Some media pundits are warning the public that high oil prices will spark a repeat of the high-inflation era of the 1970s. High oil prices will feed through to inflation; however, the economic, monetary policy, and geopolitical environments of the 1970s are quite different from today's. To wit, consider the following reasons for inflation in the 1970s:

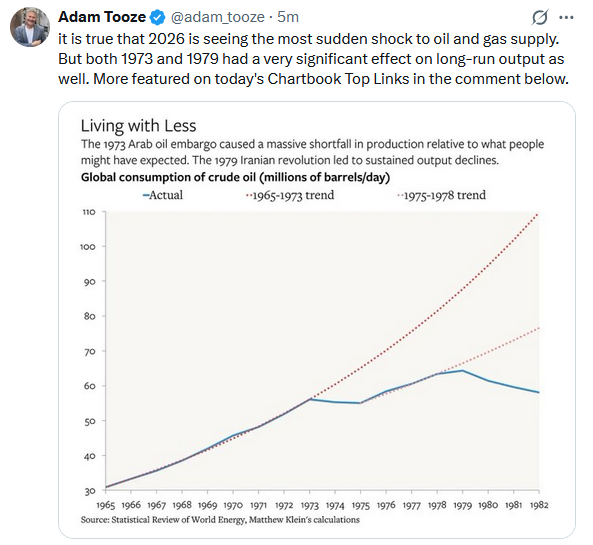

- 1973 Oil Embargo- OPEC nations imposed an oil embargo on the US in retaliation for US support of Israel during the Yom Kippur War. Oil prices quadrupled almost overnight, from approximately $3 per barrel to nearly $12 per barrel, delivering an immediate and severe supply shock to the economy. At the time, we were importing about a third of our oil usage; today, our net imports are less than 5%.

- Iranian Revolution- Oil prices doubled between 1979 and 1980 as the Iranian revolution resulted in the loss of 2.5 million barrels a day of oil.

- Gold Standard- President Nixon abandoned the gold standard in 1971, resulting in a weaker dollar and higher oil prices.

- Wage Price Spiral- in a circular fashion, unions garnered wage increases, which resulted in higher prices, which led to higher wages, and so on…. Today, unions have much less power, and wage growth is not a problem.

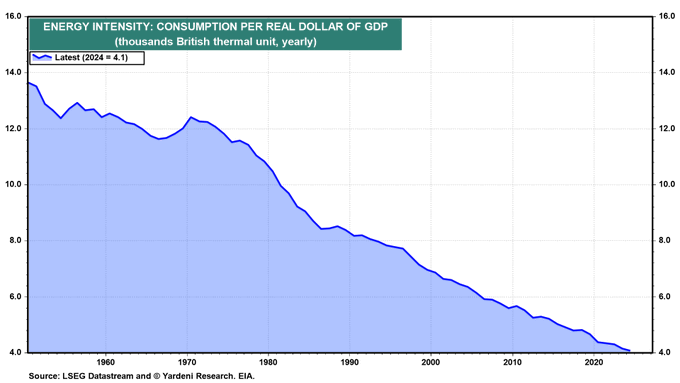

Yes, the current oil supply is severely impaired due to conflict and the closing of the Strait of Hormuz. However, supply shortages and associated high oil prices are likely temporary, unlike during the longer-lasting embargo and Iranian revolution noted above. Also, the other major factors mentioned above aren't issues we face today. Most importantly, the US is not dependent on foreign oil, and the economy's energy dependence is much less than it was in the 1970s. The following graph and commentary are courtesy Ed Yardeni.

The US economy now requires significantly less energy per unit of GDP than in earlier decades, reflecting efficiency gains and a shift away from manufacturing toward services (chart). As a result, oil price spikes are less inflationary and do less damage to real economic activity than in the past when energy intensity was much higher."

What To Watch Today

Earnings

Economy

Market Trading Update

As discussed yesterday, we remain below the 200-DMA, so risk levels are increased. As such, we reduced our equity holdings in our portfolios yesterday by 5% to increase cash levels for now. Today, I want to focus on oil prices, which have been the headlines as of late.

