Dario Perkins of TS Lombard wrote a piece titled "How to Respond to Oil Shocks." His analysis draws on the Fed's history to address how it should respond to today's oil shock. While researching Fed transcripts from the 1990 Gulf War, he discovered a proposal by Don Kohn, senior Fed staffer, that offers a solution to the central bank's oil shock problem: nominal GDP targeting.

Kohn’s logic is straightforward and makes sense in the current environment where the Fed is contemplating monetary policy as oil prices spike, simultaneously boosting inflation and reducing economic growth. Per Kohn, if those two forces balance out, the Fed should hold rates steady. But if one dominates, the Fed should respond: "hike if nominal GDP growth rises" and "cut if nominal GDP growth falls." In other words, a demand shock calls for higher rates, while a supply-side shock calls for lower rates. Historically, as he shares in the table below, nominal GDP almost always falls after a supply-driven oil shock. Today's spike, driven by the Iranian conflict and "the Iranian weaponization of the Strait of Hormuz," is unambiguously a supply shock. By the Kohn framework, the Fed should be cutting the Fed Funds rate, not considering hiking it.

The current counterargument is the high-inflation era of the 1970s, when central banks were allegedly too dovish on inflation and allowed inflation expectations to spiral out of control. Perkins dismisses this comparison directly. To wit:

The 1973-74 recession "was one of the worst in history" and "in terms of its impact on unemployment, it was only slightly better than the GFC."

Importantly, he notes that the 1970s featured widespread union membership and inflation-indexed wage contracts that caused wages to "accelerate even as the economy sank." That wage-price spiral is nonexistent today. Thus, the inflationary danger of easing into an oil shock is considerably lower than the popular 1970s narrative suggests. His conclusion:

Central banks don't need to hike today. In fact, if they follow the advice of Don Kohn, they will probably need to ease policy.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we discussed that the market has been negative for 5 consecutive weeks, which supports at least a short-term reflexive rally. Another issue is that we have started the 2nd quarter, which brings a focus to both quarter earnings and the resumption of corporate share buybacks.

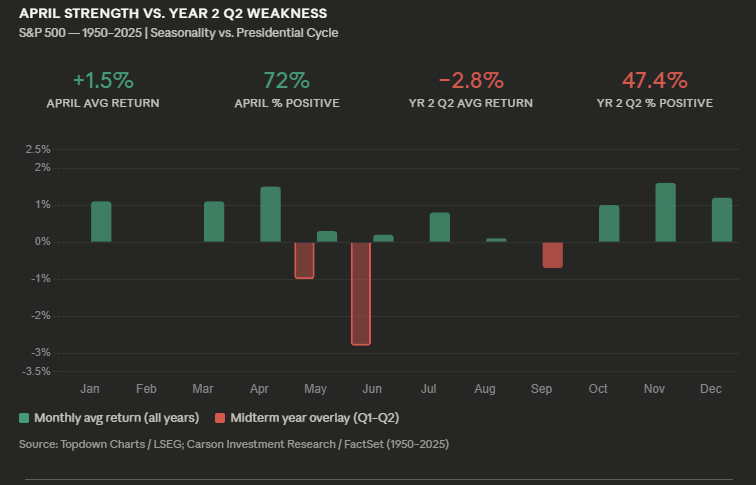

April is the best month of the year for the stock market. Since 1964, the S&P 500 has posted an average gain of 1.5% in April, with positive returns in 72% of all occurrences, the highest hit rate of any calendar month. The numbers aren't even close. November comes in second with an average return of 1.6%, but lags meaningfully on consistency, and every other month trails April on at least one of the two metrics.

The driver behind this seasonal strength isn't complicated. April is the heart of Q1 earnings season, and the combination of fresh corporate guidance, tax refund dollars flowing into retail brokerage accounts, and institutional rebalancing after a quarter-end window creates consistent buying pressure. Add the fact that April sits inside the historically strong November through April seasonal window, and you get a month that has repeatedly rewarded bulls.

Here's the problem in 2026.

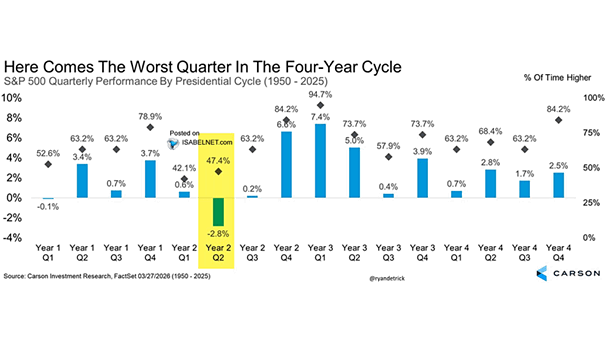

We're in Year 2 of the presidential cycle, and Q2 of Year 2 is the worst quarter in the entire four-year rotation. According to Carson Investment Research's FactSet data going back to 1950, the second quarter of the second year of the Presidential cycle has produced an average negative S&P 500 return of -2.8%. Furthermore, the index finishes higher only 47% of the time.

