P 500 earnings growth are Alphabet, NVIDIA, Amazon, and Meta. Second, margins are at a record. Revenue grew 11.1%. Earnings grew 27%. The gap is operating leverage. Companies that cut headcount in 2023 and held the line through 2025 are now monetizing every incremental dollar at a higher margin. Third, breadth is finally improving. Median S&P 500 company growth is in the double digits for the first time in four years. All eleven sectors are tracking positive growth.

Here's where I have to put the brakes on. The current reading on long-term S&P 500 earnings growth estimates sits near 19%, the highest print since 2000. The chart's prior peaks tell a story. The “New Economy” peaked in 2000. The “Tax Cuts” peaked in 2018. The “COVID” rebound peaked in 2021. Each was followed by a meaningful equity drawdown and a sharp downward revision cycle within twelve to twenty-four months. The S&P fell 49%, 19%, and 25%, respectively. Forecasts above the long-term trend channel have a poor history.

“When everybody is revising higher, the marginal trade is no longer to buy the beats. It's to fade the next miss.”

The setup that worries me isn't that earnings are bad. It's that they're so good the bar has been raised to a level that historically marks a peak, not a launching pad. The Q1 print benefited from easy comps. Q2 won't. The 27% growth rate could halve on math alone when July prints lap stronger 2025 results. Markets don't always distinguish between “growth slowing” and “earnings missing.” They tend to react to the headline first and sort it out later.

Bottom line: stay long, but stay hedged. Trim into strength, reduce concentration in names that have done the most work, and keep dry powder for the first material disappointment. The asymmetry has shifted.

Counterpoint: Passive Is Here To Stay

Nicoletos makes a compelling case, but the conclusion to abandon passive strategies and embrace active stock picking deserves scrutiny. The following bullets share a few important counterpoints to his thesis:

- Timing: Arguments for active management's imminent comeback are not new. With each January forecast of what the year holds, there are always analysts predicting that this will be the year of the stock picker. They have consistently been proven wrong. As shown below, the S&P Indices Versus Active Index (SPIVA) indicates that the overwhelming majority of active managers underperform across multiple time horizons. Not shown, but in 2025, 79% of active investment strategies underperformed the market.

- High dispersion: Recently, the performance spread or dispersion between winners and losers has been wide. While that does present an opportunity for active investors, most active managers have failed to identify those winners and losers in advance. While high dispersion creates the ability to outperform major indexes, it also creates an equal opportunity to be wrong.

- Cost of being wrong: His paper undersells the performance risks. Fees, taxes, and behavioral mistakes resulting from active trading can harm returns in ways that are easy to underestimate but hard to recover from. The "deliberate basket" of AI winners that Nicoletos describes sounds great in theory. But executing it consistently, over a decade, against a low-cost index is another matter entirely.

There is no way to know whether active or passive strategies will be better in the future. The primary reason is that it's not just about the strategy, but about the infinite ways investors can execute them. We believe it is most important for investors is to select a strategy that properly addresses their risk tolerance and return goals. One that will help them meet their future goals, regardless of how it performs versus an index.

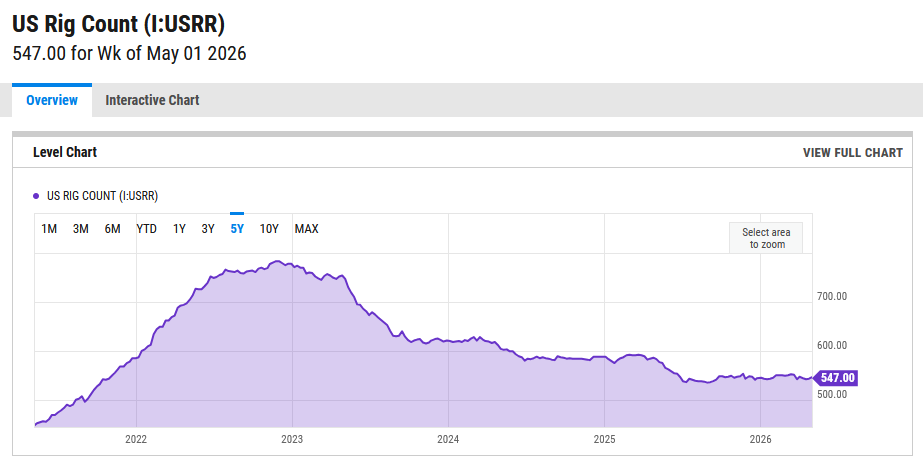

Rig Counts Cast Doubts On High Future Oil Prices

The number of US oil rigs in operation provides a good indication of what oil drillers think of future oil prices. As we share below, the rig count has remained steady despite the price of crude oil nearly doubling since the Iranian conflict started. This is an indication, that those putting money to work do not think higher oil prices will remain at current levels. To wit, future oil prices, a year out have risen by 10-15%, far less than the cash price for crude oil.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Nicoletos: AI Makes A Case For Active Strategies appeared first on RIA.

Full story here Are you the author?You Might Also Like

The Apple AI Strategy: Discipline Over Hype

The Apple AI Strategy: Discipline Over Hype

2026-04-08

While tech giants invest billions in AI, Apple executives are quietly sitting on their hands and a mountain of cash. Given the massive growth in AI investments, as shown in the graphs below, executives of leading companies at the forefront of AI development must be ecstatic about the prospect of AI significantly boosting their bottom …

Mag 7 Debt & Declining Free Cash Flow: Worrisome Or Not?

Mag 7 Debt & Declining Free Cash Flow: Worrisome Or Not?

2026-02-23

We have read a few articles expressing concern that the free cash flow for many of the Magnificent (Mag) 7 companies that are heavily involved in AI development and/or data center construction has leveled off. Furthermore, the hyperscalers, including Amazon, Microsoft, Google, and Oracle, issued over $120 billion in debt last year. Additionally, Google just …

2026-02-21

🔎 At a Glance 🏛️ Market Brief – War With Iran On Friday, the Supreme Court struck down Trump’s signature tariffs. The ruling affects tariffs levied under the International Emergency Economic Powers Act (IEEPA) which includes the so-called reciprocal tariffs at various levels against nations all around the world to address trade imbalances, as well …

Market Outlook For 2026

Market Outlook For 2026

2026-01-03

🔎 At a Glance 💬 Don’t Miss Our Upcoming “Live & In Person” Summit Our 2026 Summit is a limited-seating event, so secure your tickets now before they sell out. Topics Include: I look forward to seeing you there. 🏛️ Market Brief – Strong Year-End Returns Lead to Bullish Market Outlooks Let’s start this week …

EBITDA And The Warnings Of Charlie Munger

EBITDA And The Warnings Of Charlie Munger

2025-11-15

🔎 At a Glance 💬 Ask a Question Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter? 📩 Email: [email protected]🐦 Follow & DM on X: @LanceRoberts📰 Subscribe on Substack: @LanceRoberts We read every message and may feature your question in next week’s issue! 🏛️ …

2025-11-12

Here we go again. The overnight funding markets are showing signs of stress, and the scent of QE is in the air. Per New York Fed President John Williams: Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long …

2025-11-11

Buckle Up! With the end of the government shutdown and the return to work of government employees comes a flood of economic data. Below is a list of old economic data that should be released over the coming weeks: The list goes on. But, of more importance is whether or not the markets will care …

Tags: Featured,newsletter