The last time oil spiked, in 2022, we wrote that:

"The market panic over crude is historically well-founded. The relief trade in energy stocks afterward almost never is"

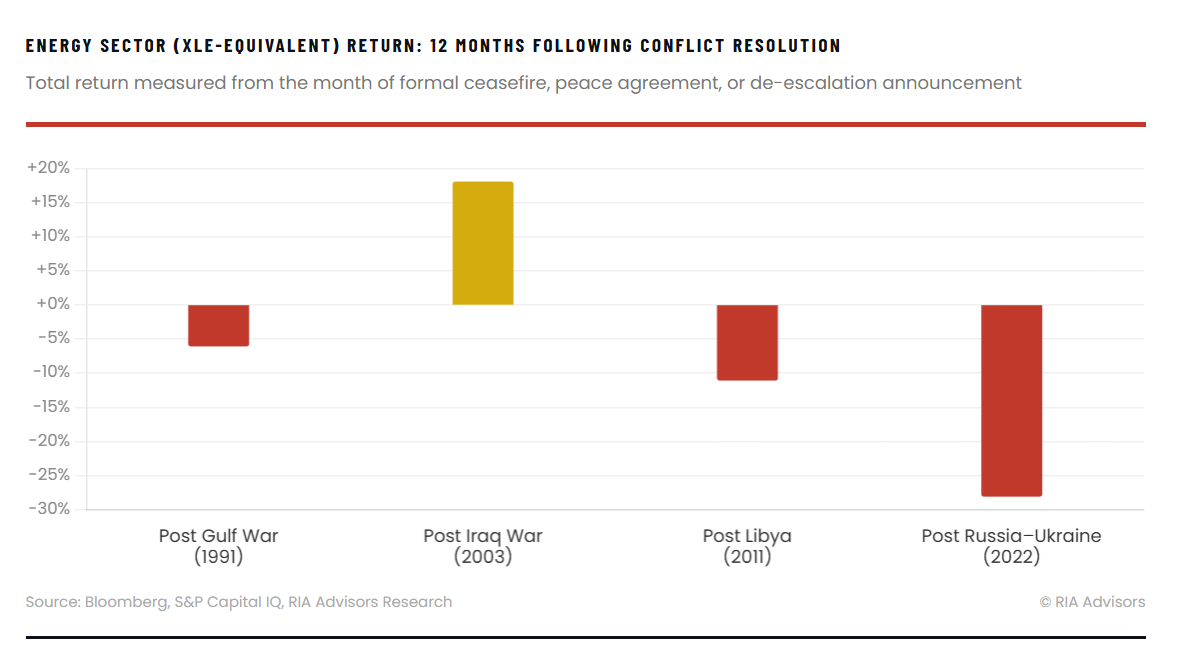

Oil's response to military conflict follows a pattern so consistent you could set your watch to it. The moment bullets fly anywhere near a major production corridor, crude prices spike, sometimes violently. With U.S.-Iran tensions running hot since late February, WTI has already reflected that premium. What history tells us, though, is that the spike is rarely the story investors should be focused on. The fade is.

Going back four decades, every major conflict touching Middle Eastern or Russian supply has produced an initial surge in crude. The Gulf War in 1990 sent WTI from roughly $17 to above $40 per barrel in under three months, a move that had oil bulls convinced a new paradigm had arrived. By the time coalition forces finished the job in early 1991, prices had collapsed back below $20. The pattern repeated itself with Libya in 2011 — a 31% spike on Brent, followed by a full reversal within six months of the ceasefire. Russia's invasion of Ukraine in February 2022 was the starkest modern example: WTI hit $130 by March, then spent the next eighteen months grinding steadily lower as markets priced out the supply disruption premium.

Such is likely to be the case today. As the old saying goes, "This too shall pass," and the structural reason isn't complicated. Markets price in worst-case supply disruption at the onset of any conflict. The Strait of Hormuz handles roughly 20% of global oil throughput, and any threat to that chokepoint commands an immediate risk premium. But conflicts rarely produce the sustained supply destruction initially feared. Production either continues under duress, alternative routes emerge, or strategic reserves get deployed. The premium that was bid in over days gets walked out over months.

"The trade that looks obvious at the start of a conflict — long energy — is almost never the trade that works through its resolution."