The average intra-year drawdown during midterm election years has been 18%, driven primarily by policy uncertainty as investors question whether the president will retain enough congressional support to sustain the legislative agenda. Uncertainty is always the market's enemy, and midterm cycles tend to front-load that pain into Q1 and Q2 before the fog lifts post-election. Since 1970, June has averaged nearly a 2% decline in midterm years, well below historical norms, suggesting the weakness doesn't end when April ends.

The bull case is that these cycles resolve. The average one-year forward return following the midterm-year drawdown low is 36.4%, and Q4 of midterm years has historically been the single strongest quarter of the entire four-year cycle. History rewards patience here, but that reward only comes to investors who survive Q2 without abandoning their positioning into the trough.

April's seasonal tailwind is real. The midterm cycle headwind is equally real. Don't let one cancel out the other in your thinking. Right now, the weight of the evidence favors the defense over the offense, so continue trading cautiously. However, this will eventually resolve, and we need to be in a position to increase exposure accordingly.

JOLTS- Employment Update

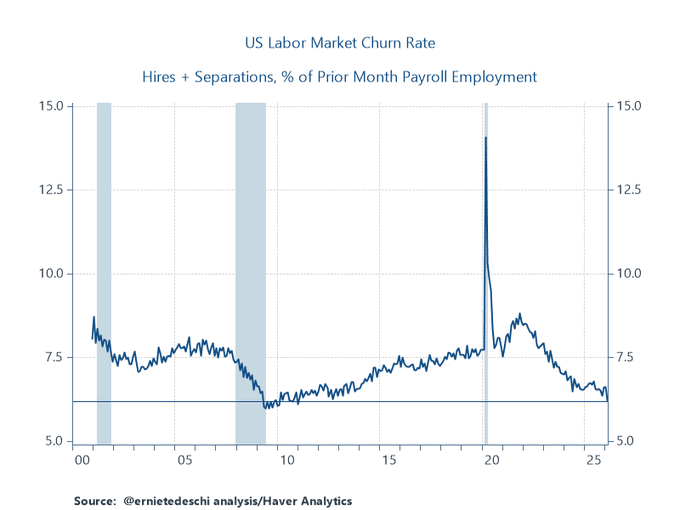

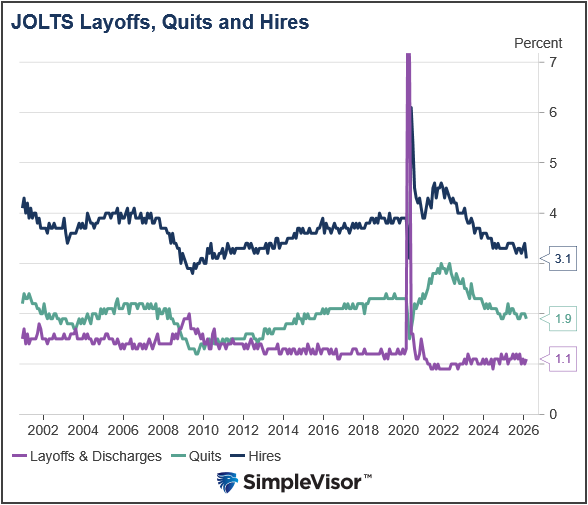

The JOLTS data once again confirmed that the labor market is in a low-hire, low-fire environment. The first graph below, courtesy of Ernie Tedeschi, shows that the labor market churn rate is near the worst since 2000. The data also confirm that labor market trends continue to weaken gradually. The headline figure for the number of job openings is 6.882 million. This is a decrease of 360,000 from the previous month's 7.240 million. However, it has been rangebound over the past few months. The job openings rate fell from 4.4% to 4.2%. The hiring rate of 3.1% is the lowest since April 2020, when COVID-19 lockdowns shuttered the economy.

Many consider the quits rate a barometer of the labor market. When workers voluntarily leave their jobs, it's a sign of confidence that they can find better conditions, and it serves as a leading indicator of wage inflation. Conversely, when they stay in their jobs, it reveals a lack of confidence in their ability to find a new, higher-paying job. The quit rate in February was 1.9%.

