Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The Gulf War continues rage. China has reportedly told top oil refiners to suspend exports of diesel and gasoline. The disruption is beginning to impact shipments of fertilizer, chemicals, aluminum, as well as natural gas and oil fuels. In the next few days, several countries will reportedly run out of storage capacity and will have to cut output. Other secondary impacts include worker remittances from the region, which are important for several Asian countries, including India and the Philippines.

The US dollar is mostly firmer but largely within the recent ranges. The inflationary implications are higher energy prices continue to press bond yields higher. With April WTI still well below levels many thought likely if the Strait of Hormuz was effectively shut, there seems to still be a sense that the war can end shortly, though hope may be getting ahead of reality.

Prices

G10

• The euro consolidated with a slightly firmer basis but spent most of yesterday’s session below the lower Bollinger Band (~$1.1615 today). Today, it is consolidating within yesterday’s range and is mostly within 30-ticks of the lower Bollinger Band. The lack of near-term conviction means that short-term speculators may be more inclined to buy into euro strength than on weakness.

• The dollar stalled in front of JPY158 on Tuesday and found support yesterday near JPY156.85. It was sold to around JPY156.45 today but is back near session highs in late European morning turnover (~JPY157.40). Stepped up intervention threat by the finance minister coincided with the greenback’s broader pullback. With a BOJ rate hike pushed deeper into H2, two dovish nominations to the BOJ board, it is difficult to imagine much US support for intervention. It is hardly a one-way or disorderly market. One-month implied volatility peaked in late January, near 11.6%. It is now around 9.5%. Options for $1 bln at JPY157 expire today.

• Sterling was mostly confined yesterday to about a half-cent on both sides of Tuesday’s settlement (~$1.3360). It has traded between almost $1.3305 and $1.3390 today; so far within yesterday’s range. Options for GBP535 mln at $1.3350 expire today. It closed little firmer, but the lack of near-term conviction continues.

• Last week, the US dollar traded between roughly CAD1.3625 and CAD1.3725. It spiked to nearly CAD1.3755 on Tuesday but once again failed to settle above CAD1.3700. It tested the lower end of the range late yesterday. It is still there today, trading between about CAD1.3630 and CAD1.3670. There are a little more than $300 mln of options at CAD1.3650 that expire today. The broad sideways movement leaves the daily momentum indicators poised to turn lower.

• The volatility injected by the Middle East war was unable to push the Australian dollar out of last month’s trading range. For the past three weeks, it has mostly traded between $0.7000 and $0.7100. It nearly covers that range today, trading between $0.7010 and $0.7090. The exceptions this week have been on the downside, while the exceptions last week were on the upside. The Aussie has not settled below $0.7100 in a month. Model-driven trading may get a sell signal when the five-day moving average crosses below the 20-day moving average, which it is threatening to do today. It has not done since being whipsawed around the middle of January.

EM

• As markets stabilized, the Mexican peso, which got hit on Tuesday, found new bids yesterday. After reaching MXN17.8770 on Tuesday, the greenback retreated to about MXN17.5250 yesterday. Initial dollar support is seen around MXN17.50, where options for nearly $340 mln expire today. While the dollar held above Tuesday’s low against the Mexican peso, it took out Tuesday’s lows against the other actively traded Latam Currencies (Brazilian real, Colombian peso, and Chilean peso). The dollar is trading quietly so far today between about MXN17.5720 and MXN17.7075.

• The offshore yuan recovered yesterday. The dollar peaked in front of CNH6.95 on Tuesday and slipped below CNH6.89 yesterday. Tuesday’s low was around CNH6.8750. It remains within Tuesday’s range today. The US dollar recovered from CNH6.8780 and resurfaced above CNH6.90. It is trading near the high in late European morning turnover. Some news wires reports indicated that Chinese banks sold dollars on Wednesday, but there was not indication whether these were commercial transactions or on behalf of the central bank. The PBOC set the dollar’s reference rate at a new low since April 2023 today (CNY6.9007 from CNY6.9124 yesterday).