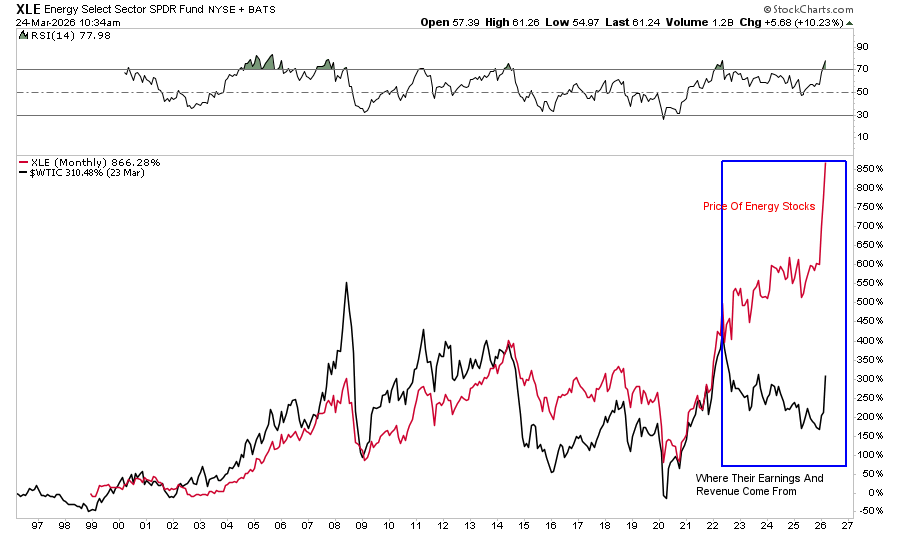

That brings us to energy stocks, where the pattern is more painful. The XLE and its predecessors have repeatedly attracted buyers during geopolitical spikes on the logic that higher crude translates directly into earnings. It does, in the short run. What investors consistently miss is that energy companies rarely get to bank those windfall margins for long. Politicians get involved. Capital allocation shifts. And when crude rolls over post-resolution, equity valuations reset hard and fast.

The 2003 Iraq War is the lone exception worth acknowledging. Energy stocks continued to advance through the post-invasion period and into 2007 as fears of "peak oil" were pervasive. But as with any commodity, high prices bring innovation and increased production. For oil, that was the shale innovation enabled by high oil prices at the time, which dramatically increased oil supplies and then collapsed oil prices. Strip out that tailwind, and the pattern holds: resolution is a sell signal for energy equities, not a reason to hold on.

If and when the current Iran situation moves toward de-escalation, the playbook suggests trimming energy exposure into current strength. Such is particularly the case as Energy stocks are grossly deviated from the long-term historical norms of where their earnings and revenue come from. The speculation is likely to reverse more significantly than we have seen in the past.

Airlines Hedge Jet Fuel Turbulence

With higher jet fuel prices, many consumers expect airfares to follow. To appreciate how higher oil prices impact airfares, consider that the standard industry metric for expenses is cost per available seat mile (CASM). Fuel typically accounts for 20% to 30% of CASM for major US carriers. However, when oil spikes to $100 per barrel, fuel can quickly represent 35% to 40% of total operating costs, which is why airline stocks are so sensitive to oil price movements and oftentimes hedge fuel prices.

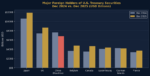

Fuel hedging practices vary significantly and have changed since the 2014 oil price collapse. At the time, airlines were well hedged and accordingly locked into above-market fuel costs. Accordingly, the industry shifted away from aggressive long-term hedging toward shorter-term tactical coverage or no hedging. Consider how the four major US airlines hedge fuel costs.

- Southwest Airlines — Historically, they are the most aggressive hedger, building a significant competitive advantage through fuel cost certainty in the 2000s. After getting burned by hedges in 2014, Southwest scaled back and now hedges roughly 50% to 60% of near-term consumption with far less long-term coverage than its earlier strategy.

- Delta Air Lines — Takes a unique approach by owning the Monroe Energy refinery, which provides a hedge against jet fuel price spikes. It supplements that with hedges covering roughly 20% to 50% of near-term fuel needs.

- United Airlines — They largely abandoned systematic fuel hedging after the 2014 oil collapse. They now hedge minimally, relying instead on operational efficiency and fuel surcharges passed through to consumers to manage price exposure.

- American Airlines — The least aggressive hedger among the major carriers. They have operated largely unhedged in recent years, arguing that hedging costs more than it saves over a full market cycle. Like United, they prefer to manage fuel costs through surcharges and efficiency measures.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post High Oil Prices Won’t Spark A 1970s Inflation Repeat appeared first on RIA.

Full story here Are you the author?You Might Also Like

The Dollar’s Plumbing: Conspiracy Vs. Data

The Dollar’s Plumbing: Conspiracy Vs. Data

2026-03-20

Every few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold. The BRICS are building a new monetary order. The sanctions that froze $300 billion of Russia’s reserves in 2022 proved, the argument goes, that dollar-denominated assets are …

Treasury Bond Yields Don’t Lie: But Wars Don’t Drive Them

Treasury Bond Yields Don’t Lie: But Wars Don’t Drive Them

2026-03-16

This past weekend, Adam Taggart and I discussed what happens to Treasury bond yields when the United States enters a military conflict. The conventional wisdom is reflexive and tidy. A conflict triggers a flight to safety, money floods into U.S. government bonds, and yields fall. It’s a clean narrative. Unfortunately, it is wrong more than …

2026-03-07

🔎 At a Glance Give Us A Review ***** If you enjoy our work each week, could you be so kind as to leave us a review? It would be most appreciated. 🏛️ Market Brief – Markets Navigate Military Conflict It was a brutal week on Wall Street. The S&P 500 finished at its lowest close …

Tags: Featured,newsletter