Higher Oil Prices Impact Consumers

The fear-mongering over whether the Iran conflict will trigger a decade-long 1970s-style inflation wave is all over social media. As we led, the real threat is not prolonged inflation but weaker economic growth. To wit, consider that the average American household spends approximately $3,000 to $4,000 annually on gasoline. At $100 per barrel, that figure rises by $1,200 to $2,700 per household relative to a $ 70-per-barrel baseline. Then take into account higher utility bills, elevated food prices driven by fertilizer and transportation costs, and the broader pass-through of energy costs into many goods and services consumers buy. Many consumers will be forced to reduce spending on other goods and services such as retail outlets, restaurants, cars, or entertainment venues.

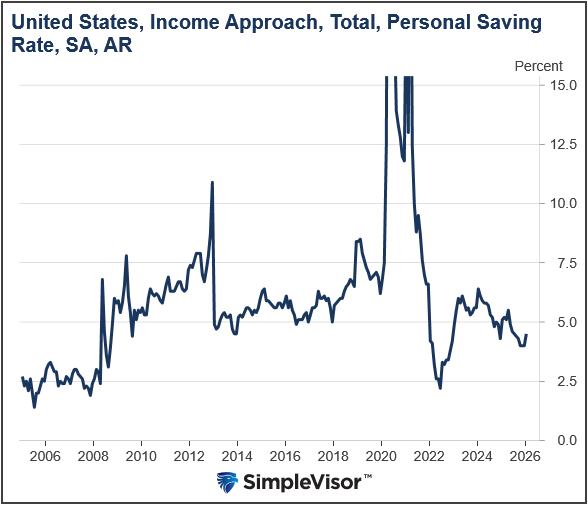

With a mere 0.7% growth in the fourth quarter, the economy and consumer were already showing signs of fatigue before the Iran conflict began. Credit card delinquencies had been rising, savings rates had declined from their post-pandemic highs, and high-income consumer spending (the cohort that drives a disproportionate share of discretionary economic activity) was beginning to soften. As we share below, consumers are saving at rates lower than at any time in the last ten years, except during the volatile 2020-2022 post-pandemic period.

Oil-driven price increases hitting an already stretched consumer are a meaningful headwind for corporate earnings in consumer-facing sectors and the companies that service them. Investors focused on the macro debate over yields and Fed policy may be underestimating the more direct and immediate impact that higher energy costs will have on the American consumer.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The Kohn Solution For An Uncertain Fed appeared first on RIA.

Full story here Are you the author?You Might Also Like

The VIX Is Lying: Or Is It?

The VIX Is Lying: Or Is It?

2026-03-30

Expected and historical (realized) volatility are sending investors a puzzling signal. Because of the Iran conflict, intense oil price swings, and rising interest rates, the VIX, or implied volatility (what options markets are pricing in as future fear), is elevated. However, actual realized volatility has been much more subdued. That gap between the VIX and …

Rubino: Fiat Currencies Are In A Death Spiral

Rubino: Fiat Currencies Are In A Death Spiral

2026-03-27

The fiat currency collapse narrative is one of the most emotionally satisfying arguments in all of financial punditry. It feels intellectually rigorous, draws on genuine history, and speaks to deep and legitimate anxieties about government overreach, monetary recklessness, and the long-term consequences of unlimited debt creation. Monetary analyst John Rubino makes the case as well …

2026-03-26

Albert Edwards from Societe Generale posted a graph similar to the one on the left below. It tracks the unemployment rate and its 3-year moving average. The red arrows signify every time the unemployment rate rose above the moving average. As we circle, the unemployment rate is now above the moving average. Albert’s comment alongside …

Financial Nihilism & The Trap Young Investors Are Walking Into

Financial Nihilism & The Trap Young Investors Are Walking Into

2026-02-13

The article from the Wall Street Journal titled “Why My Generation Is Turning to Financial Nihilism” by Kyla Scanlon argues that Gen Z is embracing high-risk financial behavior out of despair and detachment. Of course, it is essential to recognize that Kyla, although well-intentioned, is a young twenty-something influencer with limited real-life experience, and sees …

Speculative Narrative Unwinds

Speculative Narrative Unwinds

2026-02-09

For nearly two years, markets were driven by the same speculative narrative that “this time is different.” Bitcoin, precious metals, and AI-linked equities rose not only because of robust fundamentals, but also because investors clung to powerful narratives about inflation, disruption, and monetary collapse. Those speculative narratives are not only seductive but also contribute to …

Fannie And Freddie Add Billions To The Bond Market

Fannie And Freddie Add Billions To The Bond Market

2025-12-18

According to Bloomberg, Fannie Mae and Freddie Mac have been increasing the mortgages and mortgage-backed securities they hold on their own balance sheets. At their peak, before the financial crisis, Fannie and Freddie held a combined total of $1.6 trillion in mortgages. As we share below, courtesy of Bloomberg, their portfolio sizes are well below …

Tags: Featured,newsletter