• Aggressive intervention by the Reserve Bank of India helped the rupee recover from record lows on Wednesday. The intervention reportedly began before the local markets officially opened. The dollar gapped lower and fell to around INR91.4125 before it recovered to nearly INR91.6390. Wednesday’s dollar low was slightly above INR92.00. The rupee and the Indian economy are particularly vulnerable to the disruption of the oil and gas market.

Other Markets

• Equity markets in the Asia Pacific region bounced back today. Japanese indices rose nearly 2%, Taiwan jumped almost 2.6%, while the highly volatile South Korean Kospi soared 9.6%. India’s leading indices rose a little more than 1%. Europe’s Stoxx 600 is up around 0.40% after yesterday’s 1.35% gain. US index futures are nursing small losses.

• Benchmark 10-year yields are higher. They were 4-5 bp higher in Australia, New Zealand, and Japan. They are mostly 5-7 bp higher in Europe. The 10-year US Treasury yield is up a couple of basis points to 4.12%.

• Gold is firm but inside yesterday’s range. It has been mostly confined between the 20-day moving average (~$5088) and the five-day moving average (~$5200). Silver tested $80 and recovered to around $85.55. It is around $84.50 in late European morning turnover.

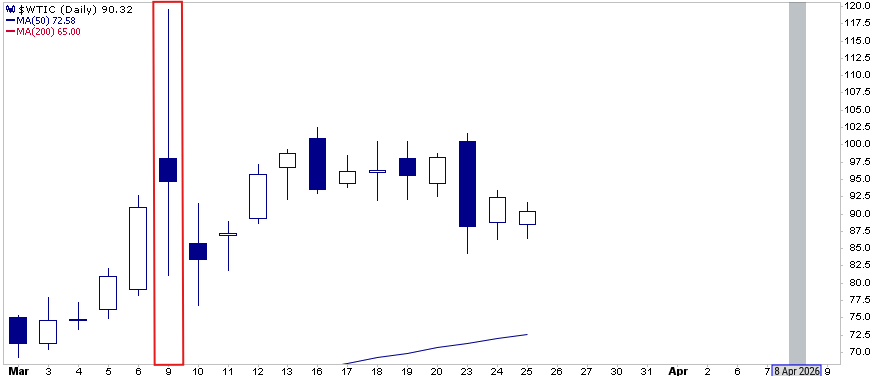

• April WTI made a new high earlier today, a little above $78. It has pulled back to around $75 by the European morning and is now back to the $76.50 area.

Data

• The US high frequency data is of secondary importance today. The inflation implication of the war renders the data moot. The market has already pushed the next Fed rate cut into September. Challenger job cuts rose almost 118% year-over-year in January, and the February report is due today. Weekly initial jobless claims may have risen for the second consecutive week, something not seen since last September-October. Nonfarm productivity and unit labor costs are not observed direction but are derived from the GDP estimate. Productivity looks to have slowed sharply (~1.8% from 4.9% in Q3 25 and 4.1% in Q2 25). This would mean that productivity increased by almost 2.2% in 2025, slightly better than 1.9% in 2024, and nothing to suggest an AI-led productivity boom is at hand. Import/export price indices do not typically move the market. Tomorrow the US reports retail sales, where the headline was likely dragged lower by soft auto sales, and the February jobs report. The median forecast in Bloomberg’s survey is for a 59k increase in nonfarm payrolls after the initial estimate of 130k in January.

• Mexico reports December capex, private consumption, and February consumer confidence. With Q4 25 GDP reported last month (0.9% quarter-over-quarter), the data will likely have little impact.

• The eurozone retail sales continue to struggle. They rose by an average of 0.2% a month last year. Today’s January estimate of -0.1% was weaker than the 0.3% projected by the median forecast in Bloomberg’s survey but the sting was lessened by the upward revision to the December series (0.1% from the initial -0.5% estimate).

• The UK February construction PMI slipped to 44.5 from 46.4 in January. It has been below the 50 boom/bust level since the end of 2024.

