On Monday, our Commentary, The Market Knows What You Don't, shared an important lesson about how markets function. The message was timely, as fear and volatility over the prior few weeks had caused great anxiety among many investors. We wrote the following to help investors maintain a north star during these challenging times:

Market prices are based on all available information. Some of the information is widely known, while some is known only to a few investors. Regardless of what we know, think, or believe, the market knows more. The market is not always right, but given that it collectively knows more than any one of us, its price movements deserve our respect.

When we wrote that the ceasefire was fresh, the market correctly foresaw it. From its lows on March 30th up to the ceasefire, the S&P 500 rose about 7%. At the lows, the rhetoric from President Trump and Iranian spokespersons was incredibly concerning. It seemed there was little hope of peace. Moreover, and of greater concern to investors, some pundits were calling for oil prices to surge to $150, or even $200, per barrel. The rally from the bottom gained strength and got a big jolt from the ceasefire agreement. Despite the tenuous agreement and ongoing military actions across the Middle East, the agreement seemed likely to fail, yet the market continued to rise.

Interestingly, as we write this on Wednesday, April 15th, we are hearing from Fox News that Trump unofficially declares the war is near an end. Per Fox: NEW: President Trump says the war with Iran is "close to over." Great news, yet the market doesn't seem to care. The S&P 500 opened flat, and crude oil was slightly higher. The market had already priced in the good news before it was known to the general public. This is not a "we told you so" commentary, but rather another reminder to listen to the markets, regardless of whether you agree with them. We end with another quote from Monday's Commentary:

The moment we believe our views outweigh the market’s, we have stopped managing risk and started taking it.