• Australia’s goods trade surplus is narrowing. It averaged A$3.8 bln a month in 2025, down from an average of A$5.8 bln in 2024 and A$10.4 bln in 2023. The January trade surplus of A$2.6 bln reported earlier today was smaller than expected and compared with A$4.5 bln in January 2025. Last year, exports of goods rose by a monthly average of 0.4% a month while imports rose by an average of 0.5% a month. In January, exports fell by slipped by 0.9% and imports rose by 0.8%. Separately, Australia reported that household spending rose by 0.3% in January after a revised 0.5% decline in December (initially reported as -0.4%).

• China’s National People’s Congress endorsed a 4.5%-5.0% growth target, a record low. However, to achieve it, officials appear to assume more stimulus. The general budget (including central and local governments) remained at 4% of GDP.

You Might Also Like

Dollar Jumps on War, but Treasuries are No Safe Haven

Dollar Jumps on War, but Treasuries are No Safe Haven

2026-03-02

There is one fundamental driver today and that is the Middle East war. After finishing last week on a soft note, the greenback has rallied. It is up by 0.5% or more against most of the G10 currencies. The Canadian dollar, which often performs relatively better in a strong US dollar environment is off the …

Dollar Sold Broadly, while Yen Soars on Fear of Joint Intervention

Dollar Sold Broadly, while Yen Soars on Fear of Joint Intervention

2026-01-26

The US dollar came under strong selling pressure at the start of today’s trading. The fear of joint intervention after the pre-weekend Fed checking on rates, ostensibly on behalf of the US Treasury, and underscored by Japanese officials, including Prime Minister Takaichi. Meanwhile, another tragic ICE related death in Minnesota has sparked a threat from …

Dollar Consolidates as American Exceptionalism Returns

Dollar Consolidates as American Exceptionalism Returns

2026-01-07

Drivers: The US dollar is trading narrowly mixed against the G10 currencies. The market has an eye toward the US employment data, which often roils trading, due Friday. Indications suggest that the US Supreme Court may rule on the legality of the broad US tariffs imposed under emergency power legislation. Most seem to expect the …

Equities Wish it were Turn Around Tuesday as Rout Continues and No Relief for the Yen

Equities Wish it were Turn Around Tuesday as Rout Continues and No Relief for the Yen

2025-11-18

Overview: A sell-off in equities is continuing while the foreign exchange market is quiet with the greenback confined mostly to narrow ranges. It is firmer against most currencies, though the dollar bloc is the most resilient today. The dollar reached a new nine-month high against the yen. Despite some escalating rhetoric from the MOF, the …

Sterling and Gilts Weighed Down by UK Government Budget Shift

Sterling and Gilts Weighed Down by UK Government Budget Shift

2025-11-14

Overview: The US dollar is trading with a firmer bias today but is mostly within yesterday’s range. There are four developments to note. First, China’s October data mostly disappointed, but the PBOC set the dollar’s reference rate at a new low since October 2024. Second, the UK government reportedly has shifted strategies to focus on …

Eerie Calm in the Foreign Exchange Market

Eerie Calm in the Foreign Exchange Market

2025-10-20

Overview: The foreign exchange market is quiet, and the US dollar is slightly softer against most of the G10 currencies, though the Australian and Canadian dollar are struggling. Most emerging market currencies are also firmer. The market seems optimistic that the US-China trade tensions can de-escalate with Beijing re-assigning Li Chenggang who apparently annoyed the …

Quiet Foreign Exchange Market in which the Greenback Struggles to Find Traction

Quiet Foreign Exchange Market in which the Greenback Struggles to Find Traction

2025-10-02

Overview: The dollar is soft and trading near session lows in late European morning turnover. The news stream is light and large parts of the US federal government remain closed. China’s mainland markets are on holiday. Among the G10 currencies, the Canadian dollar remains the laggard in a soft greenback environment. Most emerging market currencies …

Tags: Currency Movement,Featured,newsletter