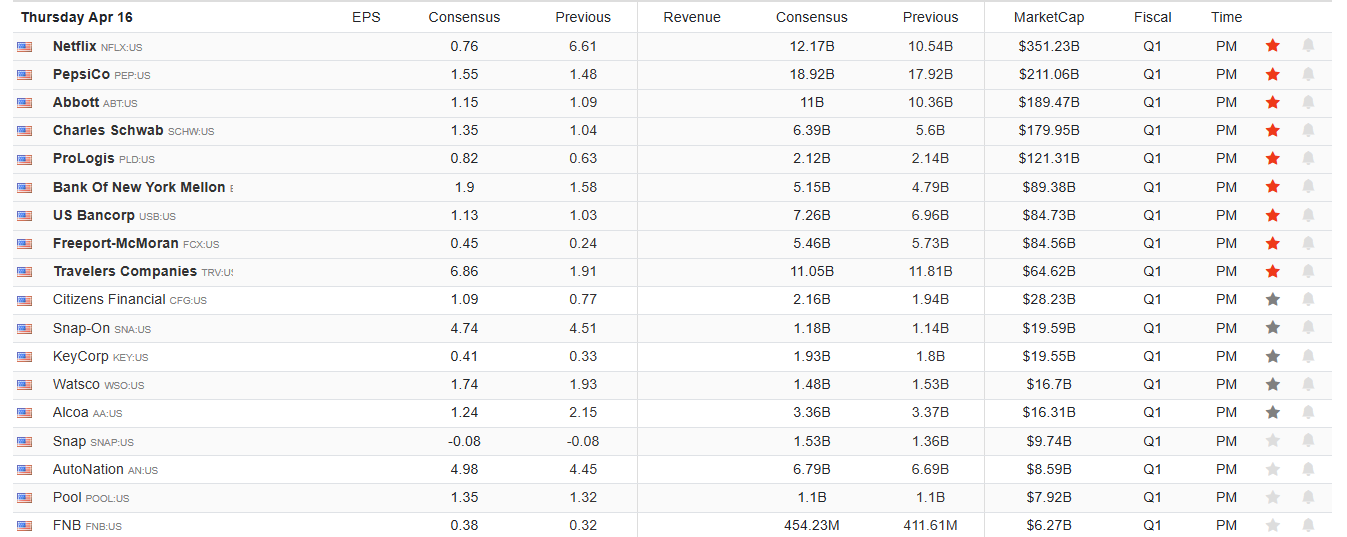

What To Watch Today

Earnings

Economy

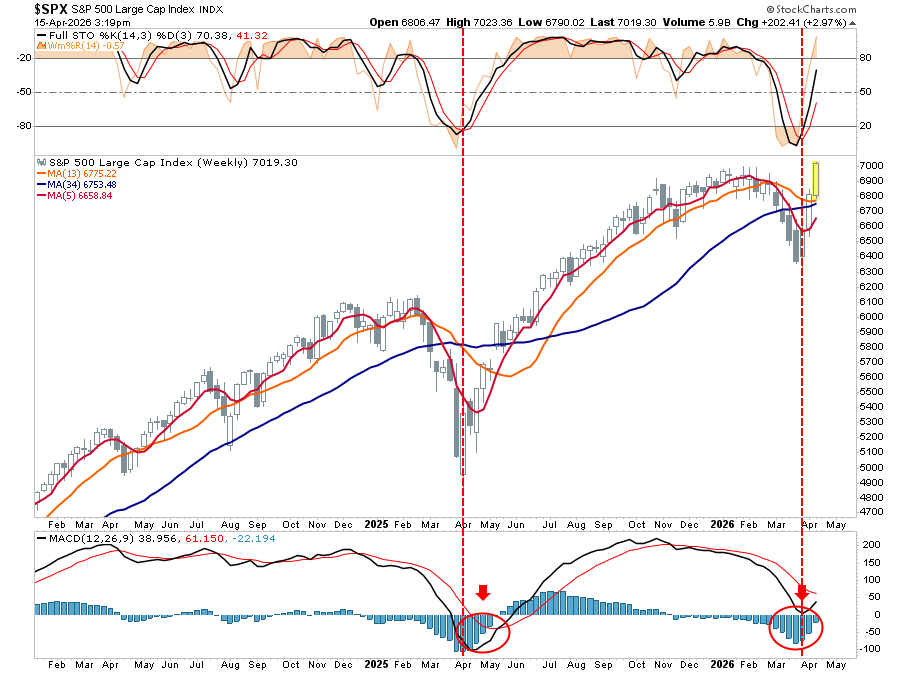

Market Trading Update

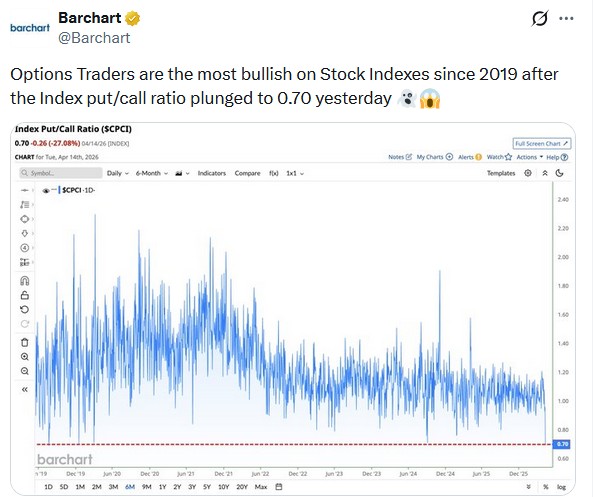

Yesterday, we discussed the bull versus bearish view of the market, and yesterday, it happened. The S&P 500 tagged a new all-time high, erasing every point of the Iran-war selloff in just over two weeks. As we noted here on Tuesday, the index was sitting within a single trading day of the January 27th peak, and the market didn’t wait long to close the gap. At the same time, the Nasdaq logged its 10th consecutive positive session, the longest winning streak the index has produced in years.

The bears have a ready-made explanation: short-covering. They’re not wrong. As we’ve discussed throughout this rally, short interest was elevated coming into the reversal, and headline-driven squeezes have a ceiling. Trump’s “deal” comments ignited the move; the Islamabad talks and ships clearing the Strait of Hormuz extended it. That’s a momentum sequence built on sentiment, not earnings revisions or balance sheet improvements. When hope meets a harsher reality, these moves tend to give back ground quickly.

However, the technical setup suggests more than just pure short-covering. The 50-day moving average never crossed below the 200-day during the entire selloff, and no death cross was ever confirmed. The VIX has retreated below 20. Breadth has improved. These are not the internals of a market in distribution. The comparison to the post-Liberation Day rally holds. The market also looked like a short squeeze at the time, and it kept going.

The honest answer is that both camps are right about their respective pieces. This rally was ignited by short-covering but sustained by technical confirmation. With JPMorgan’s earnings in the rearview and a full slate of S&P 500 companies reporting over the next three weeks, the market now has a fundamental catalyst to anchor to, or a reason to re-examine the bull case more critically. The macro and geopolitical backdrop hasn’t structurally changed. It’s softened. That’s not the same thing.

We’re watching the all-time high level as both a magnet and a potential ceiling. A clean breakout on improving volume would be a meaningful signal that this is more than just borrowed momentum. Until then, we’re adding exposure on confirmed strength while keeping stop levels intact.

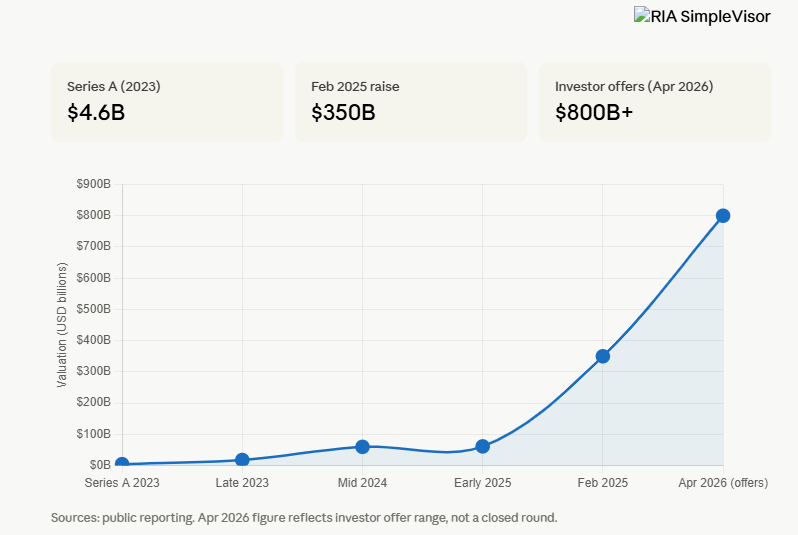

Anthropic's Valuation Doubles In Two Months

Anthropic, the company developing the Claude AI model, is reportedly taking investor offers that would value it upwards of $800 billion. If they decided to offer more shares, the price would be more than double the $350 billion valuation it had just two months ago, at the time of its February fundraising round. The company hasn't accepted any offers yet, and there's no guarantee it will.

Revenue growth seems to be behind the investor interest. Anthropic recently disclosed it has reached $30 billion in annualized revenue, up sharply from $19 billion just months earlier. For context, rival OpenAI is generating roughly $2 billion per month in revenue and recently raised over $120 billion at an $850 billion valuation.

Further driving investor interest is that they know of the potential for a market IPO in the Fall.

Will Private Credit Cause The Next Crisis?

When subprime defaults started to increase, losses weren’t the only problem. Equally important was a lack of trust among the largest financial institutions. Eroding confidence was most evident in the boiler room of the financial system, the overnight Fed Funds and repo markets.

These overnight loan markets ensure banks and brokers have ample daily liquidity to function. The biggest risk to the financial system is the concern that money lent today will not be repaid tomorrow. Once the rumors of losses started to grow, Wall Street questioned what their counterparties might be on the hook for. Trust was lost, and the overnight repo markets seized up.

Lehman Brothers, which had survived the Great Depression, went bankrupt in a weekend. AIG, a large issuer of synthetic insurance, collapsed. Many of the world’s largest banks and brokers were on the brink of failure. The web of leverage and derivatives surrounding subprime mortgages was so tight that pulling on one thread unraveled the entire financial structure.

While it’s fair to say that defaulting subprime borrowers were certainly the match, the bonfire, fueled by greed and irrational expectations, had been building for years.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The Market Knew And Proved It Again appeared first on RIA.

Full story here Are you the author?You Might Also Like

Private Credit Stress: Will The Fed Backstop Excuberance Again?

Private Credit Stress: Will The Fed Backstop Excuberance Again?

2026-03-18

The Fed is governed by its dual Congressional mandates of price stability and maximum employment. At times, however, the Fed throws these mandates out the window to protect the financial system. With liquidity and credit stress in the private credit market rising, we must consider whether the Fed might once again ignore its mandates to …

The South Park Market Of 2026

The South Park Market Of 2026

2026-01-23

I have been a “South Park” fan for as long as I can remember, and while the show isn’t a market guidebook, its brutal satire cuts through nonsense better than many Wall Street commentaries. Just like on the show, characters make absurd decisions and face absurd consequences, which is familiar to investors today. For example, …

Akademiker Pension Serves The US A Warning

Akademiker Pension Serves The US A Warning

2026-01-22

A Danish pension fund, Akademiker Pension, which manages roughly $25 billion in retirement assets for teachers, announced that it plans to sell all of its U.S. Treasury holdings by the end of January.

Fannie And Freddie To The Rescue

Fannie And Freddie To The Rescue

2026-01-12

President Trump is using Fannie Mae and Freddie Mac to help make housing more affordable. According to a TruthSocial post, the President claims Fannie and Freddie have a combined $200 billion in cash. Accordingly: I am instructing my Representatives (Fannie and Freddie) to buy $200 billion dollars In mortgage bonds. The hope is that increased …

Tags: Featured,newsletter